From AI to real estate, the winners and losers are already emerging

The U.S. economy is living inside a paradox. Tax policy remains unusually supportive of capital formation, and foreign direct investment continues to flow into semiconductors, energy, manufacturing, and AI infrastructure. Yet the federal government is also running deficits large enough to influence the price of capital across the economy. That tension was already building before the Iranian war. The war has now made it harder to dismiss. President Trump’s budget request of $1.5 trillion for defense spending without significant spending cuts, if passed, will make it significantly worse.

This is not primarily a recession story. It is a cost-of-capital story. Why? Note what happened when the war broke out: US Treasury 10-year yield rose 50 basis points. The central question is whether the current investment wave can outpace a fiscal backdrop defined by structurally high deficits, elevated long-term rates, rising interest expense, and an increasing risk that fiscal constraints emerge in the post-2030 period rather than a distant, abstract future.

Why this matters now

- The Congressional Budget Office projects a $1.9 trillion federal deficit in fiscal 2026, with debt held by the public rising from 101% of GDP this year to 120% by 2036.

- CBO also projects real GDP growth of 2.2% in 2026, slowing to 1.8% in 2027. That is growth, but not growth strong enough to make the debt trajectory harmless on its own.

- The Federal Reserve influences short-term rates , but long-term rates are increasingly being shaped by inflation expectations, Treasury supply, and fiscal credibility.

- The Iranian war has added a stagflation channel: higher oil prices, increased shipping risk through the Strait of Hormuz, a more complicated policy path for the Fed, and the possibility of a Pentagon supplemental reportedly near $200 billion that has yet to be approved.

- The long-term risk is not simply more debt. It is the interaction of more debt with slower trend growth, higher refinancing costs, and a bond market that may eventually demand a larger fiscal risk premium.

- A second long-term fiscal squeeze is demographic: CBO projects the Social Security Old-Age and Survivors Insurance trust fund will be exhausted in 2032, while the broader population-growth trend slows toward zero by 2056. If net immigration remains near zero or negative for a prolonged period, the labor-force slowdown arrives faster than many business plans assume. Potentially leading to a spike in yields as investors doubt the ability of the US government to pay for the debt.

The capital supply paradox

The United States is simultaneously the world’s primary destination for investment capital and its largest sovereign borrower. These two identities can coexist for a while, but not without cost.

When Washington must finance persistent trillion-dollar deficits, it competes with corporate borrowers, households, private equity, commercial real estate, infrastructure developers, and state and local issuers for the same pool of savings. That does not automatically produce a crisis, but it does raise the cost of capital relative to prevailing market conditions.

That is why Fed easing has not translated cleanly into lower long-term borrowing costs. The market is not only pricing inflation and growth. It is also pricing duration risk, issuance risk, and policy credibility.

I. Policy tailwinds are real, but they are being financed against a weaker fiscal base

The bullish side of the story remains credible. Full bonus depreciation improves after-tax returns on machinery, equipment, and technology spending. Industrial policy continues to favor domestic production in sectors such as semiconductors, advanced manufacturing, energy systems, and AI-linked infrastructure. The direct investment position in the United States reached $5.71 trillion at the end of 2024, up $332 billion in one year, a reminder that the U.S. remains the preferred destination for large-scale capital even in a more fragmented world.

However, pro-investment policies do not change the underlying fiscal arithmetic. The CBO’s February 2026 outlook estimates a federal deficit of $1.9 trillion this year, rising to $3.1 trillion by 2036. Net interest is expected to become an even larger driver of the budget over time, rising toward roughly $2.1 trillion annually by 2036. In other words, Washington is trying to subsidize investment while simultaneously absorbing ever more of the nation’s future savings.

The result is a policy mix that can feel pro-growth in the short run and destabilizing in the long run. That is exactly why the policy should not be framed as either boom or bust. It is simultaneously a tailwind and a drag.

II. The Fed has a ceiling problem

The Federal Reserve held its policy rate steady at 3.50%-3.75% on March 18, 2026, while describing growth as solid and inflation as somewhat elevated. Markets’ expectations have adjusted accordingly, with oil prices and geopolitical risks making the path to policy easing less certain.

