Can the West survive Beijing’s export-or-collapse gamble?

China’s identity as the “world’s factory” is undergoing a massive transformation. The global economy is bracing for ‘China Shock 2.0,’ not a just flood of cheap goods as in the past, but a sweeping, state-driven push to dominate future-facing industries with advanced technologies, delivered at a scale few can match. China Shock 2.0 represents a huge leap into high-value industries, including renewable energy, semiconductors, AI, and EVs. These are sectors that Western nations consider strategic to their economic futures.

However, this surge in exports isn’t just a display of strength; it’s a high-stakes gamble fuelled by deepening domestic troubles. These internal strains expose the fragility of Western efforts to decouple, highlighting just how deeply entwined global supply chains remain and the risks that come with that dependence.

As author of “Breakneck” Dan Wang puts it, “China has shifted from importing technology to producing it at scale. The West still underestimates how fast its engineers can learn and build.” This shift makes detachment harder, and the stakes higher.

This begs the question: can the West truly detach from this dependency, and will China continue to export both goods and deflation? Western leaders must balance a complex policy trilemma, where they must protect domestic industries, manage inflation, and maintain alliances. This article unravels these challenges by examining:

- China’s Factory Blueprint: Analysing the four pillars of China’s manufacturing anatomy: state-directed capitalism, massive infrastructure, a unique industrial ecosystem, and ambitious long-term strategies.

- Global Trade Imbalances: Examining the resulting trade distortions and the original “China Shock” that followed, leading to the deindustrialisation of Western economies.

- The West Pulls Back: Exploring the diverging detachment strategies of the West- the U.S.’s “hammer,” versus the E.U.’s “scalpel”- and the corporate response of regionalising supply chains.

- EVs: China’s Power Play: The electric vehicle market serves as a case study to illustrate the global dilemma between adopting affordable green technology and protecting domestic industries.

- Crisis at Home, Deflation Abroad: How China’s domestic crises are forcing it to export deflation by flooding global markets with overproduced, high-tech goods.

- Policy Trap: Outlining the policy trilemma facing Western leaders, who must balance industrial protection, inflation, and international alliances.

China’s Factory Blueprint

It is no secret that China’s dominant lead in manufacturing has created unprecedented wealth for the nation and growth for its economy. China accounts for approximately 30% of global manufacturing output as of 2024, but beyond sheer size, it has employed a coordinated approach that has allowed it to move up the value chain at unprecedented speed. These large growths can be linked to four key pillars: a system of state-directed capitalism, massive investments in infrastructure and a vast skilled labour force, ecosystem advantage, and their ambitious long-term strategies. Analysing these four areas can help us to understand the anatomy of China’s manufacturing and ultimately how it became ‘the world’s factory’, shaping global trade and economic dynamics.

State-Directed Capitalism.

China’s manufacturing process is no accident or stroke of luck but has come from its deliberate and sustained use of state-led capital directed towards manufacturing industries. The foundation for this economic transformation was the “Reform and Opening Up” policy in 1978, which introduced market forces to drive growth, foster competition, and attract foreign investment. However, the real manufacturing boom in China came when the nation entered the World Trade Organisation (WTO) in 2001, creating the “China Shock”- a period of explosive growth that saw China rapidly outpace all other industrial nations. The WTO entry allowed China unprecedented access to global markets, taking advantage of its low wages and business-friendly regulations to become the go to destination for manufacturing.

The magnitude of this transformation is staggering. Between 1995 and 2023, China’s share of global manufacturing output surged from approximately 5% to nearly 35%, while its share of global exports rose from 3% to 20%. And it’s projected to grow to 45% by 2040. This represents one of the most rapid and substantial shifts in global manufacturing capacity in modern economic history, with China becoming the world’s largest manufacturer within two decades.

Figure. 1. Source: The SAIS Review of International Affairs. In Hindsight: Evaluating the Complex Legacy of China’s WTO Accession.

Crucially, this global rise was not driven by market access alone. China’s state support acted as a cornerstone in implementing industrial policy, nurturing, and protecting its domestic industries. Through direct subsidies, tax rebates, and the creation of a protected domestic market, local companies were able to scale and mature before facing global competition. One of the most potent tools in this arsenal has been the tax structure, particularly the 0% Value Added Tax (VAT) on exports, incentivising manufacturers to sell their goods abroad. All of this entwined has led to the creation of many manufacturing industries, such as China Railway Rolling Stock Corporation (CRRC), BYD and CATL that have established a global presence. CRRC is the world’s largest rolling stock manufacturer by revenue. BYD has become the world’s largest electric vehicle manufacturer in 2024, surpassing Tesla in production with 1.78 million vehicles produced. CATL dominates global battery production with a 37% market share. These examples demonstrate how state support can create globally dominant champions in strategic industries.

Infrastructure and labour.

While these industrial policies have given strategic direction, China has held another ace up its sleeve to achieve these goals: a colossal labour force and world-class infrastructure. To fully optimise this labour force, China has extensively invested in creating a logistical network designed to minimise lead times and reduce operational costs to an absolute minimum.

This includes the development of some of the world’s busiest and most efficient ports, such as Shanghai, handling 50 million twenty-foot equivalent unit containers (TEUs), and Shenzhen, 33.38 million TEUs, acting as global gateways for the seamless flow of goods. To put this in perspective, Shanghai alone handles more container traffic than the top five U.S. ports combined. This advanced logistics infrastructure ensures that raw materials can be brought in and finished products shipped out with unparalleled speed and efficiency, a critical advantage in the fast-paced world of global supply chains.

