Trade is now power. Resilience is the new advantage. The next decade belongs to the companies that build AI-driven supply chains that can’t be broken, bullied, or blocked.

🔥 Breaking Geopolitics Update: U.S.–China Trade Showdown Reloaded

The U.S.–China rivalry didn’t cool off this week—it accelerated. In the last 24 hours, Washington and Beijing moved toward a temporary trade framework to prevent another tariff explosion. The deal would hit the pause button on Trump’s threatened 100% tariffs on Chinese imports, while China agreed to delay new export controls on rare earth minerals—the lifeblood of U.S. defense systems, EVs, and advanced chips. Beijing also signaled a restart of U.S. soybean purchases; a strategic move aimed squarely at America’s farm belt.

But let’s be clear—this isn’t a return to globalization-as-usual. It’s deal-by-pressure, not partnership. Both sides are negotiating with leverage, not trust. China is still playing the long game on industrial dominance. The U.S. is still building economic walls around strategic tech. Nobody’s backing down—they’re just reloading.

This moment proves our theme of Globalization 2.0: trade is now national security, and supply chains are geopolitical terrain. Tariffs aren’t taxes anymore—they’re tactics. Deals aren’t permanent—they’re timeouts. And the companies that survive this era will be the ones that build flexible supply strategies that adjust faster than geopolitical risk.

Overview

For decades, the goal of globalisation had been simple: Maximising global trade efficiency above all else. This pursuit for maximum efficiency led corporations to outsource production to find the cheapest labour and fastest supply chains, treating excess inventory as dead weight under the assumption that global trade would remain seamless and uninterrupted. Unfortunately, this Western-led order would eventually start to crack, with geopolitical rivalries challenging the status quo.

Welcome to what Altana titled ‘Globalisation 2.0,’ an era where the system of global commerce is being directed not by economists, but by generals, diplomats, and national security advisors. In this new environment, the key drivers are not just market dynamics, but also geopolitical events. Wars, strategic tariffs, climate disruptions, and the formation of emerging alliances are turning the previous predictable pathways of global trade into a contested geopolitical chessboard of uncertainty.

Our aim here is to show that geopolitics is no longer a backdrop, but the economy, reshaping growth, supply chains, and financial markets. However, we also want to shed some light into the opportunities in this fragmented environment.

Here’s a quick summary:

Globalization isn’t over — it’s under new management. Security now beats efficiency as wars, cyber threats, and rival blocs reshape the world economy.

Politics hijacked the supply chain. Tariffs, sanctions, and alliances now dictate who trades with who — and who gets cut off.

AI just became a national security asset. From digital twins to trusted networks, AI is now the weapon for surviving global turbulence.

Cheap is out. Resilient is in. Companies are rewiring everything around de-risking: nearshoring, friend-shoring, and “China +1” aren’t strategies — they’re survival.

The winners? The adapters. In Globalization 2.0, the edge goes to those who think faster, move earlier, and build smarter networks than their rivals.

How Geopolitics is driving Economic Shifts.

In Globalisation 2.0, geopolitical events are no longer the background music in trade, they have become key in shaping the trajectory of global economic change.

In its earlier forms, globalisation’s main objective was simple: making trade as cost-effective and seamless as possible, however these days have passed. As we see across news and government sources, tariffs, sanctions, and restrictions have taken centre stage, with emphasis on strategic imperatives, national security, and political alliances all dictating the flow of trade goods and capital.

These changes have materialised and are actively shaping the core economics of multiple nations, creating a new economic reality that ultimately leads to an age of fragmentation, strategic competition, and trade resilience over pure efficiency. The four main areas of influence that we will be analysing are wars/ conflicts, alliance/ blocs, tariffs/ trade policies, and immigration/ demographics.

Wars and Conflicts

Though wars have been a consistent factor throughout the 21st century, they were mainly on the periphery for trade planning. Yet, recent conflicts such as the Russo-Ukrainian war and Israeli-Palestinian conflict have sent shock waves across the globe, causing conflict risk and mitigation to heavily guide investment decision making.

