A Myriad of Changes in a Disrupted World

The plastics industry is one that is highly dependent on energy and water for its operation. Both climate change, and the related weather and drought impacts, as well as the energy crisis from the Russian war, can affect the plastics sector in multiple ways, which we will closely explore in this article. Moreover, with the recent United Nations (UN) resolution on ending plastic waste and the expected global legal regulations in 2024, the plastics industry is expected to witness a change as it rapidly transitions to a more circular one.

Climate change is perhaps the major long-term threat facing the world, causing severe and widespread disruptions in nature and affecting billions of lives everywhere. In its latest 2021 Assessment Report, the Intergovernmental Panel on Climate Change (IPCC) issued a “Code Red” for humanity as human-driven global heating has increased. As we’ve covered in previous articles, we are already witnessing the impacts of climate change on various countries, including global droughts, the related water and food shortages, and severe weather volatilities. Those changes can have multiple impacts on the plastics industry. As will be explained in this article, unpredictable weather events can affect the industry’s supply chains, leading to severe closures and halting production and deliveries. This is what happened in 2021 in Texas, for instance, when the winter storm forced the shutdown of close to 80% of the U.S. plastic resin production. Moreover, given the industry’s high dependence on water for direct production, cleaning, and cooling, limited water resources can lead to less water allowances for plastic plants, which can significantly slow down their production. For example, in 2014, Dow Chemicals, one the world’s largest plastics manufacturers, struggled to secure the needed water supplies for its production operations, which affected its business.

Climate change is not the only disrupter currently affecting the plastics industry. As the world was recovering from the COVID-19 economic impact, including the shortages in supply chains, the Russia-Ukraine war hit the global economy like never before. Russia and Ukraine are major players in the global energy sector and other industrial commodities, as we’ve covered in a previous article, and the war between both countries has had a catastrophic effect on the global economy. Higher oil and gas prices can largely hike plastic and resin prices, given they represent main inputs in the manufacturing process. As an example of the downstream impact from the war, BASF, one of the world’s largest chemicals companies, is considering how to potentially shut down the world’s largest integrated chemical complex spanning some 200 plants if gas supplies fall further from Russia (WSJ).

This article seeks to give a better insight into the plastic industry and the impact of global developments on it. To achieve this, it gives an overview of the plastic industry and discusses the sustainability of plastics. It goes further to examine the impact of geopolitical events on the plastics industry. Finally, it analyses the future of the plastic industry as it transitions towards reducing virgin material and seeking circularity.

As a reminder, plastics are essential for daily use, both for consumers and industrial processes alike. How the industry navigates the next five to ten years will be critical.

A Brief Overview of the Plastics Industry

Global Production of Plastics

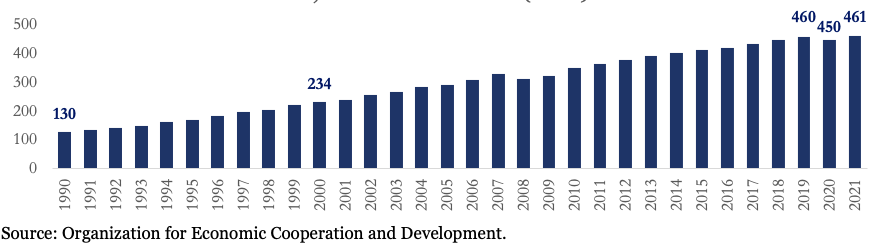

Fueled by rapid population growth and rising income levels, global plastics production has grown substantially over the past 30 years. The graph below shows the development of the global production of plastics between 1990 and 2021, according to the Organization for Economic Cooperation and Development (OECD). In 2019, prior to the COVID-19 pandemic, global plastics production stood at 460 million metric tons (Mmt), which was almost double the 234 Mmt produced in 2000 and four times the 130 Mmt produced in 1990. In the two decades, the growth in plastics outpaced global economic growth by around 40%. The plastic industry has also grown faster than other industrial commodities, such as aluminum, steel, and cement. While the COVID-19 pandemic slightly slowed down plastics growth in 2020, production quickly rebounded to reach its pre-pandemic levels in 2021. The OECD forecasts that, if no regional or global action is taken to reduce plastic use, the industry will reach almost 1231 Mmt by 2060.

