On June 18th and 19th, the FOMC will meet to discuss monetary policy. Similar to the January 2019 meeting, the members of the FOMC appear to be indicating the Fed’s nervousness over a rapidly slowing economy and their intent to lower interest rates. As well, President Donald Trump is in Fed attack mode accusing the central bank of making a “big mistake” with its interest rate hikes while suggesting that current Fed policy was undermining him in negotiations with China. (1)

On June 4th, Fed Vice Chair Richard Clarida said the economy is in a good place but he and his fellow central bankers are willing to take action if conditions change. (2) As well, Fed Chairman Jay Powell went further to calm markets and stoke belief the central bank would cut rates in response to the trade disputes, “We do not know how or when these issues will be resolved,” Mr. Powell said of the United States’ trade disputes with Mexico, China and other nations. “We are closely monitoring the implications of these developments for the U.S. economic outlook and, as always, we will act as appropriate to sustain the expansion, with a strong labor market and inflation near our symmetric 2 percent objective.” (3)

The markets are now pricing in the interest rate cuts. The CME 30 Day Federal Funds Futures contract is now showing in a 50% chance of a 25 basis point rate cut next week, 100% chance of 25bp by August, almost 100% chance of 50bp in rate cuts in October, and almost 100% chance of 75bp rate cuts by January 2020. (4)

Let’s take a quick review of a few economic items the Fed may be considering heading into their meeting.

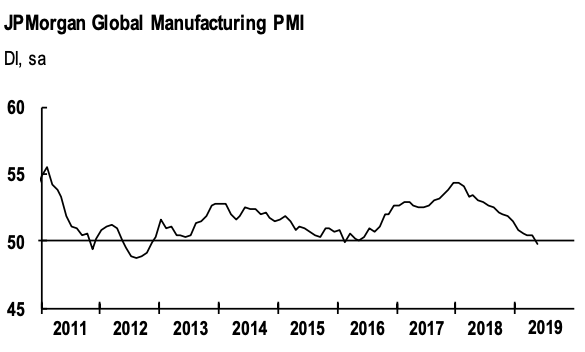

First, As an example of the economic impact from the trade wars, the JP Morgan Global Manufacturing PMI shows a steady decline since the US tariffs began in January of 2018.

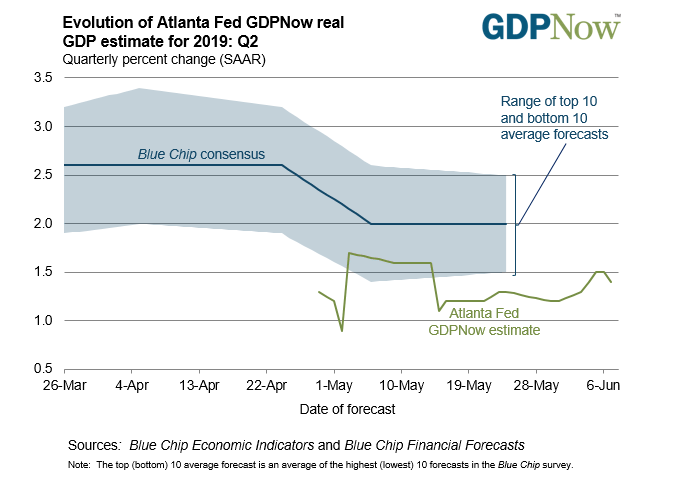

The estimates for US Q2 GDP are less than half of the 2019 Q1 3.1% GDP.

Next, let’s take a look at two leading Federal Reserve District GDP models to see what they are predicting.

Up first, the Atlanta Federal Reserve 2019 Q2 GDPNow model shows US GDP at 1.4% with Blue Chip consensus at 2.0%.

Next, the New York Federal Reserve 2019 Q2 GDP NowCast model and this is a lower estimate at 1.0%.