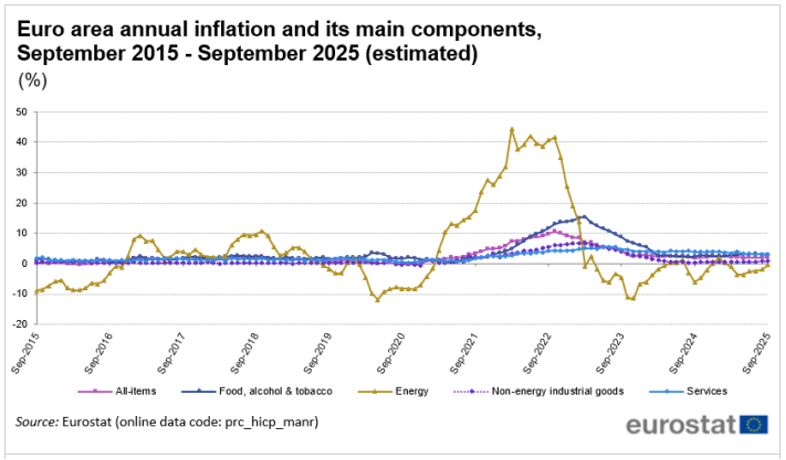

Russia and Ukraine are key examples of how conflict has impacted energy markets and trade flows. Russia supplied the EU with 150 billion cubic meters (BCM) of gas in 2021, the largest provider of gas at the time. Likewise, Ukraine was a significant source of global grain and sunflower oil. However, the emergence of this conflict has led to sanctions against Russian gas and large supply chain bottlenecks in Ukraine. As a result, EU energy inflation rose to a record high 41.9% in late 2022, while food inflation climbed to over 19% by early 2023, reflecting the severe price shocks in both sectors.

Figure. 1. Source: Eurostat. Inflation in the euro area.

Within the Israeli-Palestinian conflict, the United Nations (UN) reported that economic activity in Gaza is “on the brink of total collapse,” while Israel also faces financial strains, highlighting how wars often heighten uncertainty and inject volatility into investor sentiment. The conflict has also raised concerns about shipping routes through the Red Sea, with attacks on commercial vessels forcing some companies to reroute around Africa, adding around 10 days and significant costs to shipping times. As a result, wars and conflicts are now central to economic planning, forcing businesses and nations to treat geopolitical conflicts not just as a remote risk due to their profound disruption to global markets.

Beyond these immediate disruptions, these conflicts have also driven nations to reallocate large portions of their budgets towards defense spending. The Stockholm International Peace Research Institute (SIPRI) highlights this trend, as world military expenditure rose to $2,718 billion in 2024, resulting in a high 9.4% year-on-year rise since at least 1988. Subsequently, we are seeing a large capital diversion away from potential investments in technology, infrastructure, or social programs.

Figure. 2. Source: SIPRI. Trends in World Military Expenditure, 2024.

With less government spending on other sectors, the risk for venture capital (V.C.) is higher, with corporations needing to re-engineer their supply chains to mitigate risks associated with conflict zones, often at significant costs. This new risk guides heavily investment decision making to mitigate conflict driven risks. Subsequently, venture capitalists and corporations are now shifting their priorities to resilience, stability, and risk diversification, over potentially higher returns but with greater risk exposure.

Alliances and Blocs

For generations, the dominant global goal was greater economic integration, guided by the U.S.-shaped system through institutions such as the International Monetary Fund (IMF) and World Trade Organisation (WTO). Yet, this foundation is now fragmented as nations form smaller political and economic blocs, challenging the old unipolar framework.

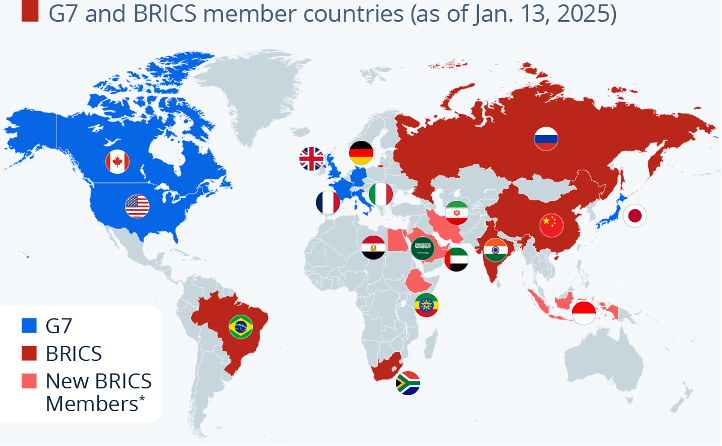

A key example is the strategic partnership between Russia, China, and India, which is pushing back against the Western-led order. We can see this evidently through BRIC, a term created by Jim O’Neill. O’Neill, then chief economist at Goldman Sachs, coined the acronym in 2001 to identify emerging market powerhouses with significant growth potential. While older blocs like the EU were founded on principles of shared governance and market integration among allies, or like the Association of Southeast Asian Nations (ASEAN), which focuses on regional economic integration and neutrality, BRIC represents a diverse trade and political coalition, whose founding members are Brazil, Russia, India, and China. This accumulation of power is aimed to not just bring economic trade and prosperity but to also stand as a challenge against privileged Western powers. For example, the U.S. alone holds 16.49% of voting power in the IMF, effectively granting it a large portion of veto power over major decisions, while the combined voting share of BRIC countries is less than 15%. Today, the organisation has grown to BRICS+ by adding major economies from the Middle East, Africa, and Asia.

