Major Central Bank Meetings Last Week

Despite the sound global economic recovery and improving outlook, rising inflation levels continue to be a major source of concern and focus for global central banks. According to the International Monetary Fund, inflation prospects are highly uncertain due to COVID. The COVID-19 pandemic has led to major disruptions in global supply chains and labor, creating massive shortages in many industries. These, coupled with rapidly rising demand as economies are reopening and lifting their restrictions, are creating global inflationary pressures. If inflation pressures persist longer than what central banks are currently anticipating, they will all be forced to play catch-up by reducing Quantitative Easing (QE) faster or raising rates sooner. This will create an environment of uncertainty and put downward pressure on risk assets accompanied by a steepening yield curve.

With these points in mind, there were three major central bank meetings last week to address such concerns – the Reserve Bank of Australia, the U.S. Federal Reserve, and the Bank of England. Let’s provide some context to the meetings, show their outcomes and provide a glimpse into future monetary policy decisions.

Expectations Ahead of Central Bank Meetings

In September of 2021, annual Consumer Price Index (CPI) inflation rates hit highs of 5.4% in the U.S., 3.1% in the U.K., and 3% in Australia. To put that in perspective, in September 2020, inflation was 1.4%, 0.5%, and 0.7% in those countries, respectively. With rising inflation expectations, tighter monetary policy decisions by major central banks have been long awaited. Many economists and market observers are pushing for central banks to raise their short-term interest rates and retreat from the huge emergency asset-buying programs launched during the pandemic. In expectations of more hawkish central bank decisions to come, the two-year U.S. Treasury yield has increased to an 18-month high of 0.55% in late October. In the U.K., the yield on the 10-year government gilt jumped by 0.37 percentage points over the last two months.

However, central banks have been reluctant to raise interest rates as economies are yet to fully recover. Here plays the classical tradeoff between inflation and employment. There is the concern that if advanced economies were to tighten monetary policies earlier than necessary, deflationary pressures that defined the previous decade and led to the adoption of the near-zero interest rates would return. This is especially the case with the low rate of wage growth and the low actual underlying inflation in many countries.

In its last meeting on October 28, the European Central Bank (ECB) announced that it will continue its high pace asset-purchasing program, while keeping key interest rates unchanged near zero. ECB President Christine Lagarde stated that: “Inflation is rising, primarily because of the surge in energy prices but also as the recovery in demand is outpacing constrained supply. We foresee inflation rising further in the near term, but then declining in the course of next year.”

Three major central bank meetings took place last week. On Tuesday, the Reserve Bank of Australia announced that it will abandon its yield curve control strategy while leaving interest rates unchanged. This was followed by the U.S. Federal Reserve meeting, which concluded on Wednesday with an announcement to gradually start tapering off its asset purchasing program, yet also leaving the interest rates at their low levels. Finally, on Thursday, the Bank of England announced that it would neither increase its interest rate nor alter its asset-purchasing program in any way. Below are the main highlights from the three central bank meetings.

The Reserve Bank of Australia (RBA)

In wake of the COVID-19 pandemic, the Australian central bank has adopted an accommodative monetary policy in March 2020. This involved setting the overnight cash rate to 0.1%, an asset-purchase program of AU$4-billion-a-week (US$3 billion), in addition to a yield curve control strategy that caps the 3-year yields at 0.1% (0.25% prior to November 2020) through the purchase of government bonds.