The CBO projects the 10-year Treasury yield at about 4.1% in 2026 and 4.4% by 2031. These long-term rates matter more to boardrooms than the federal funds rate. Companies refinance using long-term borrowing costs, as do homebuyers. Major investments such as commercial projects, data centers, and large industrial expansions are also evaluated against longer-term yields.

The important shift is conceptual. The Fed is no longer the only institution that determines broad financing conditions. The bond market is imposing its own discipline by keeping term premiums elevated. That is what a fiscal warning looks like before it becomes a full fiscal event.

III. The Iranian war makes the fiscal story worse in three ways

First, it raises the probability of higher-for-longer interest rates.

The Energy Information Administration now expects Brent crude to remain above $95 per barrel over the next two months before dropping later in 2026. The International Energy Agency has described the current disruption tied to the Strait of Hormuz as the largest supply disruption in the history of the global oil market. (I’d argue 1973 oil embargo and the 1979 Iranian Revolution were larger.) Even if prices retreat later, the near-term effect is clear: the war has reintroduced a serious oil shock into the inflation outlook.

A renewed energy shock makes the Fed more cautious, and caution at today’s debt levels is costly. Every month that long-term rates stay elevated raises refinancing costs for the private sector and lifts the government’s own future interest bill.

Second, it raises the likelihood of slower real growth due to higher input costs like steel, aluminum, and helium.

Higher energy and shipping costs operate like a tax on households and businesses, compressing margins, raising freight costs, and diverting consumer spending toward gasoline, utilities, and insurance. Exposure in Europe and Asia to the Gulf disruption amplifies these effects, through weaker external demand, which can feed back into U.S. export performance and multinational earnings.

This is why the Iranian war matters even if the U.S. avoids a domestic supply shock. It can still lower real growth through confidence, trade, logistics, and cost channels. Debt sustainability depends not only on the level of borrowing, but on its relationship to growth.

Third, it risks adding directly to federal borrowing.

Reuters and the Associated Press reported in March 2026 that the Pentagon is seeking roughly $200 billion in supplemental funding for the war, although the request has not yet been finalized or approved by Congress. In a $30-plus-trillion economy, $200 billion by itself does not create a debt crisis. However, that is the wrong way to think about it.

The impact is cumulative. Additional war spending compounds an already large structural deficit, rising net interest costs, and a market environment increasingly sensitive to Treasury issuance. The risk is not a single fiscal shock, but the incremental pressure it adds to an already constrained fiscal trajectory.

If passed, the Trump administration’s Fiscal Year (FY) 2027 budget request would dramatically deteriorate the US fiscal position. It is projected to result in a $2.17 trillion deficit in 2027, $300 billion above 2025 levels. The Committee for a Responsible Budget projects that the total national debt could rise from $36 trillion today to over $56 trillion by 2036. Here’s the kicker: interest costs to service the debt are expected to reach $1.35 trillion in 2027 alone.

IV. Why the real reckoning is more likely after 2030

The central risk is increasingly concentrated in the post-2030 period. The near-term economy can still look healthy while the long-term setup deteriorates. That is not a contradiction. It is how debt problems usually develop in advanced economies with strong institutions. The next five years are about absorption; the following decade is about constraint.

Between now and 2030, the U.S. can still benefit from safe-haven capital, favorable industrial policy, and the lagged payoff from today’s capital spending. After 2030, the composition of the problem becomes more dangerous. Debt service takes up more of the budget. Demographic pressure on Social Security and Medicare intensifies. If growth moderates toward the 1.8% area while average financing costs remain elevated, the gap between nominal borrowing needs and politically feasible fiscal reform becomes more pronounced.

That is the period in which markets begin to ask more pointed questions. Does Washington have a credible deficit path? Will Treasury have to pay structurally higher yields to clear the market? Does the Fed face political pressure if financial conditions tighten too much? Does the dollar’s reserve role continue to offset those pressures, or only cushion them?

V. Social Security and demographic stagnation can turn a debt problem into a debt crisis

There is another structural force that strengthens the post-2030 debt-risk argument: the country is aging into higher entitlement costs at the same time population growth is slowing sharply.