Beyond ports, China has built the world’s most extensive high-speed rail network, spanning approximately 48,000 kilometers as of 2024. This network connects manufacturing centers with ports and major cities at speeds up to 350 km/h, enabling efficient transportation of components and goods across the country.

Complementing this physical infrastructure is China’s vast human capital. The country maintains one of the world’s largest manufacturing workforces, historically benefiting from significantly lower labor costs compared to Western nations. This cost advantage remains substantial: while U.S. production and nonsupervisory manufacturing employees earned an average of $26.60 per hour in 2024, Chinese manufacturing workers earned approximately $6.80 per hour (based on an annual average of ¥107,987 in a standard 40-hour work week). For context, the U.S. is the world’s second-largest manufacturing nation after China.

Figure 2. Source: National Bureau of Statistics of China. National Data.

Additionally, this human capacity is evolving to meet further needs. China is producing a more talented and educated workforce, with an expected 12.22 million educated individuals entering the market in 2025. This shift from a purely low-cost labour model to one that incorporates higher skills, and technical expertise allows China to move up the value chain, competing in more advanced manufacturing markets.

Ecosystem Advantage.

With these attributes, China has established a highly developed and specialised ecosystem of industrial clusters for manufacturing that is simply too good to pass up on. This is not just a collection of large industrial factories, but a one-stop environment where suppliers, manufacturers, and service providers are all geographically concentrated with seamless coordination and efficiency. What makes these clusters truly unique is their deep supply chain integration. A single cluster might house everything from raw material processing to final assembly, quality testing, packaging, and even financial services, creating an ecosystem density that reduces transaction costs and accelerates innovation cycles.

The city of Shenzhen is one example where we can see this industrial cluster. Dubbed as the “Electronics Capital of the World,” Shenzhen is ranked the world’s second largest innovation hub for Science and Technology in 2024. As a central hub, it offers unparalleled access to a vast array of components- often just a few cities block away. In Shenzhen’s Huaqiangbei district, one of the world’s largest electronics market, entrepreneurs can source virtually any electronic component within a few city blocks, prototype new products in days rather than weeks, and scale to mass production without leaving the city. This hyper-concentration fuels the acclaimed “Shenzhen Speed,” allowing companies to move from concept to mass production at an unimaginable pace.

The ecosystem effect creates powerful network externalities: as more companies cluster together, the value proposition for each individual company increases exponentially. This creates what economists call “agglomeration economies,” where the whole becomes dramatically greater than the sum of its parts. The result is that even as labor costs rise, the total cost of production often remains competitive due to reduced logistics, coordination, and time-to-market expenses.

As a result, companies such as Apple, whose success hinges on the mass production of high-quality technologically advanced devices, view this ecosystem as invaluable to their business model. A Nikkei Asia analysis of Apple’s supplier list, published in 2024, revealed that despite efforts to expand into other low labour cost nations like India and Vietnam, Apple’s reliance on Chinese suppliers has actually deepened. This highlights how large-scale Chinese manufacturing services are not easily transferable, especially when manufacturing complex products like those of Apple. This effectively ‘locks in’ major global manufacturers, not through a contractual obligation, but through the sheer competitive advantage, scale, and efficiency that China’s industrial ecosystem provides, ultimately making relocation a costly proposition for both the brand and consumer.

Strategies and Goals: MIC2025 and the Belt and Road Initiative

China’s state planning has led it to benefit from becoming ‘the world’s factory’; however, the nation’s manufacturing ambitions are not done yet. The most prominent of these is the “Made in China 2025” (MIC2025) initiative. Originally launched in 2015, this ambitious 10-year plan is now in its final year, having strategically focused on transforming China from a low-end manufacturer into a high-tech powerhouse across 10 key sectors, including next-generation information technology, robotics, electric vehicles (EVs), and biotechnology. As the initiative approaches its 2025 deadline, its extraordinarily ambitious target of achieving 70% self-sufficiency in high-tech components has driven nearly a decade of massive investment and research, fundamentally reshaping China’s technological ecosystem and reducing its reliance on foreign technology[GS1] .

The success of MIC2025’s decade-long implementation can be clearly seen in the EV industry, where sustained government support has yielded remarkable results.

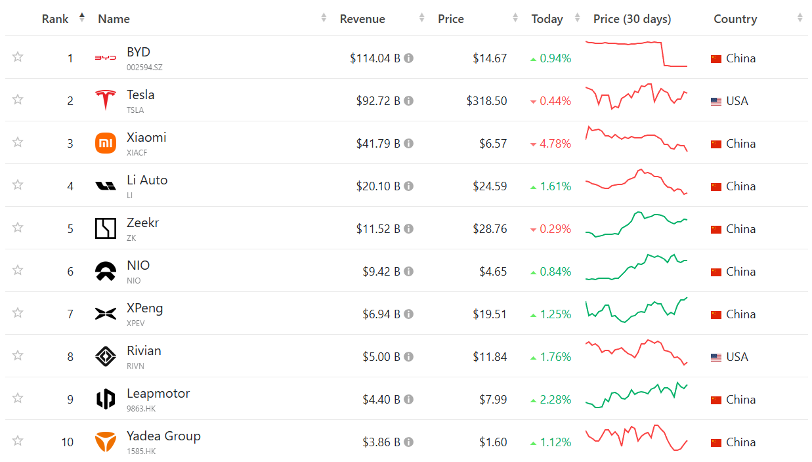

Figure 3. Source: Companies Market Cap. Top publicly traded electric vehicle companies by revenue.