Global Plastics Production, million metric tons (Mmt)

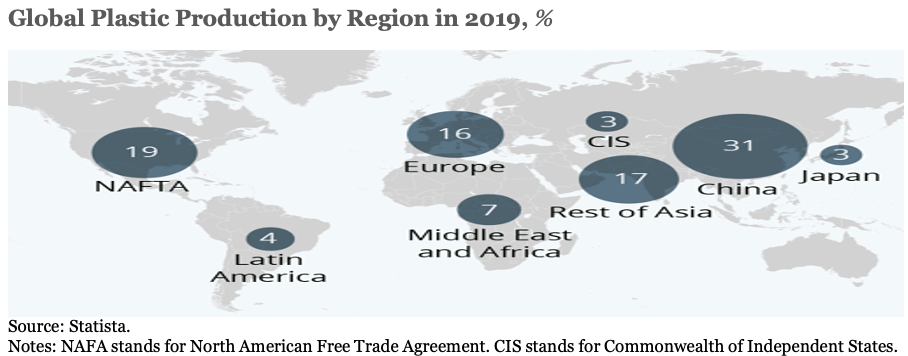

The map below shows the percentage contribution of each region to the global production of plastics for 2019. Asia alone is responsible for almost half of the global plastic produced, with China accounting for 31%and the rest of Asia for 16%. North America accounts for almost 19% of global production, with the United States being the major player. Many of the largest plastic manufacturers in the world are based in the U.S., including ExxonMobil and Dow Chemical. Europe, the Middle East and Africa, and Latin America are each responsible for 16%, 7%, and 4%, respectively. Japan alone produces almost 3% of global plastic.

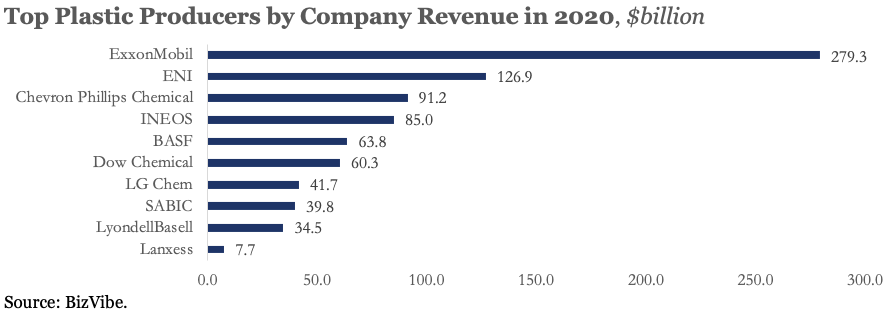

Looking at the top-10 manufacturers of plastics in the world, ExxonMobil, ENI, Chevron Phillips, INEOS, and BASF are the five largest companies by revenue. ExxonMobil’s revenues in 2019 stood at $279.3 billion. Dow Chemicals is also a major producer with revenues of around $60.3. It should be noted, however, that those figures represent the company’s total revenue, which also includes various other non-plastic products, mostly other chemicals.

Global Plastics Consumption

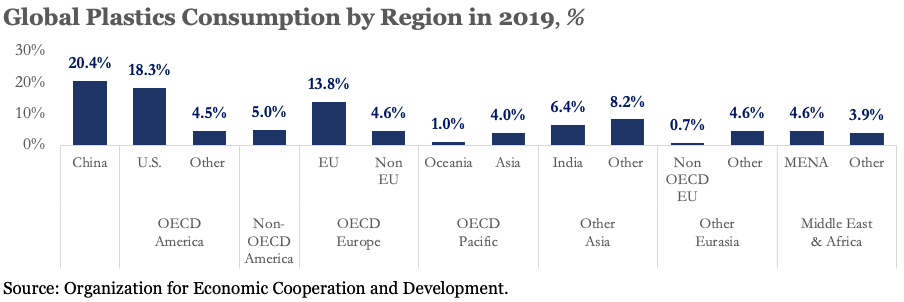

When it comes to global plastics consumption, OECD countries and China alone account for almost two-thirds of the global use of plastics. China and the U.S. are the largest two single-country users, accounting for global shares of 20.4% and 18.3%, respectively. European OECD countries are responsible for almost 18.5% of total plastic use, with the European Union (EU) accounting for 13.8%. Other Asian countries contribute a share of 14.6% and the Middle East and Africa contribute around 8.5%. Other regions each account for around 5% of the global use of plastics.

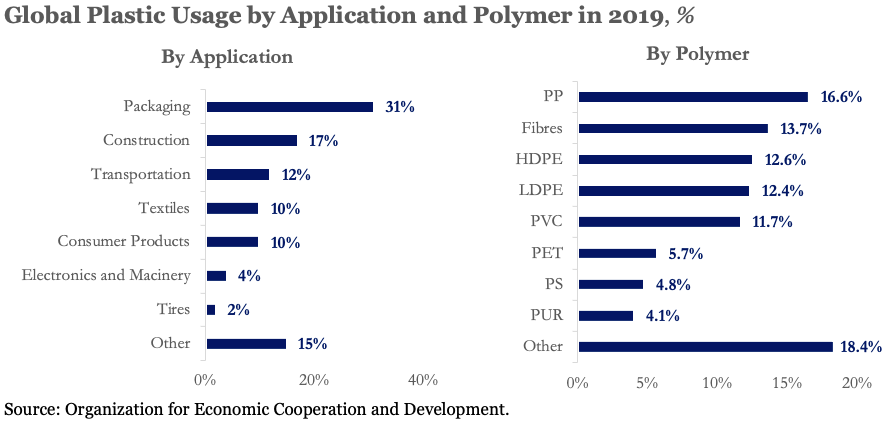

The graph below shows the usage of plastics by application in 2019. Most plastic usage is in Single-Use applications. Packaging is single-handedly the largest segment that consumes plastic, accounting alone for a global share of 31%. Other estimates by IHS Markit even report a packaging share of 38%. In Europe, the share of packaging in plastics use is estimated to be 41%. Construction and Transportation come next, contributing to shares of 17% and 12%, respectively. Collectively, packaging, construction, and transportation consume almost 60% of global plastics. Consumer products and textiles applications are each responsible for around 10% of global plastics usage, while electronics and machinery account for 4% and tires account for 2%.

