If the UK and EU don’t scale fast, their best ideas will exit to Silicon Valley or Shenzhen

The global race for dominance in artificial intelligence (AI) is largely defined by the rivalry between the United States and China. each respectively making innovations and developments within the industry. However, whilst the spotlight may focus greatly on these two AI titans, the United Kingdom (U.K) and European Union (E.U) have set ambitious plans to establish themselves as significant AI powers. While their strategies differ—the UK favouring agile innovation and the EU championing robust regulation—both are constrained by a shared set of structural hurdles. These include critical infrastructure deficits, intense competition for capital and talent, and a lag in AI adoption, which collectively threaten their goal of achieving technological sovereignty.

Key Takeaways:

🚦UK hits the gas, EU lays the guardrails: The UK’s pro-innovation blitz—backed by billions for compute, talent, and startups—clashes with the EU’s regulation-first AI Act. One’s building a racetrack, the other’s perfecting the rulebook.

🧠Brain drain meets data drain: Top-tier AI talent is flocking to Silicon Valley while Europe and the UK outsource critical compute to U.S. hyperscalers. It’s hard to win the AI race when your team and toolkit live overseas.

🏗️Infrastructure: the hidden bottleneck: Without sovereign supercomputing and cloud capacity, both the UK and EU risk becoming renters in the AI economy—dependent, reactive, and digitally vulnerable.

🏭SMEs stuck in slow gear: Niche AI success in auto, MedTech, and fintech can’t mask the bigger problem—99% of EU and UK businesses (SMEs) are falling behind. A two-speed AI economy is already forming.

💸VC gap is a scaling trap: While U.S. AI startups feast on $100B+ in capital, EU and UK ventures starve for late-stage funding. Without bigger bets and bolder backing, promising firms risk being poached—or folding entirely.

Technological and Regulatory Landscape

The UK’s AI Opportunities Action Plan was unveiled in January 2025, emphasising a “pro-innovation” government approach to the rapidly changing AI industry. During London’s Tech Week, we saw this “pro-innovation” approach reinforced, with Prime Minister Keir Starmer emphasising a plan to embed AI across all sectors of work. During his opening speech, the PM highlighted four key areas that would boost the UK’s status, becoming an “AI maker not an AI taker”:

- A £1 billion government-backed pledge to boost high-performance computing capacity by twenty-fold in preparation for a larger AI industry.

- Digital and AI training programs, aimed at educating individuals from school to workforce including “TechFirst”, a £187 million program for secondary school students teaching AI and digital skills, alongside training programmes delivered in partnership with large tech firms and upskilling initiatives through partnerships with major tech companies, with the potential to upskill 7.5 million workers by 2030.

- Government-industry partnerships to create a sovereign AI industry forum, attracting investments from companies such as Nvidia, BAE Systems, BT, Babcock, Oxford Ionics, Graphcore, and ARM. The Turing Institute already plays a central role in AI research, law, and ethics, and could become instrumental in AI deployment across sectors.

- Regulatory streamlining to unlock innovation, including the Planning and Infrastructure Bill and the AI tool “Extract”, currently being tested by UK councils. These measures aim to expedite approvals for data and R&D facilities. Regulatory testbeds also allow companies to trial high-risk AI systems under real-time regulator oversight—balancing innovation with safety.

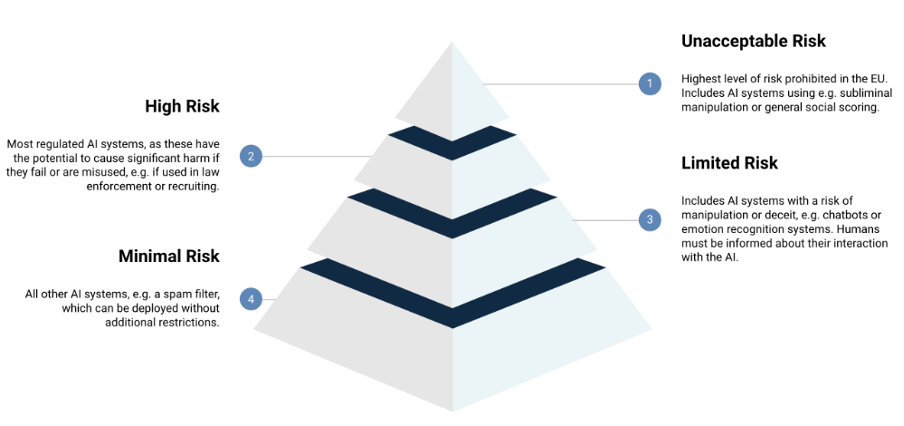

Alternatively, the EU’s approach stands in sharp contrast, positioning itself as a global regulatory superpower. This is exemplified by the EU AI Act, a risk-based framework that imposes progressively stricter requirements depending on the system’s risk level. The framework classifies AI into four tiers: Unacceptable Risk, High Risk, Limited Risk, and Minimal Risk. By prioritising oversight, data protection, and ethical safeguards, the EU aims to establish a global “AI gold standard.” To ensure compliance, the European Artificial Intelligence Board (EAIB) has been established as a supranational authority

To ensure compliance, the European Artificial Intelligence Board (EAIB) has been established as a supranational authority responsible for overseeing implementation, harmonising enforcement across member states, and providing guidance to both startups and multinational companies.

Figure. 1. Source: trail (2023). EU AI Act: How risk is classified.

While the EU’s strategy has a large regulatory aim, it has gathered substantial funding from channels such as, Horizon Europe and the Digital Europe programme, to help start-ups and initial investments. Furthermore, some EU nations have already made national-level investments that work in harmony with the EU’s AI regulatory mission, such as Germany’s “AI Made in Germany” strategy and France’s “France 2030” industrial renewal program. Underpinning these commercial and industrial efforts are academic unification through EU institutions such as the European Laboratory for Learning and Intelligent Systems (ELLIS) and CLAIRE, which work in harmony to create a cross-border unified research environment, which drives collaborative research and development across its 27 member states.