From the chart, we can see how out of the top ten highest EV revenue companies, eight are Chinese, with little competition from other nations. The innovations created by the MIC2025 initiative have created a perfect environment for many Chinese companies to rapidly develop and expand. Again, this transition from low-end manufacturer into a high-tech powerhouse has positioned China as a global leader in the EV industry.

Complementing this internal industrial strategy is China’s monumental geo-economic project, the Belt and Road Initiative (BRI). The BRI is essentially China’s plan to create a modern-day Silk Road, connecting regions and their domestic resources internationally. This includes massive investment in the construction of ports, railways, roads, and pipelines in over 150 countries across Asia, Africa, and Europe. In return, China has secured two advantages; first, they have established vital access to natural resources such as raw minerals and energy sources to continue feeding the large appetite of the high-tech sectors prioritised under MIC2025. Secondly, China has cemented even further their position as the ‘world’s factory’ through infrastructure dependency, positioning China as a central hub in global trade and development. Together, MIC2025 and the BRI represent a clear and coordinated strategy to not only maintain but elevate China’s position in the global manufacturing hierarchy for decades.

The Trade Imbalance

From analysing China’s trade and manufacturing planning, we can see how these strategies have turned China into a manufacturing powerhouse of both low and high-end products. As a result, China has profoundly shaped the economic order within the world through its rapid ascension. However, this rise has created a deeply unbalanced ledger, leading to significant global trade distortions that have evolved in complexity and consequence over time. The impact of the “China Shock” greatly disrupted many Western industrial bases, offshoring local manufacturing jobs, leading to factory closures, job losses, and long-term economic decline in several regions. Research by economists David Autor, David Dorn, and Gordon Hanson demonstrates that the original China Shock eliminated approximately 2.4 million American manufacturing jobs between 1999 and 2011, with affected communities experiencing lasting social and political consequences, including increased political polarization, higher crime rates, and reduced social mobility. Today, the world is grappling with a potential “China Shock 2.0“, a new and more strategically potent wave of disruption targeting the high-tech core of many advanced economies. Using a government-led plan, China can take advantage of its large trade profits and control over key materials. This transforms its trade advantage into a tool of geopolitical influence, creating challenges for global policymakers and nations.

Looking Back on ‘China Shock 1.0.’

As mentioned previously, the initial ‘China Shock’ was like pouring fuel onto a fire. The “Reform and Opening Up” policy laid the groundwork for rapid economic growth; however, it was the entry into the WTO that ignited a vast explosion of labour, low wages, and state-supported industrial policies into the global market. This resulted in many Western corporations moving their work operations from local areas to take advantage of reduced costs and optimised supply chains, leading to a huge influx of low-cost Chinese goods into global markets.

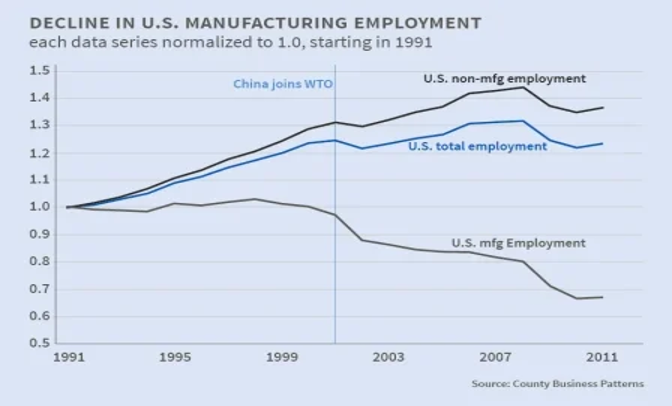

Figure 4. Source: National Bureau of Economic Research. Import Competition and the Great U.S. Employment Sag.

Whilst the shock enabled companies to lower production costs- boosting profit margins and reducing prices for consumers, many Western countries suffered significant industrial manufacturing job losses and wage stagnations. According to the National Bureau of Economic Research, from 1999 to 2011, Americans experienced net job losses of 2 to 2.4 million due to the rise in import competition from China. By 2014, China’s formal manufacturing sector employed approximately 120 million workers, ten times more than the U.S. manufacturing employment at that time.

These vast and irresistible labour advantages alongside state supported tax rebates on exports triggered a manufacturing drain, pulling away local industrial employment across many Western economies. The speed and scale of this transformation caught Western policymakers off guard. Traditional economic models had predicted gradual adjustment periods that would allow workers and communities to adapt. Instead, the China Shock compressed decades of expected industrial change into just one decade, overwhelming the capacity of social safety nets and retraining programs to cushion the impact.

Consequently, many Western industries, such as textiles, furniture, and consumer electronics, experienced a painful decline. This deindustrialisation was not just an economic change towards Chinese manufacturing. It also led to generational unemployment, crumbling local economies, and a growing sense of disenfranchisement among working-class populations in these previous industrial regions in the West. Again, whilst consumers benefited from lower prices and a wider range of goods, these came at an immense social and political cost that fuels much of the rising inequality, social fragmentation, and political polarisation in Western industrial societies today. Ultimately, the rapid shift toward Chinese manufacturing alongside deindustrialisation has resulted in the manufacturing dependency the West faces today. Additionally, the West’s dependence on China’s low-cost goods and tightly integrated supply chains has exposed significant strategic vulnerabilities, as both the EU and the U.S. highlight.