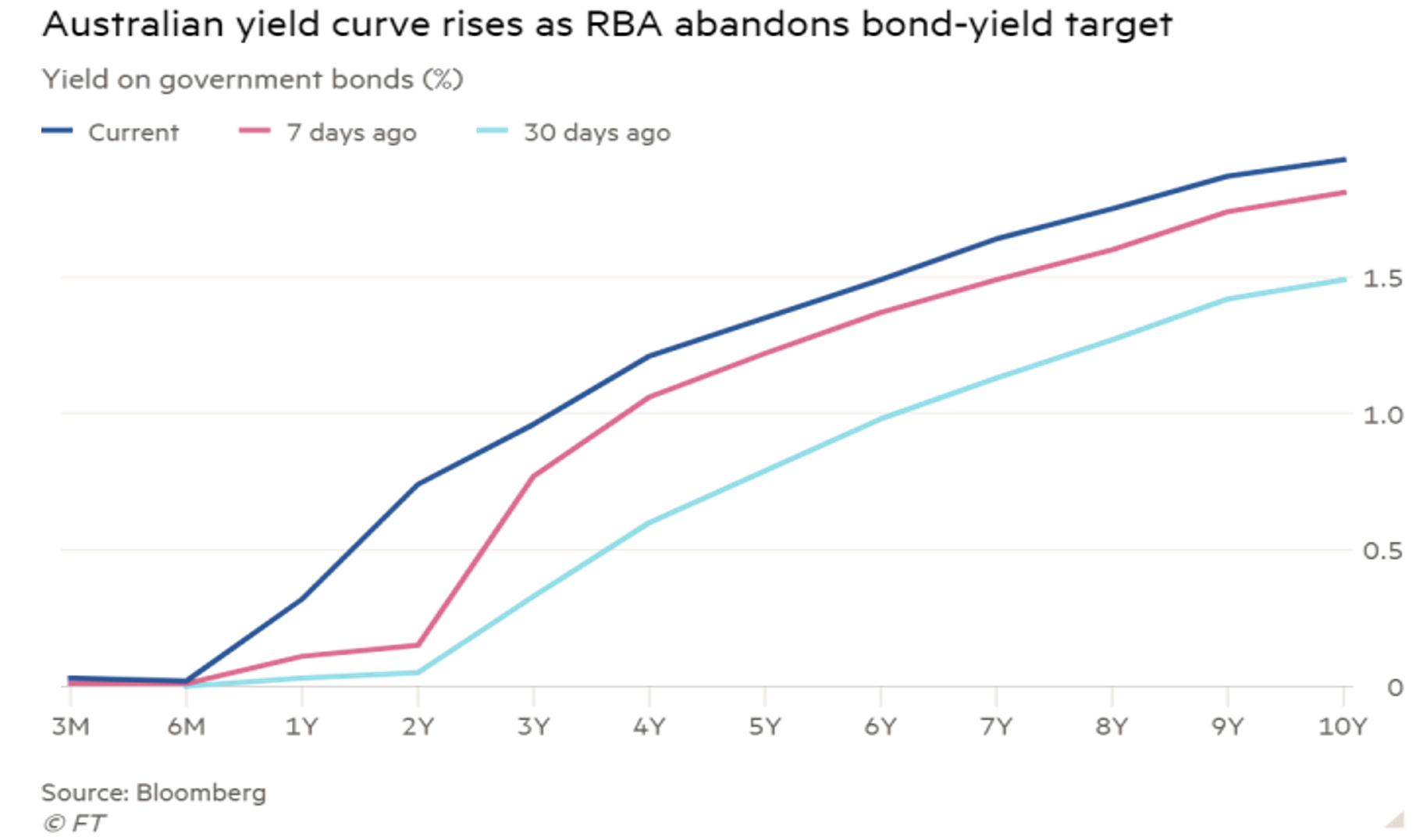

The RBA concluded its Tuesday meeting with a decision to discontinue its yield curve control, while maintaining the 0.1% cash rate. The central bank also decided to leave the weekly pace of asset purchases unchanged, up to at least mid-February 2022. The RBA came to this decision following the strong recovery of the Australian economy, with higher vaccination rates and lower restrictions. The graph below shows how the Australian yield curve rose following the central bank’s decision. A couple of weeks preceding this decision, the RBA has allowed the 3-year yield to increase over its 0.1% cap as it traded at 0.98% one day prior to the meeting.

Annual CPI Inflation recorded a high of 3% in September 2021, which was mainly driven by higher fuel prices, house prices, and the shortages of global supply chains. Nevertheless, the central bank believes that inflation is still as low as 2.1% in underlying terms and is expected to marginally increase in the coming two years. The problem lies in the low growth rate of wages, which should gradually, yet slowly, increase overtime. For this reason, the RBA has stressed that it won’t rush increasing short-term interest rates until it has stabilised actual inflation within a sustainable target of 2-3%. According to RBA governor Philip Lowe, this move will necessitate the labor market to generate substantially higher wage growth rates than current levels, which will take some time and for which the central bank is willing to be patient.

The United States Federal Reserve

The Fed concluded its two-day meeting on Wednesday by announcing a plan to start tapering off its $120-billion-a-month asset purchase program later this year. The meeting’s focus was on winding down asset buying, while interest rates were left near zero. In wake of the rising global inflation, this has been a long-awaited decision since May or June.

Since June 2020, the Fed has been purchasing $80 billion and $40 billion of Treasury securities and mortgage-backed securities (MBS), respectively, every month to inject more liquidity into the market and stabilise the economy. Beginning later this month, the Federal Open Market Committee (FOMC) should start reducing its monthly pace of asset purchases by $10 billion for Treasuries and $5 billion for MBS. A similar incremental decrease will also be applied in December, to reduce Treasury and MBS purchases by a cumulative of $20 and $10 billion, respectively. Moving forward, the FOMC expects to apply similar incremental reductions each month, however, it is prepared to adjust the pace and direction of asset purchases as needed, in case there is any change in the economic outlook. In its statement, the committee highlighted that “The Federal Reserve’s ongoing purchases and holdings of securities will continue to foster smooth market functioning and accommodative financial conditions, thereby supporting the flow of credit to households and businesses… The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals.”