Figure. 3. Source: Statista. BRICS Expands Footprint in the Global South.

By accumulating power, BRICS+ seeks to reshape the rules of global trade and governance, as seen through its institutions like the New Development Bank, providing infrastructure and development loans without the conditions and processes imposed by the IMF and World Bank. Since its establishment in 2014, the New Development Bank has approved over $39 billion in financing projects across member states, offering an alternative to Western-dominated financial institutions. This gives nations an alternative payment system that reduces their dependency on the U.S. dollar and opens the doors to other spheres of economic influence with their own trade rules and technological standards. For businesses, this means navigating a more complex and fragmented global market where access is increasingly determined by a company’s country of origin and its government’s political affiliations.

Tariffs and Trade Policies

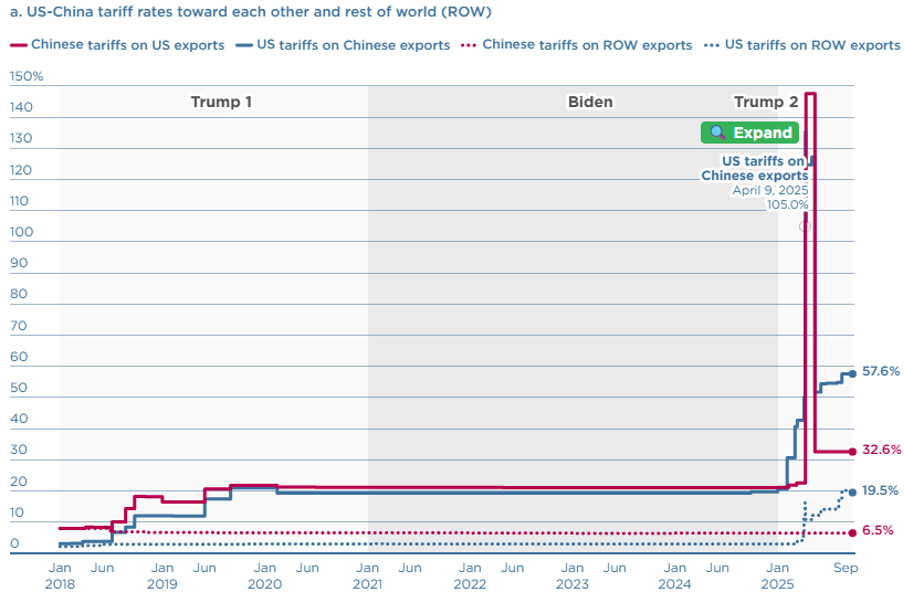

Looking back over the past year, 2025 has been a notable year of tariffs and trade policies, with Trump tariffs dominating the centre stage of discussion. Previously, trade policies were primarily an economic tool to maximise efficiency through the global trade framework, but now the era of assuming that all trade is mutually beneficial is over. Instead, we see how nations are wielding tariffs as a weaponised economic tool to protect domestic industries, safeguard critical supply chains, and counter geopolitical rivals.

As previously mentioned, Trump tariffs are a prime example of this as the U.S. moves away from free trade orthodoxy and toward a more protectionist, strategically driven trade policy. This is particularly evident if we analyse the U.S.-China trade restrictions, where high-tech goods at low prices are hurting many domestic markets in the West. In response, a targeted tariff on Chinese exports was established on April 10th, with the U.S. imposing a 135.3% tariff and China responding with a 147.6% tariff before both cooling off in May.

Figure. 4. Source: PIIE. US-China Trade War Tariffs: An Up-to-Date Chart.

Looking at the timeline chart, we can see how volatile trade wars can be, leading to a rapid escalation that causes supply chain issues for many companies like Apple, which utilise China extensively due to its low labour costs and high manufacturing ability. Similarly, the EU has also taken steps to protect its domestic businesses and markets through the Anti-Coercion Instrument and green tariffs, intended to enforce its regulatory standards globally and leverage its market access.

Ultimately, these tariffs have resulted in businesses needing to navigate through a minefield of politically motivated trade barriers. These potential volatile and unexpected costs are essentially drawing a geopolitical map of where to build a business that is economically sustainable with less exposure. Again, we are seeing how business is being guided by stability and risk mitigation rather than economic logic.