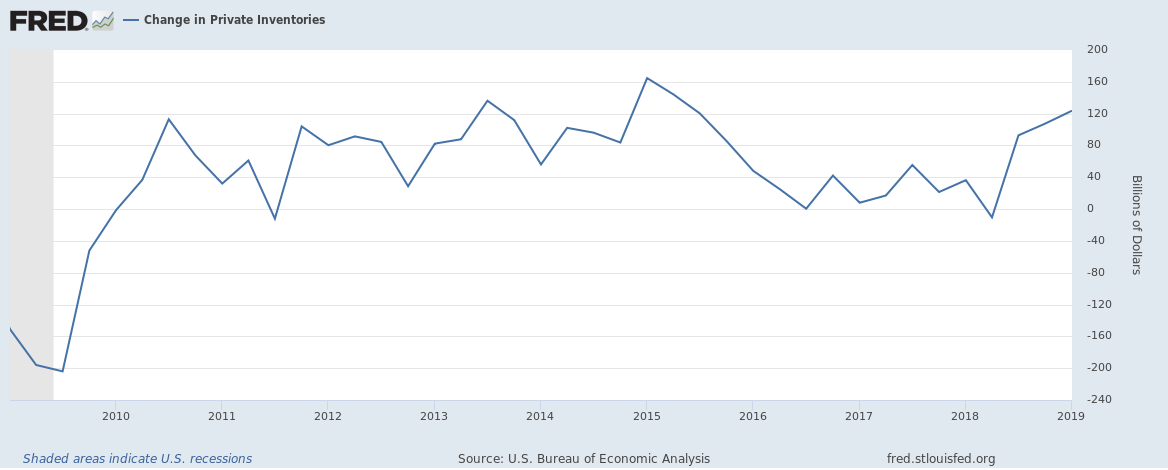

Please note, the Total Business Inventories number on this table shows a decrease from the last GDP estimate. I think this is worth pointing out because increases in private inventories helped significantly increase GDP in 2018 Q3, 2018 Q4, and 2019 Q1. The chart below shows the change in billions of dollars.

What’s worrisome here is the average Q1 inventory over this 10-year period is $63 billion and 2019 Q1 was almost double the average. To me, a large inventory adjustment is likely to occur because inventories were built up in anticipation of the 25% tariffs on Chinese goods, and inventories are likely to be run down even if the trade war continues. Companies are likely to use the lower cost imports/inventories before ordering new inventory.

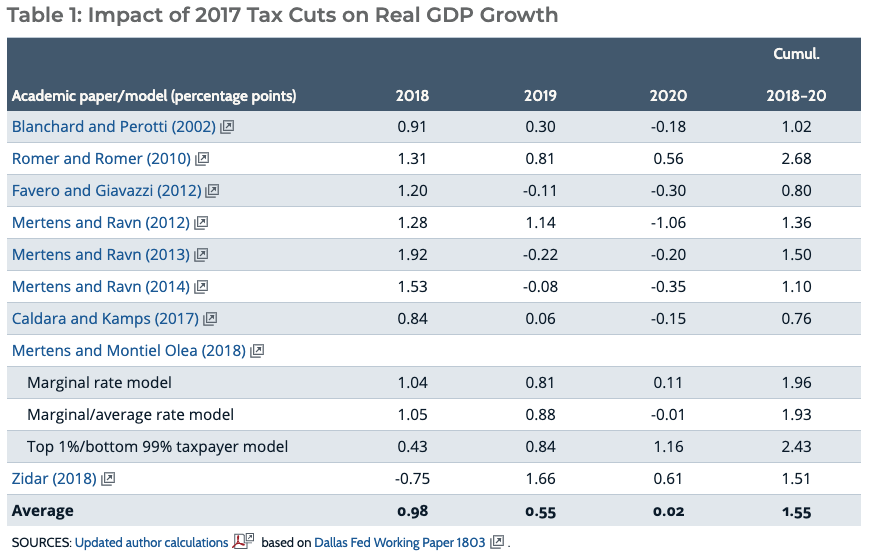

Lastly, as depicted in the chart below, researchers are anticipating a smaller stimulus from the 2018 tax cuts. The Dallas Federal Reserve compiled a list of academic papers and models estimating the impact to GDP from the 2017 tax cuts. In 2018, the tax cuts gave an average 0.98% boost to GDP. In 2019, the estimate is 0.55%. In 2020, the estimate is 0.02% or flat.

In summary, President Trump and the Fed are likely seeing risks from an extended trade war, a potential sharp reduction in private inventories, and waning stimulus from the 2018 tax cuts that could lead to negative GDP. Both the Fed and President Trump are making it known to the markets their concerns over economic growth. The risk is that both are right and both are wrong. They’re right in pointing out the problem. The Fed is wrong in the lack of action by the central bank to stop quantitative tightening and cut rates. President Trump is wrong by his lack of ending the US-China Trade war and continuing to create supply chain disruptions via his tariff threats on Mexico.

- https://www.politico.com/story/2019/06/10/trump-federal-reserve-interest-rate-hikes-1358816

- https://www.cnbc.com/2019/06/04/vice-chair-clarida-if-economy-slows-fed-will-implement-policy-to-keep-it-in-a-good-place.html

- https://www.nytimes.com/2019/06/04/business/economy/powell-fed-trade-wars.html

- https://www.cmegroup.com/trading/interest-rates/stir/30-day-federal-fund.html

- https://www.markiteconomics.com/Public/Home/PressRelease/b2eb8a67afb44a4299eff370169f603e

- https://www.frbatlanta.org/cqer/research/gdpnow.aspx

- https://www.newyorkfed.org/research/policy/nowcast

- https://fred.stlouisfed.org/graph/?g=o9MH

- https://www.dallasfed.org/research/economics/2019/0604