The decision to slow down the rate of asset purchases has come as a result of the sound economic performance and recovery since last December coupled by the rising inflation rate. The Fed targets an inflation rate of around 2% over the long-run. In his statement, the Fed’s chair Jerome Powell highlighted that the current inflation level is not consistent with price stability and that the central bank would use its full range of tools to get inflation under control. Nevertheless, the time to raise interest rates has not come yet. Supporting labor market recovery and reaching full employment is another major FED policy goal, for which according to Powell, there is “still ground to cover.” Today, this remains a critical hurdle before the central bank can raise interest rates.

Yet, the focus is squarely on inflation. During his press conference, Powell mentioned inflation 19 times and kept pressing the point that COVID was responsible for the elevated rate of prices. Here’s the key text from the presser to provide guidance on the mindset of the FOMC: “Getting to your question, our baseline expectation is that supply bottlenecks and shortages will persist well into next year, and elevated inflation as well and that as the pandemic subsides, supply chain bottlenecks will abate, and job growth will move back up. And as that happens, inflation will decline from today’s elevated levels.”

The Bank of England

In its meeting on Thursday, the BoE announced that it will hold benchmark interest rates unchanged at their low level of 0.1%, which was set in March 2020 when the pandemic hit. This came as a surprise to investors and market observers who expected the BoE to be the first central bank (of the 3) to raise its policy rate. Nevertheless, the Monetary Policy Committee (MPC) decision to standstill came as a 7-2 majority vote. No additional asset-purchase programs were announced, maintaining the total assets bought at £895 billion ($1.2 trillion).

The BoE has been adopting a policy of QE since 2009, following the global financial crisis. This involves the massive purchase of U.K. government bonds and corporate bonds, to raise their price and reduce their yield. Since March 2020, the central bank has added a total of £450 billion ($607 billion) to its QE program to support the economy in wake of the COVID-19 pandemic. To date, the BoE has purchased a total of £895 billion ($1.2 trillion) worth of assets in QE, of which £875 are government bonds and only £20 are non-financial investment-grade corporate bonds.

The central bank follows an inflation target of 2%, which is suitable for maintaining a healthy growth rate and full employment. The BoE also published its quarterly monetary policy report on Thursday, which expects inflation to temporarily increase to around 5% next spring, before it falls back to its target. This fall will come as oil prices fall and supply shortages shrink, the report argues. Despite the bank’s decision to maintain its low interest rates, the report acknowledged the need for future interest rates to increase modestly to gradually return inflation to its 2% target.

How Did Markets React to the Meetings?

Stock markets have reacted favorably following the news on Wednesday. Major U.S. stocks rose to high records as the FED’s announcements signaled a positive economic outlook, which raised investors’ confidence. After all, the central bank wouldn’t have started tapering its emergency stimulus if it hadn’t expected an optimistic recovery path for the economy. The S&P 500 Index (SPX) rose by 0.65%, closing at a record high of 4660.57. This graph shows the jump in the S&P 500 index on Wednesday, following the 14:00 FED’s announcement.

Other benchmark indices also showed record increases on Wednesday. The Nasdaq Composite traded up 1% and the Dow Jones Industrial Average rose by 0.29%. Small market cap companies have shown the highest jump, with the Russel 2000 closing at an up of close to 2%. On the debt side prices fell, with the 10-year US Treasury yield jumping to 1.6% (an increase of 0.05 percentage points) reflecting expectations of higher long-term borrowing costs.

Positive global market reactions were also observed as the Japanese Topix index was up by 0.9%, while the European Stoxx 600 and the Australian S&P/ASX were both up by 0.4% on Wednesday. This rise in the Australian ASX came after its prior 0.6% fall on Tuesday, following the RBA’s announcement to abandon its control over the yield curve, which signaled to investors that borrowing costs might have to rise sooner than previously expected.