Immigration and Demographics

Finally, immigration has also been a subject that has reached a tipping point, with many nations staging protests that lead to economic consequences. Within the West, a nationalist wave has taken a strong root in politics with groups such as Reform UK, Alternative for Germany (AFD), National Rally, Brother of Italy (FDL), and the Trump administration. These organisations all have in common a strong conviction for tighter immigration restrictions; however, these policies can lead to mass labour shortages in critical sectors like healthcare, agriculture, construction, and technology.

In turn, this causes two major effects. Firstly, a major disruption to already existing businesses and industries. Within the U.S., the Home Builders Institute (HBI) construction labour market report for 2024 stated: “Immigrant workers now account for 24.7% of the construction workforce, a new historic high. In construction trades, the share of immigrants is even higher, exceeding 31%”. With immigration representing over a quarter of the construction force, if new restrictions are to take place, policy laws can be directly responsible for a large shortage in labour.

Figure. 5. Source: HBI. The Home Builders Institute (HBI) Construction Labor Market Report Fall 2024.

The second major disruption is that tighter restrictions can limit a sector’s potential growth. Less workers would result in work becoming a slower and more expensive process. In construction, this can lead to project delays and reduced housing supply. In turn, this reflects an uncertainty within the industry to investors, resulting in them seeking opportunities in more stable environments. In the long term, this economic strain can blunt innovation, competitiveness, and overall economic development.

Simultaneously, broader demographic pressures are emerging. Aging populations in developed countries contrast sharply with youth bulges in developing nations forcing governments to adopt national strategies to attract and sustain a workforce. By 2030, one in six people globally will be aged 60 or older, according to World Health Organization’s demographic projections. In Germany, the new Skilled Immigration Act seeks to secure a vital work force for a wide variety of “shortage occupations.” These efforts reflect a country’s recognition that skilled human capital is a key component of long-term economic power and national security, bringing in economic interests as well.

Understanding The Overarching Financial and Economic Implications.

From briefly looking at these four areas, we can see how intertwined geopolitics and economics are heavily affecting financial decision making. We see how strategic safety has become the priority compared to the old globalisation playbook of efficiency, interdependence, and open markets. It is then vital that we understand the overarching financial and economic implications that are happening as we move towards globalisation 2.0.

Interest Rates and Inflation.

One of the biggest impacts of this globalisation shift is on monetary policy, which is becoming more driven by geopolitical events rather than pure economic data. From our previous analysis, we can see how wars, supply chain bottlenecks, and strategic tariffs prime drivers of inflation are, with their effects overflowing into other nations or an entire region. Furthermore, as the European Central Bank (ECB) demonstrates, geopolitical events are intensifying further.

Figure. 6. Source: European Central Bank. Addressing the impact of geopolitical risk.

These inflationary pressures put a lot of strain on central banks worldwide. In response, banks have had to adjust their policy frameworks to account for larger political uncertainty, disturbances and risks surrounding large global fragmentation. As stated by the ECB, geopolitical risks are playing a growing role in driving inflation and financial instability, challenges that central banks have limited tools to manage. Consequently, bank policies are becoming less predictable and more reactive to geopolitical developments beyond their direct control.

Supply Chain Fragility & Trusted Networks.

Within supply chains, the “Just-In-Time” model (JIT) has been a staple system for procurement, aligning raw-material orders from suppliers directly with production schedules. What this means is that often a particular good or product would only be manufactured when there is an actual demand for it. This demand led system essentially boosts efficiency by limiting inventory costs and waste, but at the cost of significant supply chain vulnerability.

Most notable, this model saw its flaws exposed during the COVID-19 pandemic, when personal protective equipment (PPE) saw a spike in huge demand worldwide. In March 2020, N95 and KN95 masks purchases increased by 14000%. The combination of high demand and Chinese manufacturing being unable to meet production goals due to pandemic restrictions led to months of delays, greatly affecting foreign health care systems.

Whilst this model is still in use today, it is often implemented as a hybrid model, intertwined with “Just in case,” to avoid any large-scale catastrophes or supply chain disruptions. The just in case model aims to strategically hold inventory even during times of low demand. Whilst this does incur a higher cost of inventory holding, it mitigates supply chain disruptions, preventing a reduction in lost sales during high demand.

This strategic shift also involves the process of nearshoring (moving production closer to home) and friend-shoring (relocating supply chains to established allied countries), creating regional blocs of trade and manufacturing. We can see this diversification in agreements such as the United States-Mexico-Canada Agreement (USMCA), where Mexico and Canada account for a combined 28.2% of total U.S. trade. Likewise, the U.S. have also expressed interest in investing in allies Australia, raising $200 million USD to support the development of its Goschen rare earths and mineral sands project. This not only strengthens the partnership between allies but also reduces vulnerability on foreign powers like China, who have a near monopoly on mining (60%) and processing (90%) of rare earth materials vital to high tech goods.