CBO’s February 2026 Social Security baseline projects that the Old-Age and Survivors Insurance trust fund will be exhausted by 2032. At that point, under current law, benefits would be limited to incoming revenues unless Congress acts. That does not mean Social Security disappears, but it does mean one of the largest federal commitments moves from a long-term warning to an active financing problem within the planning horizon of every board and investor. The fund running out can lead to dramatic cuts to retirees between 17%-25%.

At the same time, CBO’s 2026 demographic outlook projects that annual U.S. population growth gradually slows to zero by 2056, with the population aging throughout the period. That official CBO timeline is later than 2032. But the key issue for businesses is not only the endpoint, but the trajectory. Slower labor-force growth means slower potential GDP growth, a smaller tax base relative to age-related spending, and more pressure on productivity gains to do work that population growth used to do automatically.

Simply put:

If productivity>cost of capital, then system stabilizes.

If productivity<cost of capital, then debt spiral risk increases.

This dynamic drives businesses to be more productive, to utilize AI and technology aggressively and to reduce costs in a similar fashion. I.E., reduce headcounts as much as possible.

This is where immigration policy matters. Recent private estimates, including Brookings, suggest net migration in 2025 may already have been near zero or slightly negative, and could remain negative in 2026 if current policies persist. USCIS has also changed H-1B allocation rules for the FY2027 season, favoring higher-wage petitions rather than broad labor-force access. The point is not that CBO has officially moved its zero-population-growth date to the early 2030s; it has not. Yet. The point is that a prolonged immigration clampdown can pull forward the economic effects of demographic stagnation even if the headline CBO endpoint remains 2056.

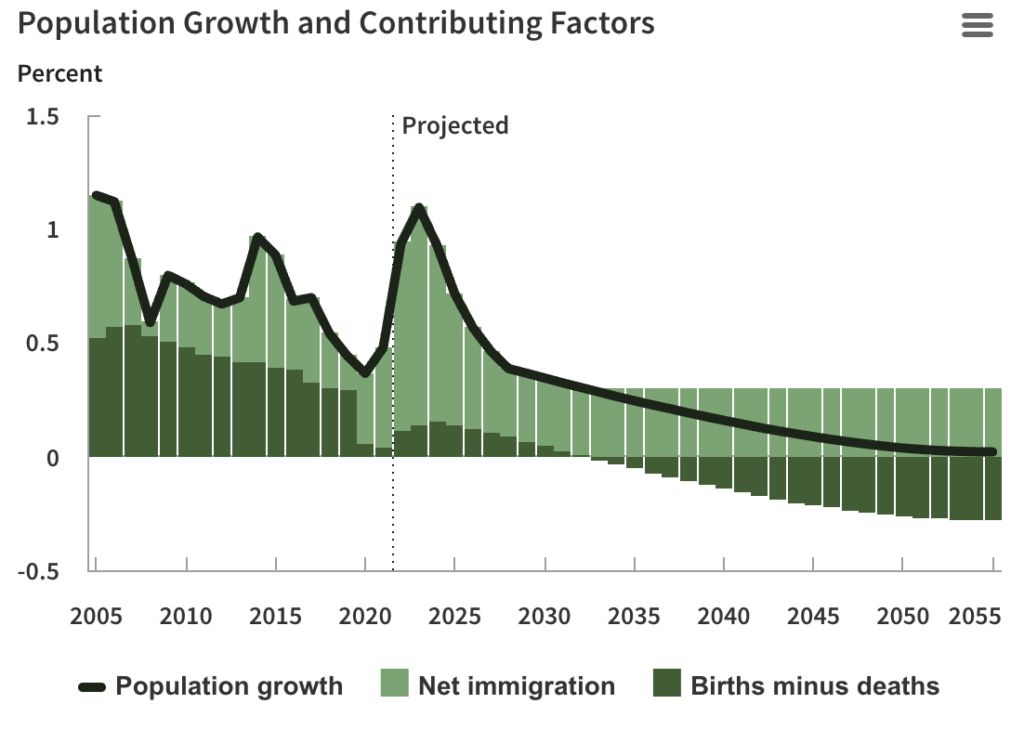

The graph from the CBO below illustrates the issue.