Looking at the global plastic use by polymer, Polypropylene (PP), Fibers, High-density polyethylene (HDPE), Low-density polyethylene (LDPE), and Polyvinyl Chloride (PVC) come at the top of the list, accounting together for around two-thirds of global plastics usage. Those polymers are used in a variety of applications. While PP, for example, is used for food packaging applications as well as automotive parts, fibers are important for the production of textiles. Applications for HDPE and LDPE include, among others, toys, shampoo bottles, reusable bags, and food packaging.

Plastics and Sustainability

Plastic Waste and Recycling

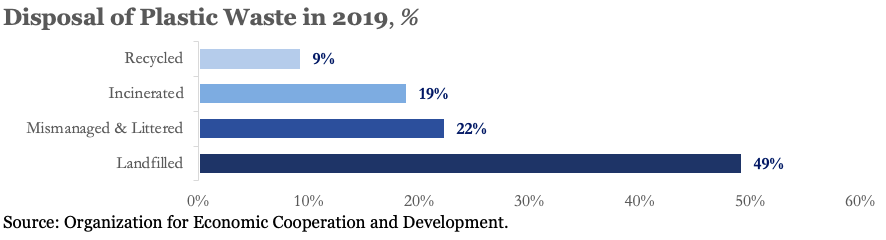

It is estimated that around 40% of wasted plastics are single-use plastics. According to the Minderoo Foundation, in 2019, single-use plastics accounted for around 135 Mmt of plastic waste. Together, food bottles, film packaging, retail bags, food packaging, trash bags, and sheet packaging were the major sources, accounting for around 80% of single-use plastics waste. The consumption of single-use plastic has risen during the COVID-19 pandemic, potentially worsening the state of plastic pollution. With the rapidly increasing production of plastics, plastic waste has more than doubled from 156 Mt in 2000 to reach 353 Mt in 2019. Out of this total waste, as shown in the graph below, 49% of plastic was disposed of in sanitary landfills, 19% was incinerated in industrial facilities, while only 9% was recycled. The remaining waste, almost 79 Mmt or 22%, was mismanaged and littered, which was burnt in open pits, disposed of in uncontrolled dumpsites, or dumped into the ocean.

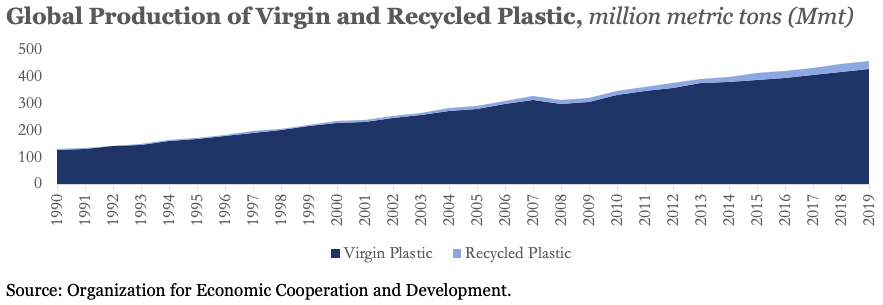

While the production of recycled (secondary) plastics has increased considerably over the years, the majority of plastic used today is still virgin (primary) plastic that is produced from crude oil and gas. Recycled plastic usage has increased almost 15 folds from merely 1.9 Mmt in 1990 to 29.1 Mmt in 2019. Yet, recycled plastic still accounts for no more than 6% of total plastic use. In 2019, virgin plastic production and usage were as high as 430 Mmt.