As we can see, the UK and EU have key philosophical differences in their AI approaches. The UK favours a more pro-innovation approach, with agile regulation to enhance innovation and spark rapid development. On the other hand, the EU prioritises creating a robust AI standard of regulation, collaborative research, and interconnected projects.

These two diverging ideological goals can be attributed to the effects of Brexit, which have greatly shaped the UK’s politics to have a more nationalistic orientation, focusing on self-development rather than strengthening co-operation with other nations within the EU. As a result, this does give the UK more liberty, agility and adaptability to achieve its goals, alongside faster response to unseen complications in the future. On the contrary, the divergence from the EU could lead to the UK creating risks of misalignment on data governance and technical standards compared to the EU. Whilst the UK does currently uphold data adequacy with the EU, the new Data (Use and Access) Act 2025 departs from certain criteria of the EU. One example is the UK’s approach to “legitimate interests” as a legal basis for using personal data.

.Under GDPR rules, any organisation wanting to use personal data based on legitimate interests must perform a “balancing test“, where the individual’s fundamental right to privacy is weighed against the organisation’s interest. The UK’s new act introduces a list of ‘Recognised Legitimate Interests’, in which no balancing test is required. This change is built to alleviate administrative pressure and streamline business practices within the UK, however, from the EU’s perspective, this could lead to the weakening of data safeguards and the protection of individual rights. As a result, changes like these can fracture the flow of data that is essential for training and deploying AI models across the UK-EU border, posing a serious challenge, as regulatory and standards-based friction could undermine the competitiveness of both regions in the global AI market.

Market Dynamics and Strategic Challenges

Whilst both the UK and EU have world-class research institutions and extensive planning to reach their desired goals, both face significant market-based and structural hurdles. One common issue is the UK and EU’s ability to compete with already established AI superpowers, such as the U.S. and China.

The most critical issue lies in the scale and speed of capital deployment. The U.S. continues to dominate global AI venture capital, capturing more than 50% of worldwide AI investment in 2024, with over $109.1 billion raised, primarily by a handful of Silicon Valley giants and aggressive late-stage venture capital firms. Meanwhile, China, though opaque in its disclosures, leverages state-led megaprojects and a highly coordinated public-private financing model to rapidly deploy AI at scale, particularly in surveillance, fintech, and logistics.

By contrast, European and UK startups often struggle to raise growth-stage funding beyond Series B, a phenomenon known as the “valley of death.” While early-stage innovation is strong—fueled by universities and deep tech incubators—scaling remains a key bottleneck. This lack of scale-up capital risks losing promising AI ventures to U.S. acquirers or forcing them to relocate operations abroad in search of funding.

Economics

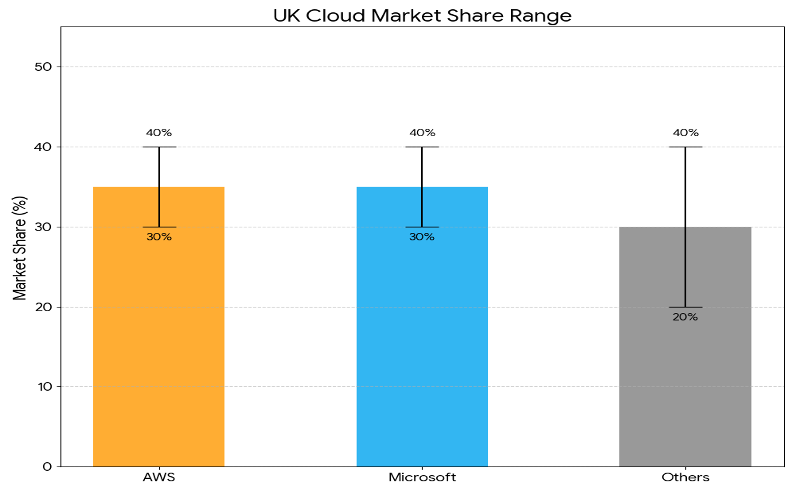

Economically, both the UK and EU are highly constrained by significant lag in sovereign computer infrastructure, both relying heavily on large scale GPU clusters and advanced AI cloud systems. As a result, Europeans often rely on the services of the “big three” hyperscalers: Amazon Web Services (AWS), Microsoft Azure and Google Cloud Platform (GCP) all of which are made in America. Within the UK, a research by the UK’s Competition and Markets Authority (CMA) listed AWS and Microsoft as being the top two providers of such service, each having a market share of 30%-40%. Their second closest competitor was Google, which has a much less substantial share in comparison, after which came smaller providers. This data can suggest the formation of a duopoly within the U.K market, with AWS and Microsoft controlling a combined potential of 60%-80% of the market.

This reliance is not just a matter of market preference, but one of foundational infrastructure. AI development, especially the training of large language models or computer vision algorithms, requires access to vast computational power and low-latency cloud infrastructure. Currently, no British or EU-based provider can match the speed, scale, or global reach of U.S. hyperscalers. This technological gap is not merely commercial—it has strategic ramifications. AI compute resources are quickly becoming a geopolitical asset like oil or rare earth minerals, and nations that lack sovereign capacity may find themselves at a disadvantage in setting global norms, enforcing national security protections, or even ensuring economic resilience during crises.

Figure. 2. Source: Competition and Markets Authority (2025). Cloud services market investigation: provisional findings.