This new strategy of nearshoring and friend-shoring is more than just geographic changes; they are part of the process in creating a “Trusted Networks” operation. The goal of these AI-powered frameworks is to create a data-driven transparency system, allowing partners, businesses, and investors to forecast and withstand potential disruptions to their supply chains. Groups such as Siemens are already implementing AI technologies like Scoutbee, evaluating suppliers against set criteria and price parameters, without any human intervention. In turn, this has led to a 90% reduction in procurement workload, whilst maintaining security.

AI as Enabler

As AI continues to evolve, its role is shifting from a back-office efficiency tool, like the procurement example at Siemens, to essentially a digital AI asset strategist, managing supply chains effectively despite geopolitical complexities. While traditional predictive models can accurately forecast future outcomes based on historical data, their power is limited. New generative tools like active simulations and decision automation create millions of hypothetical scenarios before assessing which is the most optimal path.

At the core of this new tool are digital twins, “a virtual replica of a physical object, person, or process that can be used to simulate its behaviour to better understand how it works in real life,” as stated by McKinsey & Company. In the global supply chain, this virtual twin can replicate an entire supply chain through continuously being fed data from Internet of Things (IoT) sensors on shipping containers, providing real-time logistics reports, satellite weather data, and even political news feeds. This torrent of data can give businesses the ability to proactively stress test their operations to specific scenarios, rather than reactively responding to disruptions.

Figure 7. Source: Hapag-Lloyd. Smart Shipping: Internet of Things and Sensor Technology in Shipping.

Already, tools such as Coupa, o9, and Blue Yonder, offer decision making with machine speed and precision for absolute certainty. For instance, it can model the cascading effects of a new tariff regime or trade war, not just on immediate costs but on supplier viability and consumer demand months down the line. Through these simulations, firms can not only better understand the levels of their own supply chain resilience but can also view potential disruptions to their partners. Additionally, this advantageous foresight can help proactively seek out potential re-route shipments, pre-qualified alternative suppliers in different regions, and adjust inventory levels with surgical precision in forecasted emergencies.

Verifiable Digital Trust Trade

With the introduction of these AI tools, the foundations for building a verifiable digital trust trade network can be laid. Even in times of high regulation and consumer demands for ethical sourcing, trust can be proven with verifiable data from IoT sensors and digital twin AI supply chain reports.

This data paired with AI tools is vital for ensuring security, compliance, and transparency as networks expand, especially surrounding complex multi-tier supply networks, with direct suppliers relying on their own network of partners that are often harder to monitor and manage. By having digital proof of the supply chain process, AI can verify that every partner, supplier, and service within a supply chain meets up to regulatory laws and standards, such as Corporate Sustainability Due Diligence Directive (CSDDD), Modern Slavery Act (MSA) and Environmental, Social and Governance initiatives (ESG). This process creates a mass auditable “shared source of truth,” often secured on a blockchain, allowing companies to provide evidence that their supply chains are clean.

What also makes this process of verifying data secure and seamless is federated learning. This process allows AI models to be trained across a large variety of datasets from multiple organisations without exposing the raw, sensitive information. How this happens is that the AI model is first installed to each organisation’s system, learning from the local data. Next the AI’s model learning from the local model (not the data itself) is then shared back to the global model, where all the learning is combined to improve the overall AI, whilst simultaneously keeping all sensitive information safely stored at its source.

Figure 8. Source: Geeks for Geeks. What is Federated Learning?

In practice, an AI model can train from a supplier’s private production data, verify its compliance, and project an accurate global model, without ever needing that sensitive data to leave the supplier’s private servers. This solves a critical dilemma when it comes to AI services: how to leverage the power of shared intelligence without compromising data privacy or security. In turn, partners can collaboratively build up a trusted network and share crucial insights while still preserving their data privacy and national sovereignty, especially in a time of complex data regulations and geopolitical events.

Challenges & Barriers

Whilst AI can offer the opportunity to build a robust framework for building trust, the real value of this technology is its ability to navigate around the geopolitical events unfolding around the world. With commercial rivalries and economic warfare ever rising, the need for verifiable, secure, and sovereign data exchange is key against the very real challenges and trade barriers now being erected. Looking into trade wars, energy volatility, political uncertainty, and nationalist sentiment, we will see how these areas are constraining trade.