Top Sources of Plastic Waste by Country and Company

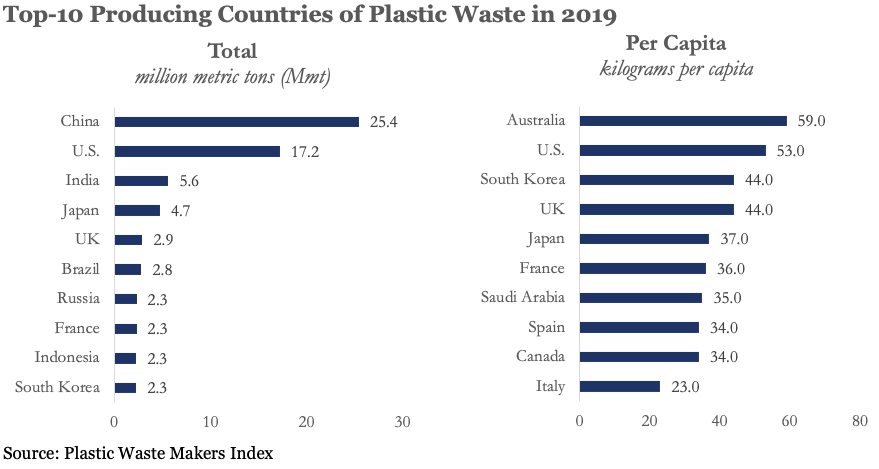

Together, the top-10 generating countries of single-use plastic waste account for a share of 50%. China and the U.S. are the two largest generators of plastic waste in the world. In 2019, each was responsible for 25.4 and 17.2 Mmt of single-use plastic waste, respectively, accounting together for a share of 42.6%. However, when looking at the single-use plastic waste generated per capita, Australia comes at the top with a contribution of 59 kilograms per person, followed by the U.S. at 53 kg. South Korea and the UK come next, each being responsible for 44kg per person as seen in the graphs below.

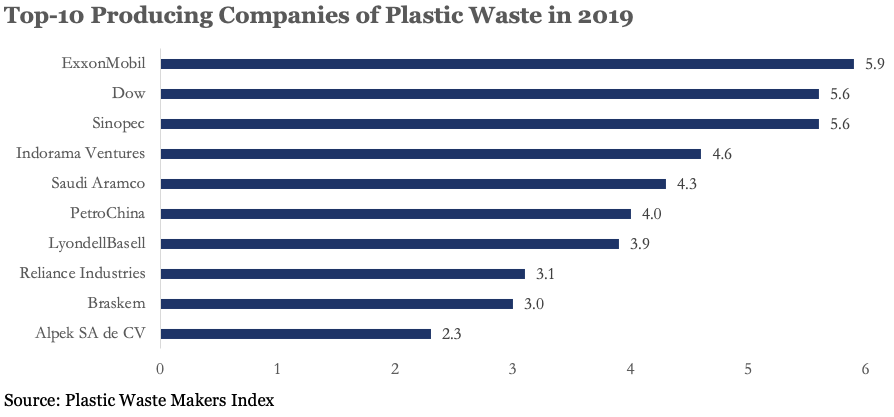

Interestingly, in 2019, 90% of the global single-use plastic waste was generated by only 100 companies, according to the Plastic Waste Makers Index. Together, the top-20 plastic manufacturers were responsible for 55% of the global waste, while the top-5 manufacturers accounted for close to 20%. The graph below ranks the top-10 companies by plastic waste generation. Among the top-5 manufacturers are ExxonMobil with 5.9 Mmt of waste, Dow Chemical and Sinopec with 5.6 Mmt each, Indorama Ventures with 4.6 Mmt, and Saudi Aramco with 4.3 Mmt. Of the total 26 Mmt of plastic waste produced by those five companies, almost half of that, 11 Mmt, was used in China and the U.S. alone.

The Carbon Footprint of Plastic Production

Plastic waste is not the only form of environmental impact from plastic production and use. Similar to steel, cement and ammonia, plastic production emits large amounts of greenhouse gas emissions (GHG) emissions during its lifecycle. Conventional plastic production begins by using an energy-intensive process that transforms fossil fuel feedstock into monomers. However, fossil extraction and use during the production process is not the only source of GHG. During its lifecycle, other activities such as transport, refining, and disposal all have a significant carbon footprint. While production and conversion of plastic into products account for almost 90% of the emissions, end-of-life emissions largely vary depending on the method of disposal. Incineration at disposal generates the highest amount of CO2, although this can be offset if energy is recovered through waste-to-energy processes. While recycling does directly emit some CO2, the use of secondary plastics rather than virgin production can significantly reduce emissions and potentially reduce costs to producers.

According to the OECD calculations, in 2019, fossil-based plastics were estimated to emit around 1.8 billion metric tons of CO2 equivalent. That’s 3.4% of 2019 global emissions. The OECD expects plastic production to triple by 2060. If plastic production and use continue growing as planned, one estimate shows that, by 2030, emissions from plastic production could surpass that of 295 new 500-megawatt coal-fired power plants. By 2050, plastic GHG emissions could reach more than 56 billion metric tons, which is almost 14% of the entire remaining carbon budget, as estimated by scientists from the University of Technology Sydney (UTS). According to the scientists, the predicted global carbon budget to limit global warming to 1.5°C is 400 billion metric tons until 2050.

Global Developments Impact on the Plastics Industry

Climate Change & Weather Volatility

With climate change comes a wide range of challenges from food and water scarcity to extreme heat waves and floods. Weather volatility is one of the major challenges that face plastic manufacturers today. As weather volatility increases, so would the volatility in the supply and demand for plastics and, hence, its prices. The supply chain of plastics is especially vulnerable to extreme weather conditions as it largely depends on huge global shipments of various intermediate materials to sustain its operations. Demand for plastics, such as PET, for example, has also been known to increase with temperature, as on-the-go bottle consumption rises.