Within the 2024 EU market, we see a similar market dominance. AWS, Microsoft, and GCP dominate the EU market as shown by the IDC MarketScape for European Public Cloud IaaS 2024 Vendor Assessment. This chart also illustrates how local EU providers have very little share within the market, making it a challenging landscape for them to effectively compete on scale against the US-based hyperscalers. While providers such as OVHcloud (France), Deutsche Telekom’s T-Systems (Germany), and IONOS (Germany) are making targeted efforts to expand their AI-oriented services, their progress has been incremental due to regulatory fragmentation, uneven national investment levels, and limited R&D budgets. These providers are often confined to niche markets or national public sector contracts, preventing them from scaling across borders. Additionally, European firms face difficulty matching the flexible pricing, developer ecosystems, and platform integrations offered by U.S. hyperscalers—factors that are critical for AI-driven businesses to thrive.

Figure 3. Source: IONOS Group (2024) IONOS Corporate Brochure.

The dependency on these foreign U.S. companies is immense in both the UK and EU markets. In turn, this situation creates a large competitive gap that makes it difficult for any local UK or EU companies to develop, scale and achieve international success, reinforcing the U.S. dominance of large-scale GPU clusters and advanced AI cloud systems markets. The issue is compounded by the fact that AI models trained on foreign infrastructure may be subject to extraterritorial laws such as the U.S. CLOUD Act, which grants American authorities the power to access data stored by U.S.-based tech firms—even if that data resides on servers in Europe.

While PM Starner has announced positive action towards the UK’s goal for AI improvements alongside a £2.2 billion budget, such infrastructure could take years before any notable progress is fully made (that is, without any unforeseen issues). Moreover, the country’s “scale up” problem could greatly undermine startups, potentially moving business abroad where already established and tested infrastructure is working with better cost efficiency. Alternatively, whilst the EU’s expected €200+ billion budget for AI infrastructure greatly surpasses the UK’s, it is split amongst all 27 of its members, making it difficult to create large-scale, high-risk investments that are commonplace in the U.S. and China.

Politics

From a political perspective, both the UK and EU must face some considerable barriers if they wish to achieve their desired goals and ambitions within the global AI tech space. Whilst some of these challenges may vary, they both share a struggle to maintain competitiveness against the tech giants U.S. and China.

For the UK, Brexit’s changes to free movement have restricted a large flow of talent and labour coming into the country, as observed by the Migration Advisory Committee (MAC). Moreover, this change has also affected the previous relationship of research collaboration between the EU, resulting in a “Brain drain” with academics going abroad for further opportunities, leaving behind a diminishing pool of UK based academics. Consequently, the focus of establishing a talent pipeline as the PM highlighted, is vital if the UK wishes to become an established innovator of AI or provide an AI service.

Similarly, though the EU is formed of 27 nations, it likewise suffers from a diminishing pool of researchers leaving towards the U.S. and China. As shown by Marco Polo’s 2022 Global AI Talent Tracker, the U.S. and China are currently the top two destinations for top-tier AI talent, with 69% of the labour market seeking to work in either of these countries.

Figure 4. Source: MacroPolo. (2024). The Global AI Talent Tracker 2.0 – MacroPolo. [online]

This struggle to retain talent is made more acute by a significant internal issue: the EU’s own regulatory-first approach. While well-intentioned, it poses a dual risk. Firstly, it may impede domestic innovation by limiting research agility, in turn increasing operational costs that can hinder any competitiveness. Furthermore, a failure to harmonise these regulations with commercial realities could trigger a flight of business and investment from the continent, benefiting American and Chinese tech giants who already dominate these areas.

Ultimately, these distinct problems converge on a single, critical vulnerability. For the UK, the issue is a shrinking talent pool; for the EU, it is the risk of over-regulation. Both scenarios, however, lead to the same outcome: a diminished capacity to innovate at pace and scale. This geopolitical squeeze threatens to relegate both the UK and the EU to the status of digital dependents, reliant on technologies developed and controlled elsewhere, rather than being the masters of their own technological destiny.

Private Sector and Adoption Gaps

Further beyond the political and infrastructural dependencies, the private sectors of the UK and EU are where both groups show their greater strengths, and if correctly managed, can create AI market footholds in this duopoly.

As previously mentioned, the UK excels in having a central political power promoting AI innovation and deployment with large liberty, agility, and adaptability to achieve its goals. Fast sectors such as finance, healthcare, and government technology, are key areas that the UK has already seen AI success. Projects such as Hertha, a fintech AI, have found 12% more illicit bank accounts compared to conventional methods and a 26% improvement in spotting new and previously unseen patterns of financial crime, ultimately making the investment worthwhile. Similarly, MedTech technologies like Mia have reduced workloads and enhanced treatment care for patients, showing the potential of developing more specialised AI within newer markets.

These niche market developments are not only impactful to innovation and development but can be financially promising. Niche markets like fintech are generating a total turnover of £220.5 billion, growing at 9.4% per year alone within the UK. Moreover, MedTech is reaching £36.9 billion total turnover, growing at 14% per year, underpinning the UK’s position as a potential sector-specific innovation.

Parallel to this, the EU has also been utilising its strengths through three established nations, Germany, the Netherlands and France, applying AI to traditional industrial sectors, particularly automotive manufacturing, advanced engineering, and logistics. Rather than attempting to replicate the same consumer-tech focus of Silicon Valley within the EU, these nations already have established industrial sectors, instead concentrating on leveraging AI to boost the productivity, precision, and efficiency of these sectors.

One notable example is Germany, a nation with a rich automotive industry, which has committed to securing €5 billion in investments by 2025 for AI to improve its automotive industry. BMW has already noted its intention to use AI as a “quality booster” through a custom AI model “GenAI4Q”, streamlining quality inspections, raising accuracy, and ultimately producing a better-quality car for the customer.