Escalating Trade Wars

China and the U.S. have been the main stars when it comes to talk about trade wars, as the two dominant global players have been clashing economically. Subsequently, their escalating trade war represents a primary barrier, as their tariff regimes raise costs for other nations, producers, and consumers. The direct consequence of these actions has been the fragmentation we see in global trade today, where seamless trade flows are replaced by a patchwork of restricted and often unpredictable regulations.

Figure 9. Source: UNCTAD. Global trade update.

For businesses, this has caused operations to be more complex and expensive in an international environment, especially as blocs like the EU introduce regional digital and green tariffs, creating economic frictions that target certain nations.

Energy Security Volatility

Likewise, energy security has become deeply entangled with geopolitical rivals. We have seen through the Russo-Ukrainian war how quickly the energy market can become volatile, affecting everything from living costs to manufacturing inputs. As nations seek to diversify their energy reliance to avoid dependencies on rivals, prices often spike due to the rushed, costly, and often chaotic scramble for secure resources.

Figure 10. Source: CSCR. A Pipeline to Power: Unpacking China and Russia’s Energy Embrace.

Additionally, realignments of energy producers and consumers from geopolitical events have created further issues, for example, the Russia-China-India bloc. Russia’s energy sanctions from the EU have led them to develop their trade relationship with India and China, quickly becoming one of the largest customers. Already, the ESPO pipeline is pumping 120 million metric tons of oil to China, with future plans to establish a second line. Also, India’s crude oil imports from Russia increased from less than 1% of total imports in 2021 to over 40% by 2024, making Russia India’s largest oil supplier and demonstrating the rapid reconfiguration of energy trade flows. These agreements are not just about generating profits from a nation’s energy sector, but creating exclusive alliances, reducing Western dependency, and reshaping the global balance of energy power.

Policy Uncertainty and Regulatory Divergence

Another major barrier for multinational corporations is the legal challenges of managing businesses in a variety of economic blocs. With nations having a renewed focus on national security and strategic autonomy, new policies can conflict with other legal frameworks. This makes long-term planning exceptionally difficult and raises compliance costs.

For instance, governments are increasingly shifting the burden of proof onto importers to demonstrate clean supply chains, as seen with policies like the Uyghur Forced Labor Prevention Act. While promoting ethical standards, there are more framework pressures that create significant operational hurdles. This divergence complicates global operations, forcing companies to employ highly customised strategies at a large expense for each market they operate in.

Rising Economic Nationalism and Populism

Finally, the rise of nationalism and populism acts as a powerful constraint on global commerce in general. As nationalists put their focus on preserving their nation first, this tends to politically translate into protectionist economic policies, including restrictions on cross-border investment and immigration. Subsequently, more nationalist nations will choose to prioritise domestic interests in a narrow sense, reducing international collaboration and disrupting integrated global supply chains.

Additionally, this includes tighter restrictions on immigration, potentially severing labour from vital sectors like healthcare, construction, and agriculture, industries that are already suffering from shortages. In turn, leading nations could find themselves quickly replaced by new global leaders if there is no consistent labour force or innovation to resolve this issue.

Impact on Business and Labor

Considering the innovations and barriers in globalisation 2.0, the major transformations we are currently seeing today will impact everything, from the corporate boardroom to the factory floor. As we have mentioned before, business strategies and labour markets are favouring resilience over pure efficiency, creating new demands for skills and talent.

Corporate Strategy

The core principle of corporate strategies for decades was maximizing shareholder value by minimizing costs. Today, we are no longer seeing this trend as prominent, as corporations are adapting for resilience and risk mitigation due to growing uncertainty. This means instead of concentrating production in a single, hyper-efficient mega-factory in one country, multinational corporations are now diversifying their manufacturing footprint across different geopolitical blocs.

The U.S. tech giant Apple is a prime example of this, having to diversify over U.S fears that China will use its technological dominance to gain a military and intelligence advantage. Instead of completely abandoning operations in China, something that would severely hurt the company, Apple has instead decoupled through a “China +1” strategy, shifting part of its labour and production to India and assembling $22 billion worth of iPhones, overall representing a nearly 60% increase year-on-year. This solution allows Apple to maintain a relationship with China and simultaneously reduce U.S. concerns.

Figure 11. Source: ETFTrends. Apple Moves iPhone 14 Production to India.

As shown, geopolitical risk planning is a highly influential variable, directly dictating where the flow of capital is. Projects in politically unstable regions are now facing a higher risk premium, making them less attractive despite low labour costs and regulations. In turn, capital is flowing towards sectors aligned with national security interests, such as defence, cybersecurity, and domestic renewable energy production. The U.S Internal Revenue Service implemented the Inflation Reduction Act (IRA), which offers significant tax incentives to attract investors to the U.S energy sector.