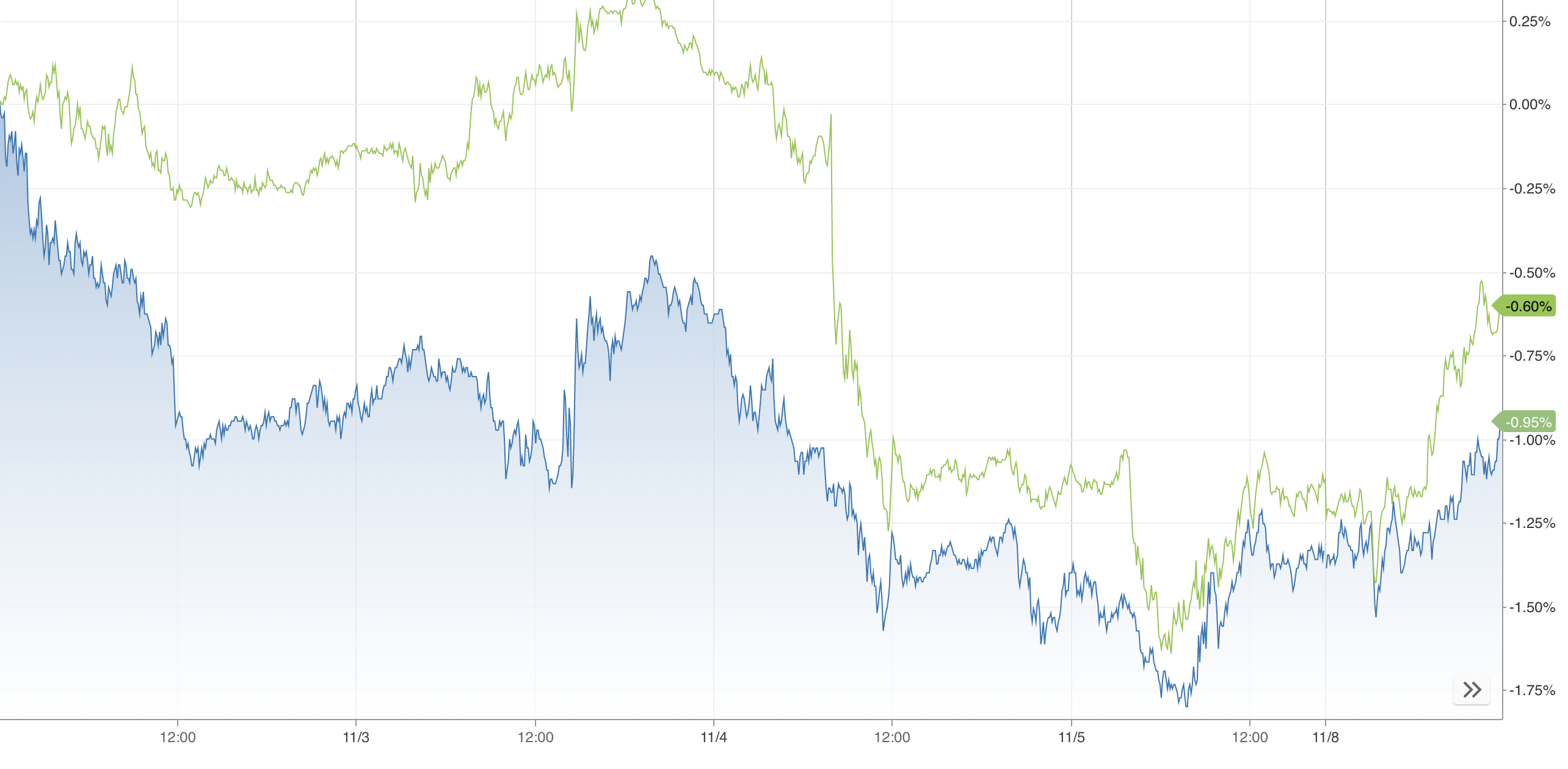

Contrary to many expectations, the three central bank meetings appeared to have signaled continuation of current easy monetary policies. This might have disappointed investors’ hopes for more hawkish reactions of rising interest rates. This was reflected in how the Australian dollar and the Sterling all dipped following the announcements.

AUDUSD in blue, GBPUSD in green.

While most central bank officials insist that current inflation pressures are only transitory, many economists and market observers disagree. According to the Fed, inflation is expected to be transitory and as stated by Powell: “Really for us, what transitory has meant is that if something is transitory it will not leave behind permanently – or very persistently higher – inflation.” On the other hand, Atlanta Fed president Raphael Bostic has criticised the FED’s choice of words arguing that supply chain disruptions pushing up the prices are expected to linger, which “by definition” renders the forces “non-transitory.”

Moving forward, all eyes will be on the coming central bank meetings and how decisions will change in the coming months. The ECB, Fed, BoE, and RBA are all scheduled to hold their monetary policy meetings in the first half of December. While the FOMC has signaled possible rate hikes by late 2022 or early 2023, St. Louis Federal Reserve’s James Bullard stated on Monday he believes the central bank will hike rates twice in 2022. This more accurately reflects where the markets believe the Fed is going. If inflation pressures persist longer that what central banks are anticipating, then all of them will be forced to play catch-up by reducing QE faster or raising rates sooner. Given Powell’s comments on supply chains and labor shortages existing well into 2022, we agree with the markets and Bullard on when the Fed will move and why they will remain reactive, not proactive on tightening monetary policy.