Similarly, France’s 2030 investment plan and the Netherland’s Strategic Action Plan for Artificial Intelligence both signal for the adoption and innovation of niche industrial AI, with companies such as The Renault Group and ASML both stating their effectiveness in operation quality, real time decision making and cost reduction. Moreover, France also pioneers some of the most cutting-edge aviation technologies with “skywise” an AI tool created by Airbus to centralise, analyse, and optimise aircraft data across airlines, creating a live portfolio of aircrafts and their analytics. In turn, this enables a more efficient system that supports predictive maintenance, streamlines operations, and enhances safety, not just for individual aircraft but easily managed across an entire fleet within the aviation ecosystem.

Figure 5. Source Aviation Today, W.B. (2021). GE Joins Airbus Digital Alliance to Expand Predictive Aircraft Maintenance Scope of Skywise.

Whilst these niche AI projects are not aimed at replacing the scale or dominance of the U.S. and China, they do represent a strategic advantage that the UK and EU have of integrating specialised AI into their already established sectoral strengths. Through the specialisation of solving specific, high-value industrial, healthcare and financial challenges, intertwined with regulatory AI development, the European region could become a producer and leader of trustworthy, efficient and sector-specialised AI, establishing market footholds in the global AI market that is dominated by superpower-scale initiatives.

These targeted applications serve as early proof-of-concept models that can later be scaled horizontally across related industries. For example, AI systems designed for predictive maintenance in aviation can be repurposed for rail, shipping, and logistics, creating value chains that amplify both economic return and technological adoption. If nurtured through public-private partnerships, strategic procurement policies, and tailored venture support, these niche applications could generate broader AI ecosystems rooted in Europe’s industrial base—an approach that stands in contrast to the consumer-dominant AI strategies seen in Silicon Valley.

However, while these niche initiatives may be successful, these plans offer limited scalability and potential global reach compared to Silicon Valley or Shenzhen, which control large amounts of AI resources. This “scaling up” problem ultimately stems from the UK and EU’s fragmented markets and a less mature venture capital ecosystem for late-stage growth. Subsequently, this creates a slow growth trajectory for these markets, hindering promising AI startups and innovations from developing into a market dominant enterprise. As a result, these companies will have a limited long-term economic influence and job creation, rather than being a catalyst in driving broad scale technological leadership over time.

Consequently, this limited scalability not only hampers innovative individual startups but also reinforces a structural issue of uneven distribution of AI across the private sector. The advancement of AI tools used by Airbus, BMW, ASML and more, remains largely out of reach for the small and medium sized Enterprises (SMEs), which represent 99% of all businesses in the EU and 99.8% in the UK. These SMEs are crucial to local economies within their respective nations but do not have the same calibre of funding nor digital skill vs. large enterprises, often having uncertainty about their return on investment. This technological gap creates a two-speed economy: where a handful of highly productive, AI enabled enterprises, lead the economy, whilst a “long tail” of SMEs that represent 99% of the economy and employment struggle to keep pace, risking stagnation and reducing competitiveness. Ultimately, this weakness leads to both the UK and EU blunting the global competitive edge of adopting niche innovations and represents a fundamental barrier to long-term competitiveness.

VC in AI

The flow of venture capital is vital for the global AI market. Investment trends indicate where markets are most vibrant and where investors expect growth and innovation.

At face value, it is no surprise that large amounts of investment are being directed towards the tech giants in the U.S. and China, setting a difficult environment for both the UK and EU to attract the scale up funding necessary to establish themselves for global competition. In 2024, Pitchbook found globally one in every three dollars was invested into an AI start up, leading venture capital investments in AI to reach over $180 billion USD. From the Stanford University’s index 2025 report, we can see the U.S. is the current leader for investment, securing $109.1 billion. Second was China at $9.3 billion, followed by the UK at $4.5 billion. To complete the European picture, the EU’s leading nations, Germany and France, attracted approximately $2.1 billion and $1.6 billion.

This immense venture capital fund gap greatly shapes the processes of development, deployment and commercialisation of AI technologies. The influx of capital allows the American ecosystem to rapidly hasten its innovation cycles, attracting top-tier global talent. In turn, this secures critical computational resources, such as the vast fleets of advanced GPUs, cloud computing infrastructure and large-scale, high-quality datasets required for training models. With access to all these resources, the U.S can reinforce their position as leaders of cutting-edge AI technology. This is particularly evident as the U.S. is home to many of the world’s leading AI labs, powered by two distinct but complementary engines: venture backed pioneers like OpenAI, Anthropic, and xAI, alongside the immense R&D budgets of tech incumbents like Google DeepMind and Meta AI. These companies have not only kept the U.S as a leader of foundation next-generation global applications and businesses but have reinforced their dominance in the cloud services market.

On the other hand, China’s approach to cultivating an AI industry contrasts heavily with the U.S. model of venture capital investments; instead many startups rely heavily on state-led directives and utilise strategic industrial policy. This top-down coordination, first detailed in the government’s ‘New Generation Artificial Intelligence Development Plan‘, has mainly focused state resources on developing AI in surveillance, manufacturing, and the creation of national AI platforms. One notable example is the China Integrated Circuit Industry Investment Fund, also known as the “big fund”. Through multiple phases, the fund has a registered capital of 344 billion yuan ($47.5 billion) with the initiative to develop and expand AI manufacturing of third-generation semiconductors, high value-added DRAM chips and semiconductor equipment and materials to become a more self-reliant sovereign power in AI and chip making industry.

In 2024, China attracted $9.3 billion in venture capital, but this funding is closely tied to state priorities, aligning private investment with national goals and long-term planning. This integration of private and public funding is further exemplified by China’s “AI Champions” programme, where select tech companies such as Baidu, Tencent, Alibaba, and iFlytek are designated to lead R&D in specific verticals like natural language processing, autonomous vehicles, and smart cities. These firms receive privileged access to government contracts, data repositories, and high-priority regulatory approvals. In effect, the Chinese system is designed not just to fund innovation, but to orchestrate it across a nationally aligned industrial policy. This approach has proven effective in scaling AI for internal market dominance and infrastructure optimisation, particularly in AI-powered surveillance, urban planning, and public services.