The years 2020 and 2021 were especially difficult for the plastics industry as supply chains suffered from volatile weather conditions, exacerbated by the unresolved bottlenecks from the COVID-19 crisis. The production of several polymers, including PE and PP, have been affected. Those are used in the production of many plastics, essential for usage in food packaging, smartphones, car parts, exercise equipment, and other appliances.

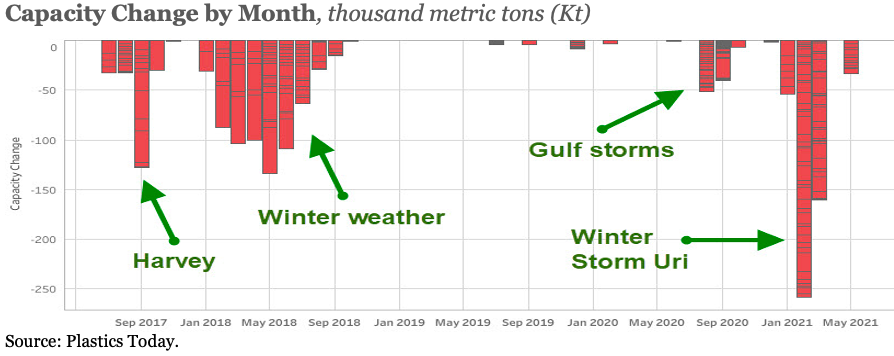

In August of 2020, several petrochemical plants in Texas and Louisiana shut down their operations ahead of Hurricane Laura, halting the production of around 10-15% of U.S. PE and PP production overnight. ExxonMobil, the giant manufacturer, was among those forced to shut down factories. In the U.S., the effects of the 2021 Ida and Nicholas Hurricanes in addition to the winter storms on supply chain disruptions and price volatilities has not been fully resolved to this day. In February 2021, the winter storm and freeze led to massive blackouts in Texas, which led to the shutdown of almost 80% of the U.S. plastic resin production and substantially hiked prices for materials like PP and PE. Texas is home to some of the largest plastic manufacturers in the world, including ExxonMobil and Dow Chemicals. It was estimated that over six months were required to recover from the imbalances brought about by the storm. The graph below depicts how unpredictable power outages from extreme weather conditions have negatively impacted the monthly production capacity of HDPE in the U.S between end-2017 and mid-2021.

The impact of volatile weather conditions on the plastics industry was not restricted to the U.S. In July 2020, for example, heavy rains and floods in the south and east of China led to cooler temperatures, which coupled with logistical curtailments, reduced domestic demand for PET and slowed down market activity. This led to a drop in the prices of Chinese PET exports.

In February 2021, production and logistics were restricted in Europe due to the extreme cold weather, which has been linked to severe storms in earlier years. Some PET manufacturers in Germany, among other countries, were affected as railways stopped due to the weather. Deliveries of materials were halted and, if made, were at much steeper prices.

Moreover, with the rising Taiwan heatwaves in May 2021, many petrochemical producers faced disruptions due to the resulting power outages. Blackouts forced a number of petrochemical plants to shut down, including Formosa Plastics’ 234,000 ton/year PVC plant. Formosa Plastics Group is Taiwan’s largest petrochemical manufacturer. Taita Chemical and Kaofu Chemical, the 100,000 ton/year polystyrene plants, were also affected.

Water Availability

Similar to semiconductor production, plastic production has a significant water footprint, given it consumes a large amount of water during its manufacturing process, whether for direct production, cleaning, or cooling. It is estimated that it takes almost 28 gallons (106 liters) of water to produce one pound of PET plastic, the material used in water and soda bottles. The production of the average single-use water bottle can take between 2 to 6 times the water it actually carries.

The International Energy Agency (IEA) estimates that non-energy industries withdraw almost 10% of the global freshwater resources. Moreover, global water demand for manufacturing is forecasted to increase by 400% in 2050, from 2000 levels. The manufacturing process of plastics, in particular, and other chemicals, in general, is highly dependent on water during the different phases of production. For such industries, water is a crucial resource for production operations as it has no substitute. With the looming global water shortage and drought conditions, plastic producers might find it harder to carry on their production processes.

For example, in the summer of 2011 during one of Texas’ worst droughts ever, the Taiwanese group Formosa Plastics suffered a cut in its water allocation from Lake Texana by almost 20%. This forced the company to pay $1 million to the city of Corpus Christi to obtain additional water for operations. In 2014, Dow Chemicals, the global manufacturing giant, struggled to secure the necessary water supplies for its production operations. Dow Chemicals is considered to be the largest consumer of water from the Brazos River.