The birth minus deaths rate goes to zero in 2032. Population growth remains positive but only if immigration remains positive. Otherwise, the demographic situation significantly accelerates the negative fiscal situation.

Put differently, the U.S. debt problem becomes much more dangerous when three things happen together: entitlement costs rise, labor-force growth weakens, and interest expense compounds. Social Security stress and demographic stagnation do not create a crisis by themselves. Combined with high deficits and war-related borrowing, they create the conditions in which investors begin demanding a much higher premium to finance the federal government.

None of this implies an imminent U.S. funding crisis. The United States still enjoys institutional depth, reserve-currency status, and unmatched market liquidity. These factors extend adjustment timelines but do not remove fiscal constraints. The post-2030 reckoning is most plausibly a long squeeze, not a sudden collapse: persistently higher long-term rates, more crowding out, weaker rate-sensitive sectors, and a progressively smaller margin for policy error.

VI. What the post-2030 squeeze would look like in the real economy

Housing remains one of the clearest transmission channels. Mortgage rates are tied far more closely to long-term Treasury yields than to short-term policy rates. If long yields remain structurally high, affordability stays broken, labor mobility stays constrained, and housing continues to act as a drag on both growth and social stability.

Capital-intensive sectors can bifurcate substantially. Companies with strong balance sheets, internal cash flow, and policy support can continue investing, while smaller and rate-sensitive firms are pushed into delay, downsizing, or higher-risk financing structures. In other words, the debt reckoning would not hit every industry at once. It would widen the gap between those who can self-finance and those who must borrow at market rates.

The federal budget would also become less flexible. A larger share of federal spending would be absorbed by interest and entitlement obligations, leaving less room for infrastructure, defense, tax policy, or counter-cyclical intervention. This reduces the government’s ability to respond to future economic slowdowns.

That is also when geopolitics becomes even more important. Wars, cyberattacks, shipping disruptions, and industrial policy competition no longer sit outside the debt story. They become part of the fiscal transmission mechanism.