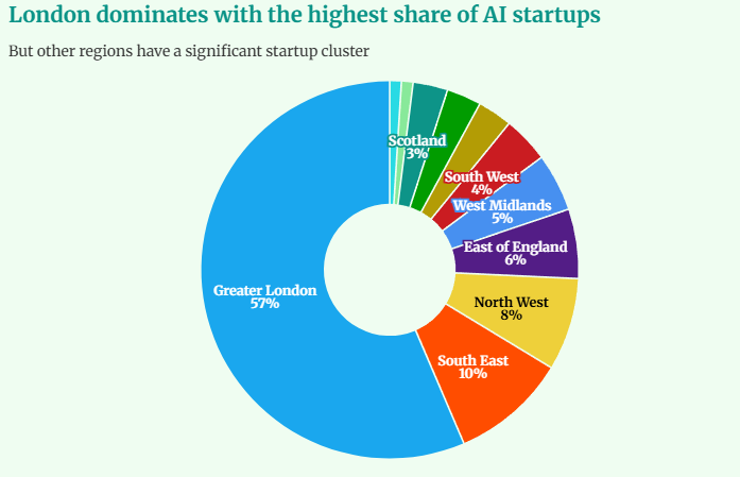

Through analysing these two tech giants, the U.S. venture backed power and the Chinese state-driven approach, we can better understand how the UK and EU seek to expand their presence within the global AI space to receive more income flow of venture capital funding. In the UK, investment is active, with artificial intelligence startups raising $4.2 billion in AI venture capital in 2024. This can be attributed to the approximately 3,300 AI tech start-ups based in the UK (of which 1,650 are in London), housing many DeepMind spinoffs that attract promising early funding.

Figure 6. Source: Hunt, S. (2025). AI startup creation rose to fresh highs in Q4 as regions outside London catch up.

Whilst this flow of income is substantial compared to the UK’s market size, there is an uneven investment distribution, with many of these investments being made at the “seed stage” but far less available at later stages of growth. According to the British Business Bank’s Small Business Equity Tracker 2025, nearly half (48%) of state-supported deals were at the seed stage, while only 41% were at the venture stage, highlighting a clear scale-up funding gap.

To address this, the government has launched a two-pronged strategy. The Mansion House Accord which seeks to unlock 5% of pension funds and institutional investments, equating to £50 billion worth of investment. This accord is also complemented by the newly formed Sovereign AI Unit in 2025, which pilots strategic investments in national compute power and AI infrastructure, helping scaling companies compete globally.

By taking these two initiatives alongside the UK’s new pro AI approach to laws and governance, the government is laying down the foundation to turn the UK into a small stronghold in the global AI market for niche tools and products. In turn, this not only keeps business investments within its borders, but can also attract researchers and developers, both local and foreign, to counter the ‘brain drain’ effect of the U.S. and China. This approach could potentially benefit the UK in multiple subsequent ways, creating innovation and wealth that could consequently also boost the infrastructure funding and quality across the nation. What is vital to making this plan successful is how well funding is allocated, especially towards promising startups. Without the development of flagship AI companies that can anchor long-term economic growth, the UK can lose its retention of business, research, and venture capital flow, blunting the competitive edge of the AI sector.

The EU is pushing for a much different strategy compared to the UK, leveraging the collective scale, power and regulatory prowess to shape the international market to its advantage. One of its key differences from the UK is its hybrid model of using traditionally conservative venture capital markets with assertive state-led intervention. Institutions such as the European Investment Fund (EIF, part of the European Investment Bank, EIB) aim to support SMEs by giving them financial access, acting as a financial intermediary, but not to replace private venture capital. Whilst this approach is more cautious vs, the ‘go big or go home’ Silicon Valley mindset, favouring smaller, slower, and risk-aversive investments, the benefits of these smaller investments are that risks are lower, startups have stronger financial discipline and focus on sustainable growth.

The European Union is bolstering its tech sector by investing in emerging innovation hubs, as demonstrated by a recent €90 million commitment to three Portuguese venture capital funds. Armilar Venture Partners IV, Faber Tech III, and 33N Cybersecurity and Infrastructure Software Fund are set to leverage this even further to over €400 million in total capital, fuelling tech startups within deep tech and cybersecurity startups across Europe, alongside entrusting confidence in emerging tech players like Portugal.

However, these conservative investments can be restrictive, especially across 27 nations, limiting who gets the venture capital funding for their startups. Within the European Investment Bank’s annual report 2024, this issue had been highlighted, calling for the European Investment Bank to play an “even greater role in closing Europe’s investment gap”. As a result, many EU nations have begun relying on government-backed banks from the EU’s leading nations, filling funding gaps that private investors aren’t covering. France’s Bpifrance is fulfilling this role by channeling a significant portion of the ‘France 2030’ plan’s capital—with €1 billion to be directly invested in “AI first” companies and over €3.4 billion earmarked for AI-themed projects by the end of 2024 into its domestic ecosystem. Similarly, Germany’s KfW capital is using its ‘Future Fund‘ to de-risk private venture capital and bolster sectors critical for national economic sovereignty, making €1.75 billion available to strengthen its venture ecosystem.

These National initiatives are likewise being complemented by EU-level partnerships with the private sector, aiming to establish the foundations and infrastructure for an independent digital European sovereignty. Gaia-X is one institution that is central to this effort, with the goal to create a federated, secure data infrastructure, giving European companies and citizens greater control over their data, reducing their dependency on U.S. cloud hyperscalers. This push for data sovereignty is not only a way to defend the EU market from being dominated by foreign tech giants but can also help improve security in the region’s ecosystem. By leveraging the regulatory AI Act, the EU can project its geopolitical power by establishing its independent and “trustworthy AI” vision as the global ‘gold standard’.