The Geopolitics of Imbalance.

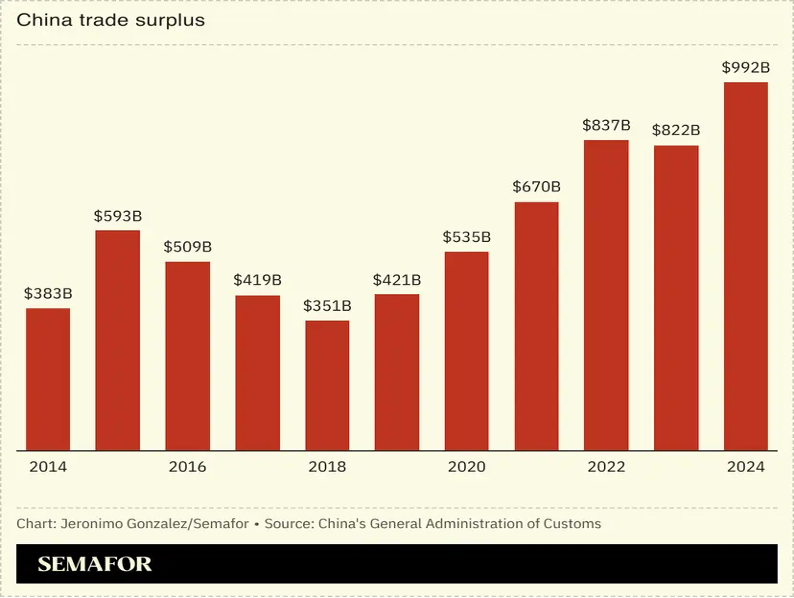

What began as a financial opportunity has eventually evolved into serious geopolitical challenges. China’s growing trade surpluses best illustrate the deepening dependency many nations now face. In 2024, China’s global trade surplus reached a record of nearly $1 trillion. This staggering figure is not the result of organic market forces (such as consumer demand, comparative advantage, etc.) but from deliberate state interventions to secure long-term dominance in global markets, even during trade tensions with Trump’s tariffs. This surplus allows China to accumulate vast foreign currency reserves, giving it significant leverage in international finance and investment, cementing further its global influence.

Figure 5. Source: SEMAFOR. China reports record global trade surplus as threat of Trump tariffs looms.

China has made it clear that it can use its control over important supply chains to serve its political interests, weaponizing trade to reach set political goals. China’s control over critical materials is a prime example. The nation has used its near monopoly on mining 60% and processing 90% of the world’s rare earth elements, which are essential to manufacture modern technologies ranging from smartphones to advanced weaponry. Through imposing export restrictions on rare materials like dysprosium, China can directly disrupt the supply chains of Western nations, targeting their defence, technology, and manufacturing sectors.

This trade power that China wields poses a high concern to many nations, showing the danger of being too dependent on another nation. The risk that a single nation could choke the supply of essential materials for national security and economic strength has been a large topic of discussion. As a response, instead of pursuing full economic decoupling (completely detaching all economic involvement), some Western countries have adopted a “de-risking” approach, reducing strategic vulnerabilities while maintaining selective economic ties.

As mentioned by the EU, a total economic detachment could question the diplomatic relationship many nations have with China, possibly spiralling into more challenges.. It makes sense then to take a targeted approach to de-risking that still allows companies to benefit from China’s world class manufacturing capabilities. This can help Western companies still maintain a steady growth while reducing overreliance on a single market through diversification, thereby limiting vulnerability to potential Chinese political or economic influence. However, implementing effective de-risking proves challenging in practice, as companies often discover that seemingly independent suppliers are ultimately connected to Chinese supply chains, making true diversification more complex and expensive than initially anticipated. The interconnected nature of global manufacturing means that reducing Chinese dependencies often requires rebuilding entire industrial ecosystems rather than simply switching suppliers.

The “China Shock 2.0”.

While the West pursues de-risking strategies with China, the global economy faces a potentially more disruptive second China shock, dubbed ‘China Shock 2.0.’ Unlike the original shock driven by cheap labor that displaced traditional manufacturing in textiles and basic electronics, this new wave threatens the technological foundations of advanced economies, targeting the very industries that Western nations assumed would remain their exclusive domain.

China Shock 2.0 represents a strategic, state-led effort to dominate future industries. The results of Made in China 2025 demonstrate this clearly, as the initiative explicitly aims to achieve leadership in high-tech sectors including EVs, robotics, and biotechnology. While MIC2025’s success in boosting innovation remains debatable, its role in creating massive industrial capacity is undeniable.

Figure 6. Source: The Wall Street Journal. China Shock 2.0 Sparks Global Backlash Against Flood of Cheap Goods

This vision to dominate the industries of the future has led to the rise of many world class corporations from China, such as BYD in electric vehicles, Huawei in telecommunications, and CATL in battery technology. These companies have not only become global brands, but also blend scale, subsidies, and innovation to outcompete global rivals. As a result, China is no longer just the ‘world’s factory,’ it is positioning itself as an architect of tomorrow’s technologies.