Today, new water restrictions are enforced as Texas’ city of Corpus Christi is entering Stage 1 of mild water shortage watch. According to the drought contingency plan, the city enters Stage 1 when the combined water levels at Lake Corpus Christi and Choke Canyon Reservoir are at 40% or lower. Currently, the water level stands at 42.9% and is expected to hit the threshold by the end of this June. Stage 1 only imposes restrictions on irrigation by residents. If water levels were to reach 30% and the city enters Stage 2 of moderate shortage this summer, further industrial restrictions would be enforced. Similarly in California, officials are strongly encouraging residents and businesses to reduce their water use, with expectations of further tighter restrictions if the situation worsens. Restrictions on water usage are also affecting the global plastic industry. For example, petrochemical producers in Taiwan are struggling with a limited supply of industrial water, as the country battles against its worst drought in 56 years.

Ukraine War

Just as the supply chains were starting to recover and prices of plastic resin started to ease following the pandemic, the Russia-Ukraine war hit the plastics industry hard. Following the global sanctions imposed and President Biden’s ban on Russian oil imports, spiraling oil prices hiked the cost of plastic resin, largely impacting the industry.

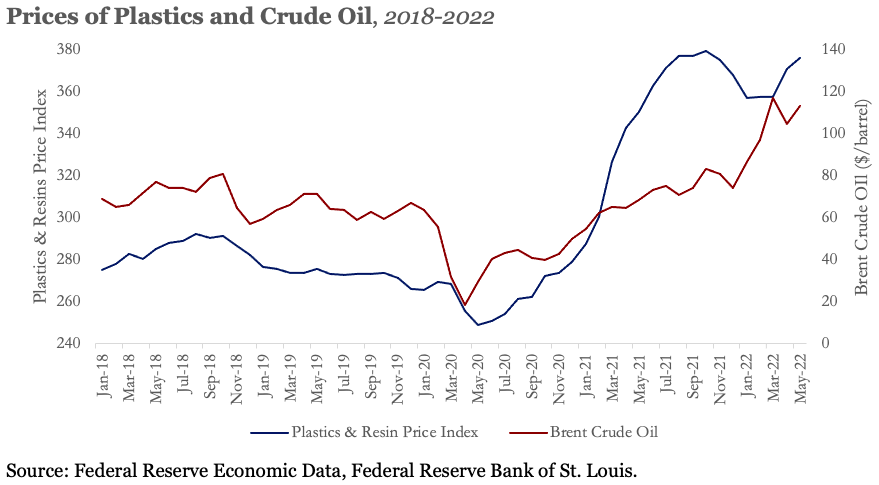

On March 8, crude Brent oil peaked at $133 per barrel, the highest since July 2008. Prices have been hovering around the $120 per barrel range for the whole month of June. Given their high-energy intensity, plastic prices are among the first to get affected. According to the ICIS Petrochemicals Index (IPEX), in March 2022, global petrochemical prices were up by 20.1% year on year (YoY). In Europe, the U.S. Gulf, and Asia, the regional price indices showed annual increases of 50.4%, 36.2%, and 9.6%, respectively. Despite a slight easing in prices, the global index still showed a YoY increase of 8.3% in May 2022.

Plastic and oil prices have always been historically linked, given the industry’s high dependence on energy for production. The graph below shows the evolution of monthly average Brent crude oil prices and the monthly producer price index of plastics material and resins, between January 2018 and May 2022. According to Joseph Chang, Global Editor at ICIS Chemical Business, “If they (oil prices) persist at these levels or rise further, there is the danger of demand destruction. Already, global and U.S. GDP forecasts are being slashed.”

The majority of Russian PP exports go to Europe, where many companies are refusing Russian products. Since 2020, Russia has largely increased its production capacity and exports of plastic resin, especially PE and PP. In 2021, over 50% of its PE exports went to China. While it was expected that Russia would boost its exports of plastics to China following the war, this wasn’t the case as the spread of COVID-19 and lockdowns in China lowered its demand. With all those geopolitical disruptions going on, unstable resin prices are expected to remain an issue for plastic processors in the near future, especially with oil prices remaining above $100 a barrel.

Recent UN, US and CA Regulatory Actions

The 5th UN Environment Assembly (UNEA-5) made history on March 2 in Nairobi, by adopting 14 resolutions to strengthen action to “reduce pollution, protect, and restore nature.”

Most notably is the resolution to “End plastic pollution: Towards an international legally binding Instrument.” The resolution established an Intergovernmental Negotiating Committee, to start its work during the second half of 2022. The committee will work on completing a draft for a legally binding treaty to end plastic waste, a first of its kind, to be finalized by the end of 2024. The historical resolution was supported by heads of state, ministers of environment, and other representatives from 175 nations.

Major takeaways from the resolution include:

- Affirming the importance of global cooperation and governance to “take immediate actions towards the long-term elimination of plastic pollution.”

- Recognizing the “wide range of approaches, sustainable alternatives and technologies to address the full life-cycle of plastics,” from production to disposal.

- Highlighting the need for enriched “international collaboration to facilitate access to technology, capacity building and scientific and technical cooperation.”