To fund these ambitious infrastructure programs, initiatives such as the European High Performance Computing Joint Undertaking (EuroHPC JU), are instrumental, pooling resources from the EU, member states and private partners. They aim to obtain and deploy a fleet of world-class supercomputers to establish a unified, pan-European supercomputing infrastructure. By partnering domestic researchers and businesses with access to elite computational power, EuroHPC can facilitate the infrastructure and means of training and developing sophisticated AI models, again like the UK, establishing a defensive stronghold in the global AI market.

Though the EU has many cross-border institutions with intentions that are set to benefit all its members, co-operation is vital for its success. The ultimate test will be to harmonize all multi-layered strategies, especially through unforeseen financial downturns that could reduce the spend from national entities like Bpifrance and KfW. On the other hand, it is important to ensure that the immense financial powers do not merely create national champions, concentrating AI infrastructure and opportunities in one or two nations, but foster an even European AI ecosystem.

Case Studies

By analysing case studies of the UK, Germany, and France, we can see these distinct national approaches in practice. They illustrate different strategic models, from public service innovation in the UK, to industrial integration in Germany and state-led ecosystem building in France. These real-world examples highlight the tangible opportunities and inherent limitations facing Europe’s varied efforts to secure a competitive role in the global AI market.

UK: Health, Wealth, and Opportunity

As mentioned previously, the UK government has an ambition to implement AI technology across all sectors, streamlining work processes to maximise efficiency, productivity, and overall quality of life. Expanding further into MedTech, the UK’s National Health Service (NHS) can serve as a critical testing ground.

One major hurdle the NHS system is currently experiencing is staff shortages, as noted in the NHS Long Term Workforce Plan, hindering the ability to deliver quantity and quality services to people in need, without sacrificing staff wellbeing. In turn, these issues have subsequently led to further issues, particularly, large waiting times for treatments creating a rapidly expanding backlog of patients.

Cera, a digital-first home healthcare provider, is one example of adopting AI to alleviate many of these multifaceted challenges, without directly increasing labour, nor sacrificing workers’ wellbeing. Through a Health Deterioration and Fall Prediction Tool, Cera’s AI platform analyses data from carers’ daily observations to predict health downturns and falls with 97% accuracy, potentially avoiding up to 2,000 hospital admissions per day. Not only has this helped deliver a better quality of care, but it has likewise reduced hospital pressures and saved an estimated £1 million per day by reducing A&E attendances.

Whilst this initiative had overwhelming success, the further introduction of AI in the NHS could highlight the difficulty of protecting personal data. Additionally, having more AI services embedded across the NHS would require more complex IT facilities, which may pose procurement setbacks and increase the risk of system vulnerabilities if not properly managed.

Beyond healthcare, the UK has also positioned itself as a policy innovator in AI governance. The establishment of the AI Safety Institute in 2023 marked a global first, with a remit to explore and manage risks associated with advanced AI systems. This proactive stance has allowed the UK to play a convening role in international AI diplomacy, hosting the first AI Safety Summit and engaging with partners such as the US, Japan, and the EU on foundational AI risk frameworks. Furthermore, the UK has invested in regional AI innovation hubs, such as those in Manchester, Edinburgh, and Cambridge, fostering a decentralised but interconnected ecosystem that supports both academic excellence and commercial scalability.

Yet, persistent challenges remain. A major barrier is the AI skills gap, as many sectors lack the in-house expertise required to adopt and deploy AI effectively. The UK’s Department for Education has responded by rolling out national retraining schemes focused on digital and AI skills, but uptake has been uneven across industries and regions. Moreover, while the private sector has embraced AI through fintech, lawtech, and proptech startups, public procurement processes remain sluggish and risk-averse, limiting the adoption of innovative solutions in government operations.

Germany: “AI Made in Germany”

Germany has strategically aligned its “AI Made in Germany” initiative with its world-renowned industrial prowess, focusing on its powerful automotive and manufacturing sectors. Rather than pursuing broad, consumer-facing applications, the national strategy emphasizes deep integration within its export-driven economy. Through industrial giants such as Siemens and Bosch, AI has become a tool of industrial evolution, enhancing efficiency and precision.

Figure 7. Source: Siemens. (2025). Robot dogs help the industry enhance worker safety and maintenance.

One innovative example from Siemens has been the development of AI tools such as The autonomous mobile robot (AMR), an analytic robot dog that can autonomously collect high-quality data from hundreds of inspection points. This data is then used to enable predictive maintenance planning, reducing production downtimes and maintaining high safety for workers. For Bosch, AI in manufacturing is a call for unlocking massive product potential with the AI Analytics Solution, being able to read 1 billion lines of data that ensure high quality control.

Whilst developments such as these can reinforce Germany’s position as a global leader in high-end manufacturing and engineering, there are still limitations. A strong regulatory environment, while ensuring quality and safety, may outpace the speed of innovation. In a rapidly evolving field like AI, a cautious, regulation-heavy approach could potentially slow the adoption of breakthrough technologies, putting German industry at a competitive disadvantage against more agile international rivals who favour innovation.

France

France’s AI strategy is highly centralised and state-driven, leveraging government procurement and public-private partnerships to channel resources toward strategic sectors such as health, defense, transport, and climate technology. It is deeply integrated with its ambitious “France 2030” industrial renewal program, which treats AI not as an isolated technology, but as a core driver of economic modernisation backed by significant public investment and a focus on nurturing homegrown talent. The strategy has successfully cultivated a vibrant AI ecosystem, leading to the emergence of globally recognized AI clusters with large European names such as Mistral AI, Poolside AI, and the Artificial and Natural Intelligence Toulouse Institute (ANITI), a Major hub of artificial intelligence rooted in the aerospace and specialized AI applications.