However, these massive industrial achievements have not come without cost. They have been fuelled by massive state subsidies- including an estimated $366.75 billion in tax cuts for high-tech and manufacturing sectors- alongside protection for domestic markets. This has led to significant overcapacity in key sectors. With its domestic market unable to absorb the sheer volume of goods being produced, China is now exporting this surplus, from EVs to solar panels, onto the global market at prices that unsubsidised foreign competitors cannot match.

Consequently, this creates a big dilemma for the global economy. While there is a push for green technologies that is fast, cost effective and in supply, the overcapacity of Chinese exports risks undermining and destabilising key domestic industries in other countries. Moreover, governments are stuck between difficult choices: a faster green transition using affordable Chinese technologies or protecting their own industrial base from unfair competition. This tension is at the heart of the “China Shock 2.0”, a disruption not rooted in low-cost labour, but in strategic overproduction and techno-industrial ambition, that could reshape global value chains and upend existing industrial hierarchies.

The West Pulls Back

As China’s presence in the high-tech industry grows, the West’s reactions have become more defensive, expanding trade barriers beyond that of just EVs. These recent tariffs and policy attitudes reflect an overarching wave of detachment from China. However, this detachment isn’t a black and white process. On one hand, governments are pushing policies to achieve a vision of industrial independence. On the other hand, corporations guided by operational costs and market realities are not simply returning home but are instead relocating production to other regional hubs. As a result, this complicated clash between geopolitical strategy and corporate reality has led to the creation of a more fragmented and multipolar global economy, where supply chains are shaped less by national borders and more by regional efficiency and risk.

Figure 7. Source: Author’s own elaborations. U.S. hammer and the EU scalpel.

Differing Western Views: The Hammer vs. The Scalpel.

Whilst both the U.S. and EU seek to achieve the goal of protecting key industrial areas from reducing their Chinese dependency, these Western powers take very different approaches to solving this issue.

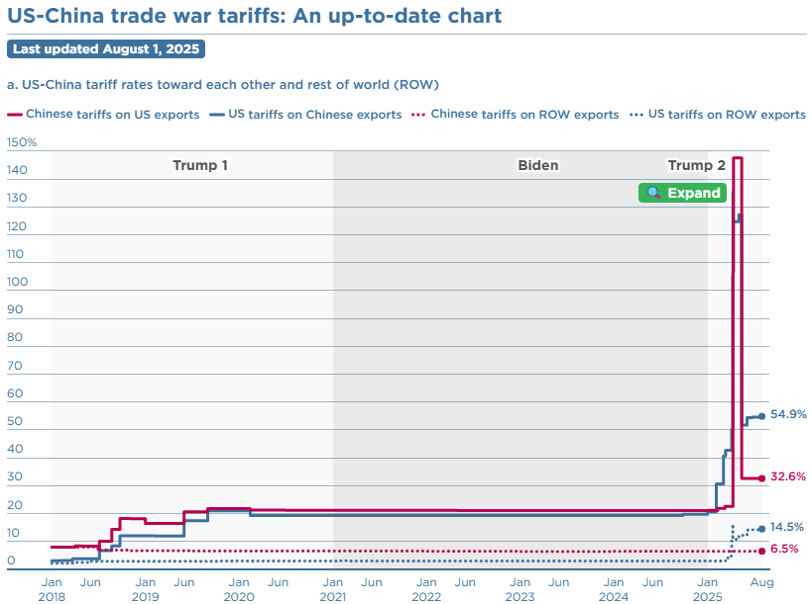

The U.S. has taken a more upfront, confrontational, and security-first approach, viewing China as an adversary whose technological rise must be contained for the U.S. to progress. This perspective treats economic interdependence not just as a source of mutual prosperity but as a critical vulnerability. In this case, American policy acts as a hammer, aggressively targeting overall Chinese industries and technologies to decisively blunt their advancement and protect U.S. strategic interests. We can see this clearly with the introduction of high tariffs initiated under the Trump administration, penalising Chinese imports and incentivising a return to manufacturing on American shores.

Figure 8. Source: Peterson Institute for International Economics. US-China Trade War Tariffs: An Up-to-Date Chart

The CHIPS Act also follows this approach. Designed as a government subsidy to boost U.S. domestic semiconductor manufacturing production, it also acts as a form of investment warfare, drawing critical industries away from China and building advanced chip facilities on American soil. Beyond direct subsidies, the Act includes guardrails that prohibit recipients from expanding semiconductor manufacturing in China for ten years, effectively forcing companies to choose between Chinese market access and American government support. By coupling incentives for domestic investment with restrictions on recipients’ dealings with China, the U.S. aims to decouple the world’s most critical supply chain whilst seeking to re-establish American technological supremacy.

In contrast, the EU has taken a much more surgical approach, pursuing a more nuanced and defensively oriented strategy as originally encapsulated in its official designation of China as a “partner, competitor, and systemic rival” in 2023. This scalpel approach focuses on specific, targeted actions rather than a wide-ranging trade confrontation and aggressive exit. This is partly because of the political complexities within the EU organisation, representing 27 nations with diverse perspectives and varying levels of economic dependence on China.