Ultimately, to survive in this fast-changing economy, senior roles such as Chief Financial Officers and Chief Information Officers are broadening their skillsets by working with geopolitical analysts. In turn, long-term corporate planning can become more agile, prepared, and resilient for any sudden changes, whether on a small- or large-scale event.

Workforce Dynamics

As corporate strategies evolve, so too does the labour market, with new skill sets emerging to meet corporate demand. As referenced above, geopolitical risk analysts are one role that large corporations are now employing in-house, a shift from their traditional positions in think tanks and government agencies, primarily providing intelligence on emerging threats. Additionally, supply chain managers are no longer solely logistics experts; the introduction of AI into supply chain operations now require them to interpret complex data sets and oversee AI-driven platforms that model disruptions in real time.

However, one of the biggest booms has been in work related to national security. With the new target of 5% GDP spending commitment to defence (3.5% for core defence requirements and 1.5% for broader security needs), NATO countries have generated a substantial amount of labour in these areas. Companies like BAE Systems, Fincantieri, Rheinmetall and more have been seeking aerospace and software engineers for advanced weapons systems, skilled manufacturing workers like welders and machinists to build hardware, and cybersecurity analysts to protect critical national infrastructure, all of which are in high demand.

This growth, however, stands in stark contrast to the labour challenges emerging elsewhere. Rising nationalist sentiment in the West has resulted in tighter immigration policies, causing key sectors already under strain to face acute labour shortages. In the UK, an official inquiry revealed that 60% of the 60,000 workers in the horticulture sector are migrants employed on six-month visas. Additionally, the government has plans to cap seasonal worker visas at 43,000 in 2025 to reduce dependency on foreign labour. This comes at a time when farmers are already struggling to fill vacancies. Ultimately, policy makers have a paradox on their hands: choosing political ideas for tighter border restrictions or addressing the critical labour shortages that threaten economic stability and the viability of essential industries.

Future Opportunities

As trade agreements are broken, barriers constructed and supply chains disrupted, new opportunities are arising in globalisation 2.0. Four sectors are poised for significant growth: energy, defence industries, AI, and regional trade growth. These sectors can seriously define the next decade of economic expansions. Furthermore, this analysis will also explore both the current and emerging key players in this transformative shift.

Energy, transitions, and security.

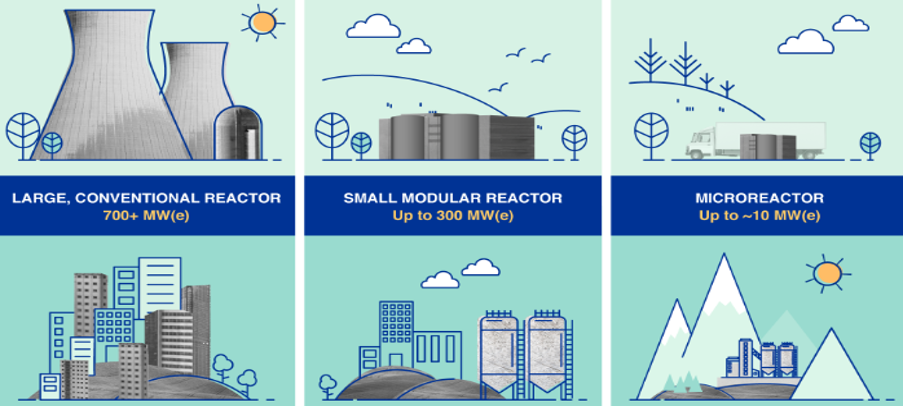

Energy has become a central concern for both climate change and national security, with events such as Russia’s weaponisation of natural gas severely disrupting the European Union’s energy supply. Determined not to repeat the same mistakes, nations are now seeking alternative suppliers and substitute energy sources. This scramble has triggered a boom in Liquefied Natural Gas (LNG) as countries work to diversify supply chains. In addition, nuclear power has become a point of reconsideration, with investments rising by 50% over the past five years due to its stable, carbon-free energy and potential to change the energy sector with the introduction of small modular reactors (SMRs).

Figure 12. Source: IAEA. What are Small Modular Reactors (SMRs)?

On the other hand, strategic competition with China’s dominance in EVs, solar panels and other green technologies have accelerated massive public and private investment in domestic renewable energy manufacturing and the development of secure supply chains for critical minerals. In particular, rare-earth materials have become essential components of these technologies, creating significant opportunities for resource-rich allies from Australia to Latin America’s lithium triangle.