- Emphasizing the “importance of promoting sustainable design of products and materials so that they can be reused, remanufactured or recycled and therefore retained in the economy for as long as possible along with the resources they are made of, as well as minimizing the generation of waste, which can significantly contribute to sustainable production and consumption of plastics.”

According to the President of UNEA-5 and Norwegian Minister for Climate and the Environment, “Against the backdrop of geopolitical turmoil, the UN Environment Assembly shows multilateral cooperation at its best… Plastic pollution has grown into an epidemic. With today’s resolution we are officially on track for a cure.” The Deputy Secretary-General of the UN, Amina Mohammed, also added, “Today, no area on the planet is left untouched by plastic pollution, from deep-sea sediment to Mount Everest. The planet deserves a multilateral solution that speaks from source to sea. A legally binding global agreement on plastic pollution will be a truly welcome first step.”

According to the resolution, the 2024 legally binding agreement should promote “national and international cooperative measures to reduce plastic pollution,” and to “develop, implement and update national action plans reflecting country-driven approaches to contribute to the objectives.” One would naturally expect that stricter national regulations should start forming, for countries to start preparing for the legally binding treaty once signed, which would affect the plastics industry and how it operates. The treaty is set to “promote sustainable production and consumption of plastics, including, among others, product design, and environmentally sound waste management, including through resource efficiency and circular economy approaches.” Leading up to and following the treaty, it is expected that the plastic industry, and especially that for single-use plastics, will change.

The United States has a bill pending H.R. 2467-PFAS Action Act of 2021. The bill was passed by the US House in 2021 and now sits in the Senate Committee of Environment and Public works. Here below are the major provisions.

- This bill establishes requirements and incentives to limit the use of perfluoroalkyl and polyfluoroalkyl substances, commonly referred to as PFAS, and remediate PFAS in the environment. PFAS are man-made and may have adverse human health effects. A variety of products contain PFAS, such as nonstick cookware or weatherproof clothing.

- The bill directs the Environmental Protection Agency (EPA) to designate the PFAS perfluorooctanoic acid (PFOA) and perfluorooctanesulfonic acid (PFOS) as a hazardous substances under the Comprehensive Environmental Response, Compensation, and Liability Act of 1980, thereby requiring remediation of releases of those PFAS into the environment. Within five years, the EPA must determine whether the remaining PFAS should be designated as hazardous substances.

- The EPA must also determine whether PFAS should be designated as toxic pollutants under the Clean Water Act. If PFAS are designated as toxic, then the EPA must establish standards to limit discharges of PFAS from industrial sources into waters of the United States. In addition, the EPA must issue a national primary drinking water regulation for PFAS that, at a minimum, includes standards for PFOA and PFOS.

- Among other requirements, the EPA must also issue a final rule adding PFOA and PFOS to the list of hazardous air pollutants, test all PFAS for toxicity to human health, and regulate the disposal of materials containing PFAS.

- Finally, the bill provides incentives to address PFAS, such as grants to help community water systems treat water contaminated by PFAS.

The bill has many issues to resolve. For example, the EPA would be able to designate these plastic products as hazardous waste making every landfill in the country a hazardous waste site. The costs would be prohibitive.

California has SB 54 as an attempt to address plastic waste in the state. According to Calmatters, the structure is as follows.

SB 54, however, would give the plastics industry more time to comply with the mandates and regulations in the ballot measure — until 2032 instead of 2030 — that are designed to ensure all single-use packaging and foodware is recyclable, reusable, refillable or compostable. In California, only a small portion of all plastic waste is recycled. About 85% ends up in landfills.

The bill would still impose a fee on single-use plastic packaging and foodware, with proceeds going to CalRecycle, the state Natural Resources Agency and local governments.

Like H.R. 2467, this CA bill has unintentional consequences which could potentially disrupt plastic production and use in the state.

Overall, the industry should start witnessing more recycled plastics used as opposed to virgin plastics, as well as finding alternative solutions and alternatives to the use of plastics for applications, including packaging and others. The OECD expects that leading up to 2060, recycled plastics will grow faster than their virgin counterparts. If both regional and global action were up to ambition, we can see a reduction in plastic use and waste by 33% in 2060, compared to baseline forecasts of no action.

The Future & Transition of the Plastics Industry

It is true that the traditional plastics industry is forecasted to grow at lightning speed over the next decades, with virgin plastic and plastic waste at the front. However, given all the global disruptions and changes in regulations, could those challenges also present opportunities for the industry to transition into one that is innovative and more sustainable?

Recycling plastic consumes much lower resources and has a smaller environmental footprint compared to the production of virgin plastic. In the transition to a more circular economy, the packaging industry, which accounts for 30-40% of plastic use, is starting to transition to sustainable alternatives or recycled materials. Indeed, such a transition has already started. Prior to the UNEC meeting, in January 2022, more than 70 organizations that included major active companies in the packaging industry, such as Coca-Cola Company, Nestlé, Procter & Gamble, PepsiCo, and Unilever, called for a legally binding UN treaty that would support the transition to a more circular economy.