However, by 2025, this strategy has evolved from a balanced concept into a more assertive, defence oriented plan. The EU’s goal of ‘de-risking’ has been far more proactive, as seen by landmark tariffs on Chinese electric vehicles and ongoing anti-subsidy investigations into other green-tech sectors. Rather than broad tariffs, the EU uses its regulatory power and tools like the Anti-Coercion Instrument to protect its single market and counter economic intimidation. The Anti-Coercion Instrument, enacted in 2023, provides the EU with legal mechanisms to impose countermeasures when non-EU countries attempt to pressure individual member states through economic means, creating a collective defense against economic warfare. Additionally, this approach has managed to avoid engaging in a direct trade war that could severely hurt the region, while still taking meaningful steps to reduce its economic risks and protect critical industries. In doing so, the EU seeks to manage its rivalry with China while preserving avenues for essential cooperation with both Beijing and Washington on global issues.

The Rise of Regionalisation: The Corporate Response

As global politics become more uncertain (especially between big powers like the U.S., China, and the EU), corporations are not sitting idly by. Instead, they are pro-actively finding alternate supply chains to reduce risk, boost resilience, and stay ahead in a more competitive and divided world. While there have been many incentives to bring manufacturing and industry back to the Western shores from China, these policies have not produced the mass industrial reshoring that governments envisioned. Rather, the world is undergoing a regionalisation of trade, with corporations utilising ‘near-shoring’ strategies and consolidating supply chains into three major regional trading blocs. A key example of this approach is the ‘China +1’ strategy, which does not seek to abandon China but diversifies production to other locations to better manage geopolitical risks. The China +1 model acknowledges the practical reality that eliminating Chinese suppliers would be economically destructive for most companies. Instead, firms maintain their Chinese operations while establishing secondary production facilities in countries like Vietnam, India, or Mexico, creating redundancy that allows them to pivot quickly if geopolitical tensions escalate.

Figure 9. Source: Procurious. Build supply chain resilience with a regionalisation strategy.

Centered on the United States-Mexico-Canada Agreement (USMCA), the North American bloc is becoming a powerhouse of nearshoring, with its two main partners, Mexico and Canada, accounting for a combined 28.2% of total U.S. trade. Most notably, Mexico has really captured the hearts of corporations with its lower labour costs, geographical proximity, and favourable trade terms with the U.S. As a result, Mexico has become a nearshoring hub, attracting a record-breaking $21.4 billion in Foreign Direct investments (FDIs) in the first quarter of 2025, a staggering 165% increase in new investments. These investments have been heavily concentrated in the manufacturing sector, which accounts for 43% of the total, firmly establishing Mexico as a winning substitute in the ongoing U.S.-China trade contention.

The second bloc is Europe, centred on its vast single market. The shocks from the COVID-19 pandemic, Russia’s invasion of Ukraine, and rising geopolitical tensions have revealed far greater weaknesses in long-distance supply chains than the EU had anticipated. In response, European corporations are reinforcing regional ties by relocating production to Eastern Europe, Turkey, and parts of North Africa. This corporate-led trend is now being powerfully accelerated by a new wave of EU industrial policy. The Net-Zero Industry Act and the Critical Raw Materials Act are two prime examples of the EU directing billions of euros to build up local manufacturing and create more reliable supply chains for essential goods. At the same time, the Carbon Border Adjustment Mechanism (CBAM) – a carbon emission tariff- has made importing goods into the EU far more costly from countries with weaker climate policies. Like the CHIPS Act, this incentivizes companies to produce goods inside the European single market, keeping jobs, innovation, and economic value closer to home while fortifying the region’s industrial base.

The third, and perhaps most significant, bloc is China-centric Asia. While the West detaches, China is pushing to deepen its economic relationships with its neighbours. Through initiatives like the ASEAN-China Free Trade Area (ACFTA 3.0) and the broader Regional Comprehensive Economic Partnership (RCEP), China’s trade with ASEAN countries surged to a record $991.34 billion in 2024 and $234 billion in the first quarter of 2025, cementing it as an indispensable hub of Asia’s manufacturing supply chain. Even as Western companies pursue a “China+1” strategy, their new factories in Vietnam or Malaysia remain critically dependent on Chinese components, sourcing an estimated 40% of manufacturing inputs from the mainland. Additionally, while projections expect China’s trade with the West will shrink due to trade tension and barriers, its trade with the Global South is set to reach a staggering $1.25 trillion by 2033. Despite western de-risking, the economic expansion within the China-centric Asia bloc remains undeterred, creating a dominant economic bloc independent of Western markets. No sector exemplifies this strategic ambition and its global ramifications more than the EV market.

EV’s: China’s Power Play

EVs have really taken the spotlight when it comes to the contentions between state-led industrial policy, global trade, and the urgent push for a green transition. The electric vehicle sector represents the perfect convergence of three critical 21st-century challenges: technological transformation, climate imperatives, and geopolitical competition. Unlike traditional automotive manufacturing, which developed over decades, the EV revolution has compressed multiple generations of innovation into a single decade, creating unprecedented opportunities for market disruption. By analysing the rapid rise of China’s EV industry, specifically BYD, we can see how one nation’s strategic ambition can reshape global markets. Additionally, we can also view the impact of these actions, creating global backlash and profound challenges for its economic rivals, even as many remain dependent on China’s supply chains and manufacturing strength.

Figure 10. Source: AI Adopters Club. How BYD and Tesla Are Taking Different Paths to Autonomous Driving

The State-fuelled dominance.