Notably, Mistral AI has rapidly achieved global prominence and attracted significant investment, positioning itself as a key European competitor, providing an arsenal of AI technologies covering a variety of industries, to excel in production within multiple sectors. However, a key limitation for France is the challenge of scale and integration within the broader European landscape. While its national strategy is fostering innovation, aligning its fast-paced, startup-friendly approach with the more deliberative, regulation-focused EU AI Act presents complexities. Effectively scaling its national champions and harmonizing its policies with those of the wider EU remains a complex task, crucial for creating a unified European front that can compete with the US and China.

Education and talent development are also central to the French approach. Through elite institutions such as École Polytechnique and INRIA, France is producing a pipeline of AI researchers and engineers. Simultaneously, vocational training programs are being modernised to provide AI literacy to non-technical professionals, ensuring that AI adoption is not restricted to a narrow elite but can permeate the broader workforce.

What’s Next

The UK and EU have both set out long term goals to establish themselves in the global AI market. However, each has taken distinct paths that diverge in their regulatory approaches, strategic priorities, and partnerships. Yet ultimately, both are determined to achieve technological sovereignty by reducing their dependency on U.S. hyperscaler cloud infrastructure and building domestic capabilities to retain long term growth.

Initiatives like the UK’s computer pledge and the EU’s Gaia-X and EuroHPC are not merely infrastructure projects. They represent a high-stakes race against time to close the competitive gap vs. the U.S and China before their dominance becomes permanent. Whilst the UK and EU share common pressure from the U.S and Chinese tech giants, mutual success could be difficult with colliding interests. The first major key separation is the UK’s Data Act 2025, particularly its departure from the EU’s GDPR’s “balancing test”, possibly breaking the flow of data between both regions—data that is essential to their respective AI ambitions. This makes collaboration more difficult at a time when unity is critical to counter external technological dominance.” This divergence could force businesses into a binary choice, undermining the creation of a pan-European market and blunting the innovative potential of both regions before they can truly compete on a global scale.

Beyond regulatory divergence, a widening gap in AI governance philosophy is emerging. The UK favours a sector-based, adaptive regulatory approach, entrusting sector regulators with autonomy to supervise AI deployment within their specific domains. This decentralised model enables quicker responsiveness to innovation yet may lack the cohesive oversight needed for cross-sectoral risks. In contrast, the EU’s AI Act enshrines a harmonised, risk-based approach, where all high-risk AI systems face pre-market scrutiny. While this creates clarity and legal certainty, it may slow deployment timelines and increase compliance burdens. This mismatch in regulatory speed and depth will have long-term implications for startups and multinationals alike when deciding where to develop, pilot, and launch AI-based services.

In a global setting, this divide translates into two competing models of influence. First, the UK markets itself as an agile, pro-innovation testbed, showcasing successes in niche sectors like FinTech and MedTech. In contrast, the EU markets itself as an exporter of a comprehensive legal framework, positioning itself as the gold standard for “trustworthy AI.”. This has led to distinct investment opportunities in each region. In both regions, heavy funding for energy and transport to meet net-zero targets, exemplified by the UK’s £46m investment in its transport-focused TransiT Hub and the EU’s ambitious, continent-spanning TwinEU project for its electricity grid.

Figure 8. Source: Thinkdigitalpartners.com. (2024). £46m investment in digital twins to decarbonise UK’s transport systems | THINK Digital Partners : THINK Digital Partners. Available at: https://www.thinkdigitalpartners.com/news/2024/08/13/46m-investment-in-digital-twins-to-decarbonise-uks-transport-systems

Additionally, using AI to empower the green transition is another key area, with governments backing AI tools to resolve and improve sustainability issues. The UK has chosen to channel grants towards AI in agriculture, while on the other hand, the EU’s GenAI4EU initiative aims to accelerate AI solutions for climate and broader environmental concerns. Crucially, recognizing that SMEs are the backbone of the economy, representing 99% of businesses, has also made them a focal point in future investments. Programmes like the UK’s BridgeAI and the EU’s extensive SME grants under frameworks like Horizon Europe can boost competitiveness. This can help ensure that the benefits of AI are distributed more evenly across the entire economy, not just large enterprises.

The long-term viability of both groups is threatened by a shared Achilles’ heel: the SME adoption gap. A two-speed economy, where AI benefits are captured only by large enterprises like the EU’s Airbus or the UK’s Revolut while 99% of businesses that form the economic backbone lag behind, creates an unsustainable model that will ultimately cripple their global competitive edge.

Ultimately, the future for both the UK and the EU hinges not on the success of any single policy but on their ability to manage multiple of these intertwined challenges.

These hurdles range from resolving the sovereignty paradox, navigating their own complex regulatory relationship without causing irreparable harm and solving the deep-seated SME innovation gap. Failure to balance these domestic and regional imperatives will see them relegated to the status of digital dependents, reliant on foreign technologies developed and controlled elsewhere, rather than becoming innovators or leaders in shaping the AI industry.

Economic Challenges in AI Leadership for the UK and EU

While the UK and EU possess significant strengths in niche AI research and a clear ambition for leadership, there are deep-seated economic challenges that could jeopardise these plans. These structural hurdles are multifaceted, involving infrastructure, capital, talent, and regulation. They pose a risk of slowing innovation, deterring investment, and widening the gap between already established AI superpowers. These barriers must be answered if the UK and EU wish to avoid being outpaced in the AI technological revolution that is occurring.