Many companies in the packaging industry have already started announcing pledges to become circular in the next one to three decades. For example, Coca-Cola Company recently pledged to sell, by 2030, no less than 25% of its beverages globally in refillable or returnable containers. Coca-Cola is also exploring more sustainable plastic packaging alternatives, such as its 100% plant-based prototype bottle. Similarly, in Europe, UNESDA Soft Drinks pledged in 2021 to use 100% recycled and/or renewable PET for its plastic bottles by 2030, where technically and economically feasible.

While plastic is constantly accused of its huge environmental footprint, there is a massive difference between single-use PET bottles, for instance, and PET screens or pipes used in many durable applications. In some situations, the long-lived non-degradable nature of plastic can be useful. If used wisely, plastic could actually increase sustainability.

Plastic pipes, for instance, are one solution that could help save water amid the current global water shortage. For example, in 2020, an oriented PVC (PVC-O) pipeline was constructed and used to feed water up to 12 kilometers in Pernik, a drought-stricken town in Hungary. This saved the town after suffering a near-empty local reservoir due to a severe drought. PVC-O is an innovative form of plastic material, which has high strength and is 12 times less dense than steel allowing for fast installation. Those pipes can be installed in a little over a month and allow for high-speed water flow, characteristics that are both very valuable in the cases of drought. Several similar projects have been introduced in other parts of the world, given how useful the strong, light, and fast-installation pipes can help adapt to extreme weather events.

Another sustainability aspect where plastic is proving to be helpful is hydrogen. The hydrogen industry is a key project for reducing CO2 emissions, as burning hydrogen for energy only produces water as opposed to the carbon-intensive fossil fuels. Some countries today are exploring the potential of pumping hydrogen into the gas network for energy use. The only caveat is that the traditional gas pipes are not suitable for transporting hydrogen due to its potential effect on the pipe and its smaller molecule that can permeate the material. In the Netherlands, experimental projects are carried out with the Thermoplastic composite pipe (TCP), in an attempt to create a suitable pipe for transporting hydrogen. Today the TCP, which consists of multiple layers, including a plastic liner, an aluminum layer and synthetic fiber reinforcements, is forming the basis of a hydrogen gas transport network in the country, supporting its climate-friendly pro-hydrogen policy of replacing natural gas.

One way to increase the sustainability of plastic pipes would be the use of recycled materials. While other products, such as PVC window frames, are now made of recycled material, most plastic pipes still use virgin plastic so as not to jeopardize strength and durability. Although sewage and drainage pipes can use recycled plastics, pressure pipes that transport water or gas at high pressure need to have a limited risk of failure. Yet, according to Nigel Cassidy, Professor of geotechnical infrastructure engineering at the University of Birmingham, UK, experimental projects are now carried out with a local pipe manufacturer Aquaspira, where a 100% net-zero pipe is tested. Maybe this is not feasible today, but new technologies and research and development (R&D) can definitely help create new products and markets.

Conclusion

Plastics are essential for daily use, both for consumers and industrial processes alike. Over the last 2 decades, the plastic industry has grown at an unprecedented rate, surpassing economic growth as well as the growth in other industries, such as steel, aluminum, and cement. The multitude of global disruptions, including the climate crisis, water shortages, weather volatilities, and the energy crisis exacerbated by the Ukraine war, will definitely leave a mark on the plastics industry.

The plastic industry is a highly resource-intensive industry that requires large amounts of oil, gas, and water for production. The current global droughts and water shortages are affecting the sector in many countries, as water access is becoming more limited for producers, affecting their daily operations. Moreover, with the unresolved disrupted supply chains from the COVID-19 pandemic and the recent conflict in Russia and Ukraine, the soaring oil prices are also pushing plastic and resin prices up. With large price increases come large demands to reduce the energy use in the creation of plastics and an increased demand for circularity.

The plastics industry is known to have a significant environmental footprint, whether through the never-ending plastic waste that leaks to land and oceans, or the non-negligible carbon emissions throughout its lifecycle. With the recent UN resolution to end plastic waste in place, and the expected signing of the legally binding draft by 2024, the plastic industry is expected to start seeing changes with more shifts towards recycled and alternative solutions.

As we’ve seen, the main cause of concern is not the use of plastics per se, but rather how plastics are being used. The dramatic rise of single-usage plastics, coupled with poor recycling and disposal of plastics has had a growing impact on the environment. Fortunately, technology is driving a transition of the industry into a more circular one, albeit at a slow rate. Hopes are that a coordinated regional and global ambition for change will start pushing it faster on this path. The use of recycled plastics, as well as alternatives for packaging, can hugely reduce the pressure on the environment. While single-use plastic might be the largest problem, more durable plastic can provide solutions, such as advanced pipes, that can actually boost sustainability by reducing water usage and transporting hydrogen for energy. If the industry can focus production on durable recycled plastics for such applications, extensive progress will be achieved.