As previously mentioned, China has managed to achieve an unparalleled position in the global electric vehicle ecosystem, dominating the global market compared to other nations. By implementing massive state support through subsidies for manufacturers/ consumers, tax incentives, and investment in research and development, China’s market bloomed before many other countries could establish a competitive foothold. As a result, vital supply chains such as the production of lithium-ion batteries quickly became under Chinese control, with approximately 75% control of global battery cell production, firmly establishing themselves as the world’s top EV exporter.

The Global Market impact.

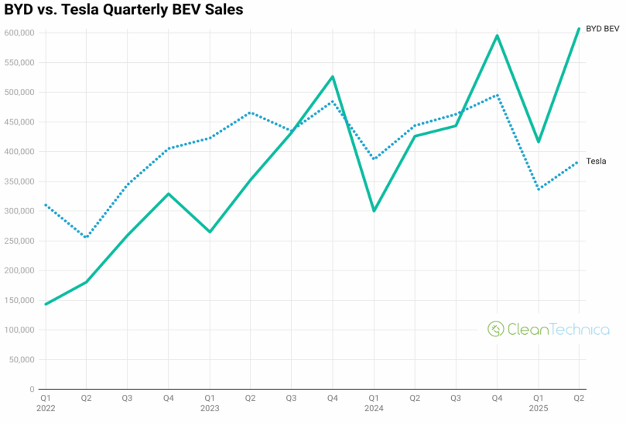

By establishing an early control of the EV market supply chain and government led subsidies, a surgeof low-cost, technologically sophisticated Chinese EVs has begun to flood international markets. BYD (Build Your Dreams) is a clear example of this trend, with the company’s rapid entry and success with the sedan in Western markets. Additionally, in the first half of 2025 alone, BYD sold over 2 million plug-in vehicles, vastly outpacing Tesla’s 700,000 units during the same period.

Figure 11. Source: CleanTechnica. BYD Sales Growth Leaves Tesla In The Dust — Charts & Graphs.

This intense expansion highlights the competitive threat faced by Western manufacturers, who are often burdened with higher labour costs and less integrated supply chains, making it difficult to compete on price. With Western brands such as Tesla, Volkswagen, and Ford being squeezed by emerging markets, the U.S. and EU have both implemented protective tariffs as mentioned before, targeting specific brands such as BYD. These trade barriers are explicitly designed to shield their domestic auto industries from what they see as unfair competition, preventing the erosion of their key manufacturing bases that contribute to Western GDP.

The Reverse Dependency Dilemma.

This situation creates a sharp and difficult paradox for Western nations. On one hand, countries in the West have committed to ambitious climate goals, such as the Paris Agreement, requiring a rapid and widespread adoption of electric vehicles. Additionally, to meet these goals, affordability and readily available models are crucial for this transition. Therefore, it makes sense that companies like BYD are perfectly positioned to meet this demand, offering popular and cost-effective EVs like the Dolphin and Seal that could significantly accelerate the move away from fossil fuels for the average consumer.

However, on the other hand, a heavy reliance on BYD and the broader Chinese supply chain creates a major strategic vulnerability. A tidal wave of Chinese vehicles would decimate legacy car manufacturers in Europe and the United States, threatening millions of manufacturing jobs and dealing a direct blow to the GDP contributions of their automotive sectors. This forces a painful choice: embrace the affordable green technology offered by BYD to meet climate targets or protect domestic industries and economic security by restricting it. The tariffs targeting BYD are the direct result of this dilemma, a measure to protect Western automakers that simultaneously makes the green transition more expensive and potentially slower for their own citizens. This Western reaction, however, only addresses the symptom. The root cause of this relentless export drive lies in the profound domestic crises now gripping China.

Crisis at Home, Deflation Abroad

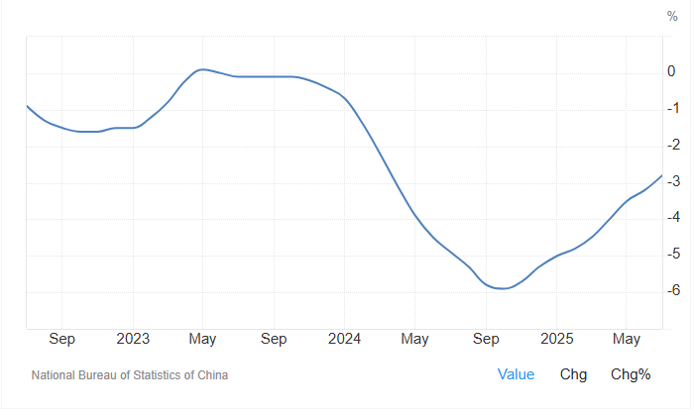

Fuelled by massive subsidies but facing internal decay, China is facing some serious domestic issues that could hijack these plans: a collapsing property market and weak consumer demand. Housing prices have fallen for over 20 straight months, with a 3.5% year-on-year drop in May 2025. This sustained downturn is eroding household wealth and straining local government revenues. This economic strain can also be seen as China’s household consumption in 2024 accounted for only 39.9% of GDP vs. the U.S. at 67.93%.

Figure 12. Source: Trading economics. China Newly Built House Prices YoY Change.