One of the primary difficulties for both the UK and EU has already been mentioned multiple times before: infrastructure. The UK and EU are highly dependent on U.S cloud service providers. Therefore, to achieve technological sovereignty and develop cutting-edge AI, there must be access to massive-scale processing capabilities that are not widely available under European ownership. This dependency not only creates an economic outflow, but also highlights a significant vulnerability regarding data autonomy, as sensitive data is processed and stored outside of their direct jurisdictional control. This situation highlights how failing to build essential digital infrastructure can threaten both digital sovereignty and economic stability.

Efforts are underway to reverse this imbalance. The EU’s IPCEI-CIS (Important Project of Common European Interest on Cloud Infrastructure and Services) aims to develop a federated European cloud ecosystem by 2030, enabling secure, sovereign data processing. Similarly, the UK’s investment in its Frontier AI Taskforce and £900m exascale supercomputing project demonstrates an ambition to reclaim control over advanced computational capabilities. However, progress remains uneven, and full independence from American hyperscalers will require years of sustained investment, industry collaboration, and international standard-setting.

Securing this funding can pose a serious challenge, especially in comparison to the U.S and China, which have larger venture capital investments and funds. For the EU, many of its initial funds are dispersed out across all 27 nations, making it structurally difficult to pool the resources necessary for the kind of long-term, large-scale investments that produce foundational AI breakthroughs. Additionally, since the UK’s Brexit departure, collaboration between Europe’s AI hubs and programs has become more fragmented, losing access to programs such as Horizon Europe that filled significant financial gaps for UK-based AI research and innovation. With less capital to spend on startups, both the UK and EU currently struggle to “scale-up” promising early-stage companies that struggle to find late-stage funding required to mature into global market leaders.

Moreover, European pension funds and institutional investors—key backers of long-term innovation capital—tend to adopt conservative investment strategies, preferring stable returns over high-risk tech ventures. This cultural and institutional risk aversion limits the growth of venture capital ecosystems in both regions. Without mechanisms to mobilise domestic capital at scale—such as tax incentives, sovereign wealth initiatives, or innovation bonds—Europe and the UK risk becoming incubators for innovations that are ultimately commercialised and scaled elsewhere.

Alongside needing infrastructure to develop and innovate within the AI field, researchers are a central piece. Europe is a world-class producer of AI talent, with many institutions across the continent involved with cutting-edge research and training highly skilled professionals. However, it faces a constant struggle to retain these intellectuals. This is in part because of the larger work opportunities in the U.S and China, offering financially backed and well-resourced environments. Likewise, another contributing factor to this high talent migration is internal frictions within the UK and EU, where bureaucratic rigidities and less flexible labour markets can hinder the ability of homegrown startups to hire and expand at the speed necessary to compete for elite talent.

Adding to this challenge is the relatively limited number of flagship AI employers in Europe. While the U.S. offers graduates career trajectories at OpenAI, Nvidia, or Google Brain, European graduates often find few domestic equivalents offering competitive compensation, impact scale, or global recognition. Until more global tech leaders emerge within the UK and EU, stemming the talent outflow will remain an uphill battle.

The drive to establish a global benchmark for ethical and trustworthy AI, while commendable, does carry inherent economic trade-offs. A complex regulatory environment can impose significant compliance costs and create high barriers to market entry, disproportionately affecting the small and medium-sized enterprises that are vital for a dynamic innovation ecosystem. (See Mario Draghi’s plan for EU growth)Furthermore, the divergence in regulatory philosophy between the UK and the EU does pose a risk in creating market and other friction, potentially reducing the interoperability that is essential for a fluid, pan-European digital market.

Perhaps the most critical long-term threat is the deep chasm in AI adoption within the private sector. While flagship enterprises have begun to integrate AI to great effect, many businesses—the SMEs that form the backbone of the European economy—are being left behind. This lag is not merely a matter of hesitancy but a result of structural barriers, including a lack of skills, capital, and clear implementation pathways. This creates a dangerous “two-speed” economy, where the productivity benefits of AI are concentrated in a small number of large firms, while the wider business landscape stagnates. Such a model is unsustainable and ultimately cripples the region’s collective competitive edge.

Closing this adoption gap requires more than subsidies—it demands structural reform. Integrating AI literacy into vocational training, offering procurement incentives for SME digital upgrades, and mandating public-sector AI adoption to lead by example are all part of the long-term solution. Without bold action, the UK’s and EU’s AI ambitions will remain aspirations, rather than a lived industrial reality.

Wrapping Up

The UK and EU are in a race against time to establish their AI presence in the global market. Both have charted distinctly different courses. The UK has championed taking agile, “pro-innovation” policies, whereas the EU’s ambition to become a regulatory superpower has resulted in a more cautious approach. Despite these philosophical divides, both share the critical goal of achieving technological sovereignty, reducing their heavy reliance on US and Chinese infrastructure. However, this ambition is threatened by a formidable set of shared challenges: a significant infrastructure deficit, a persistent ‘brain drain’ of top talent, and a venture capital landscape dwarfed by global rivals.

The UK-EU relationship itself, strained by regulatory divergence such as the UK’s Data Act 2025, risks fragmenting the European market when unity is paramount. Yet, the most profound threat to both is internal: the gaping chasm in AI adoption between a few large enterprises and the small and medium-sized enterprises (SMEs) that constitute 99% of their economies. This creates an unsustainable ‘two-speed’ economy, blunting their overall competitive edge.

This disparity is already reflected in productivity and innovation outputs. Large firms like Airbus and Rolls-Royce are successfully leveraging AI to streamline operations, accelerate R&D cycles, and expand into new markets. In contrast, SMEs—particularly in traditional sectors such as logistics, retail, and manufacturing—often lack the digital literacy, financial capacity, or institutional guidance to adopt even foundational AI tools. This polarisation not only limits inclusive economic growth but also stifles the innovation spillover necessary to build resilient, sector-wide ecosystems.