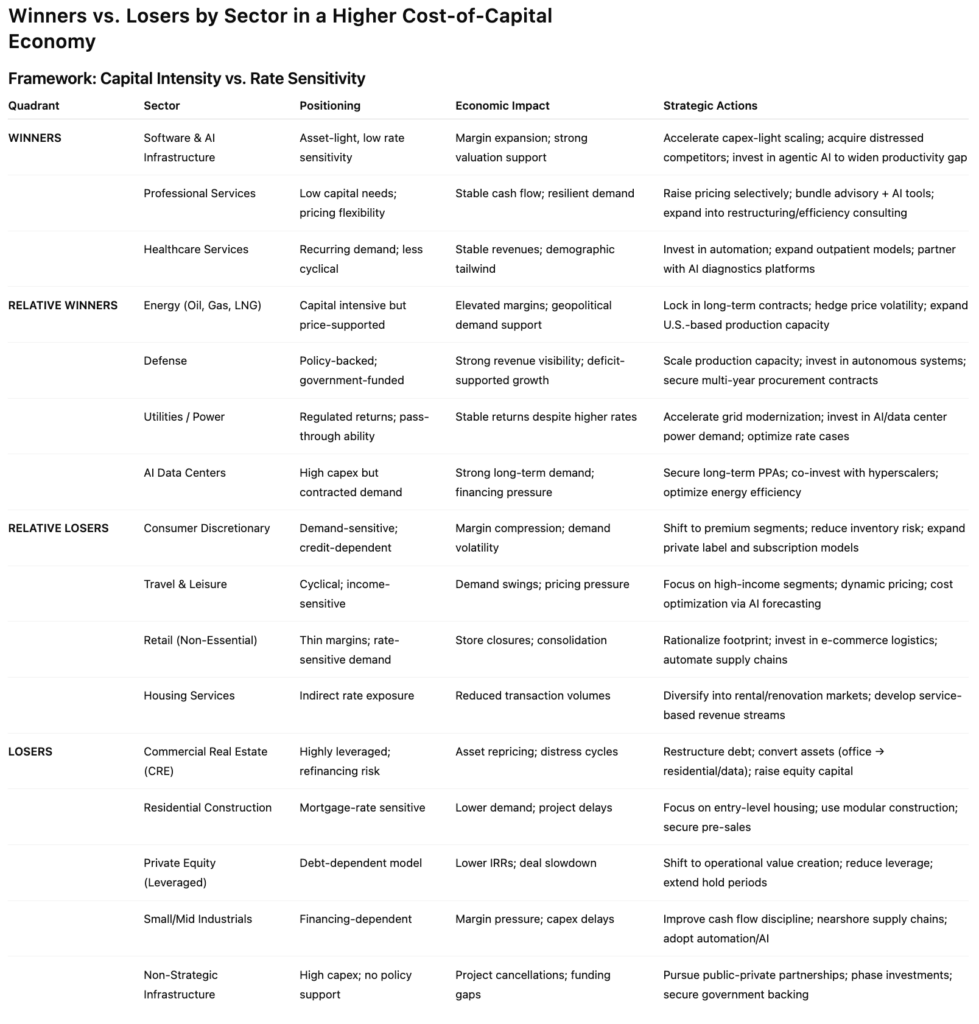

VII. Sector implications

Energy: Inthe near term, the war supports investment through higher prices and supply-security concerns. Over the longer term, elevated energy costs act as a tax on the rest of the economy, raises inflation, keeps interest rates higher than they should and reduces growth.

Defense: The sector benefits from replenishment cycles and potential supplemental spending. But for the macroeconomy, increased defense adds to borrowing pressures rather than providing net economic relief.

Technology and AI infrastructure: These remain among the best-positioned investment themes because they sit at the intersection of productivity, national strategy, and foreign capital inflows. Even so, the rising cost of power, transmission, and long-term financing remain important constraints.

Industrials and manufacturing: Policy support and reshoring continue to help, but margins remain exposed to financing costs, imported inputs, labor shortages, and energy volatility.

Consumer and housing-linked sectors: These sectors remain the most exposed to a post-2030 adjustment because they are highly sensitive to rates, affordability, and real disposable income.

At the end of this research, there is a fully expanded version of these implications and strategies.

VIII. Four questions executives should be asking now

The macro environment is shifting from a cyclical framework to a more structural one, where capital costs, fiscal constraints, and geopolitical risks interact more persistently. In that context, the key challenge is not forecasting a single outcome, but stress-testing assumptions that may no longer hold. The following questions are intended to frame that shift and highlight where current strategies may be most exposed.

• What if the current investment boom is real, but the discount rate applied to that boom stays permanently higher than the last cycle?

• How much of your planning assumes the Fed can eventually deliver lower long-term borrowing costs, even though the bond market may refuse to cooperate?

• If a $200 billion war supplemental or if the Trump administration’s 2027 budget is approved, what matters more for your business: the direct fiscal amount, or the signal that Washington is still adding obligations without a credible medium-term consolidation path?

• What does your strategy look like if the debt reckoning is not a 2008-style crash, but a 2030s environment of slower growth, repeated inflation scares, and chronically expensive capital?

Big question is not whether the economy grows, but the cost

The U.S. economy can keep expanding in 2026 and 2027 and still be moving toward a harder reckoning after 2030. Both can be true. In fact, this is the key point to consider.

The investment story is real. The fiscal story is also real. The Iranian war does not create the debt problem, but it can intensify it through higher rates, slower growth, and new borrowing. At the same time, the projected Social Security financing cliff in 2032 and slower population growth (via immigration policy) deepen that vulnerability by raising age-related spending just as labor-force expansion and tax-base growth weaken.

For businesses, this means the strategic issue is no longer simply recession versus expansion. The more important question is whether your organization is built for a world in which capital remains more expensive, fiscal policy becomes less flexible, and geopolitical shocks hit an already leveraged public balance sheet.

Over the next five years, the advantage will shift toward organizations that treat federal debt dynamics as an operational variable rather than an abstract policy issue. Financing conditions, workforce planning, housing exposure, investment timing, and competitive positioning will increasingly reflect this constraint.

The adjustment is unlikely to take the form of a single, discrete event. The more probable outcome is a gradual repricing of capital: persistently higher long-term rates, increased crowding out, and a reduced margin for policy error as the post-2030 period approaches.