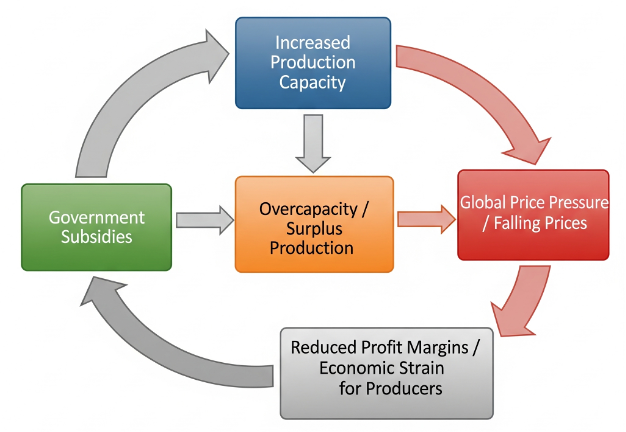

This gap between state-supported production and fragile domestic demand creates a deflationary cycle:

- Government Subsidies Fuel Overproduction: Government Subsidies encourage massive industrial overcapacity in sectors like EVs, batteries, etc.

- Domestic Demand Falls Short: Because the domestic market is too weak to absorb/purchase all these goods, the overcapacity is offloaded onto global markets at discounted rates.

- Global Markets Flooded: This flood of low-cost, state-supported products causes prices globally to deflate (including Western products). This puts pressure on goods globally and threatens the industrial base of other nations.

- Protectionist Backlash: This creates foreign backlash, creating tariffs, trade barriers, or industrial policies, leading to trade tensions that disrupt global supply chains.

- Trade barriers trigger the cycle again: These trade barriers limit export opportunities, prompting governments to increase domestic subsidies to keep industries afloat- restarting the cycle.

The deflationary cycle

Figure 13. Source: Author’s own elaborations. The Deflationary Cycle.

As a result, this has created even more pressure on China to succeed in an export-or-fail gamble, where this industrial overcapacity must be offloaded onto global markets. The stakes for China are existential rather than merely commercial. With domestic consumption growth stagnant and property investment collapsing, exports represent the only remaining viable engine for sustaining economic growth and employment. U.S. Treasury Secretary Janet Yellen highlighted this very issue during a visit to China in April 2024, warning that Chinese overproduction of green technology was distorting global markets.

This immense pressure is forcing China to unleash a new wave of exports on a massive scale, centred on high-tech, low-cost goods like EVs, solar panels, etc. Unlike the first shock, which hollowed out low-skill manufacturing jobs. This new wave directly targets the strategic industrial core of Western economies, the very industries the U.S. and the EU have identified as critical for their future economic growth, climate goals, and technological sovereignty. As we have seen, the flood of subsidised low-cost Chinese EVs poses a serious threat to the legacy automotive industries in North America and Europe.

As a response, the West has been defensive. In May 2024, the U.S. announced it would quadruple tariffs on Chinese EVs to over 100%. Shortly after, in June 2024, the EU followed suit, unveiling its own provisional tariffs on Chinese EVs following an anti-subsidy investigation. However, implementing more trade barriers risks restarting the deflationary cycle. This could force China to push its high-tech goods onto global markets at even lower prices, directly undermining the West’s efforts to protect its domestic industries from a price collapse. Ultimately, this latest shock is pushing trade tensions from long-standing friction into a direct confrontation over the control of key industries.

The Policy Trap

China’s export-driven economy and global “de-risking” have trapped Western policymakers in a complex policy trilemma, forcing them to navigate between three conflicting objectives: protecting domestic industries, managing inflation, and maintaining international alliances, with each choice coming with a significant and often undesirable trade-off.

Protecting domestic industries. Dealing with a flood of low-cost, state-subsidised Chinese imports requires protectionist measures, meaning establishing various tariffs and trade barriers. Whilst this can protect the domestic industry essential to GDP growth and national resilience, they are inherently inflationary, potentially undermining the broader goal of price stability. In effect, governments are forced to choose between long-term industrial resilience and short-term macroeconomic health.

Managing inflation. Alternatively, policymakers can prioritise the fight against inflation by allowing the flow of low-cost Chinese goods, which provides immediate relief to consumers. This approach, however, comes at the direct cost of exposing domestic manufacturers to subsidised competition, risking the erosion of strategic industrial capacity and a repeat of the “China Shock” that previously impacted Western labour markets.

Maintaining alliances. Both an economic and geopolitical problem, maintaining alliances through trade tariffs and growing tension is problematic. The United States and the European Union have adopted different strategic approaches to China. The U.S. has pursued a more confrontational, security-first policy with high tariffs, while the EU attempts to balance its view of China as a “partner, competitor, and systemic rival”. This divergence complicates the formation of a united front, as aggressive tariffs or trade actions by one bloc can create friction and undermine the alliances needed to address shared security and economic challenges effectively.

Let’s Simplify This…

China’s export machine is now a geopolitical weapon. It delivers green goods cheaply but destabilizes Western (and emerging countries) industry and inflames global trade tensions.

How is it being dealt with?

- The U.S. wields a hammer.

- The EU uses a scalpel.

- Corporations hedge with China+1.

Back to Dan Wang and he warns, “The West still hasn’t reckoned with how quickly China’s engineers can move up the value chain.” As a reminder, the US employs about 13 million in manufacturing. China employs 100 million.

The next five years will decide whether China Shock 2.0 locks in Beijing’s technological leadership—or whether Western economies adapt and resist. The consequences will shape not just trade but the global balance of power for the next fifty years.

[GS1]This fails to acknowledge that the MIC2025 initiative is now approaching its 2025 deadline.