The critical issue for the world is that China mines 60-70% of rare earth metals and refines 90% of them. This is not a problem you can simply through funding at and get a solution. This requires overcoming decades of China investment and relying on new players like Africa to begin building the full stream of rare earth production. It will take between 10-15 years to make a significant impact and therein lies a major risk for defense industries (and others) around the world who rely on these materials.

Defence and Security Industry

As we have mentioned before, the increased investment in national defence and security has not only generated a plethora of jobs, but has also expanded the global defence market. Rising defence budgets are driving demand not only for traditional aerospace and naval platforms but also fuelling next generation capabilities and innovations. The Global Combat Air Programme (GCAP), a collaboration between the UK, Japan, and Italy illustrates this trend. The multi-billion-dollar initiative aims to develop a sixth-generation fighter jet, creating thousands of high-skilled jobs and funding cutting-edge R&D in AI, autonomous systems, and advanced sensors technologies. This evolution demonstrates how next-gen technologies, developed as a direct response to the growing capabilities of other nations, attracts additional investments while also heightening the potential for arms races as geopolitical uncertainty intensifies.

AI and Digital Resilience

Although we have mentioned AI briefly in the previous section, its application within supply chains represents a critical strategic asset. Digital twins, virtual replicas of physical supply chains, offer a complete real time visibility into the whole supply chain process, predicting model disruptions before they occur and how to mitigate them. Similar to defence spending, as more political uncertainty grows, so too will investment. These tools help navigate through volatile global conditions by identifying risks, automatically executing mitigation strategies, sourcing from alternative suppliers, and ensuring legal compliance within trusted networks. In both the long and short term, AI can really reinforce its value.

Regional trade growth

Finally, regional trade growth can really define global trade over the next decade. As companies seek to de-risk from over concentrated single markets like Chinese manufacturing, supply chains are being completely reorganised around strategic allies. At this time of writing, the North American bloc is becoming more integrated with manufacturing, with Mexico emerging as a major beneficiary of the nearshoring trend. In Asia, the “China+1” strategy is funnelling massive investment into Malaysia, Thailand, and Vietnam, establishing them as the next generation of global manufacturing hubs.

The Key Players

Throughout this article, we have mentioned a plethora of key players. Nations, corporations, and international institutes have all been affected in this new global overhaul, creating massive waves in global trade and order.

In terms of nations, the U.S., China, and Russia are major actors, with their actions ultimately redefining geopolitical dynamics, influencing economic policies, and reshaping alliances at both regional and international levels. These three global powers are major drivers of change, and it is crucial to consider how their policies impact not only their domestic economies but also the broader global system. In particular, the increasingly volatile relationship between the U.S. and China is something to continually monitor, with Trump threatening again a 100% tariff despite a lack of sustainability. In turn, we could be seeing a large inflation in consumer goods prices if this plan continues, proving how corporations must cultivate strong resilience and adaptive strategies to these sudden and uncertain political changes.

On the other hand, the EU has been consistently leveraging its influence as a regulatory power rather than as a manufacturing competitor. Sometimes referred to as the ‘Brussels effect’, the EU’s regulations are often setting the standards for global norms, such as the data protection act, giving a unique soft power that shapes the global frameworks without direct economic coercion. The EU’s General Data Protection Regulation (GDPR), implemented in 2018, has been adopted or significantly influenced data privacy laws in more than 140 countries, demonstrating how European regulatory standards can reshape global business practices through governance and normative influence rather than force.

Likewise, India’s rising importance on the global stage is also something to watch out for. The country is growing as an important swing state that works with different superpowers such as the U.S., Russia, or China, depending on the issue. Last in national power is the Gulf states with Saudi Arabia, the United Arab Emirates and Qatar controlling massive amounts of energy resources, especially oil and gas. Their influence in the energy market often translates also into international political power and economic negotiations.

For corporations, this organisational shift has centred around defensive actions, favouring stability as political uncertainty grows. In turn, defence giants like Rheinmetall and Lockheed Martin are expected to experience sustained growth, driven by increased military spending due to fears over geopolitical conflicts. Likewise, in an energy sector, oil, and natural gas companies like ExxonMobil may see continued reliance on fossil fuels as a stable solution amid energy security concerns. Alternatively, Ørsted, a global leader in green and offshore wind power, represents how innovation in green energies could be the solution to energy security and meeting climate goals.

Additionally, logistics companies are crucial in maintaining the flow of global trade and supply chains. Maersk, UPS and other logistical services will be ever more vital with the current rising trend of tariff and trade barriers, especially in a more fragmented environment. At the same time, AI firms such as Microsoft, OpenAI, and Palantir are continually evolving the AI industry and security, with innovations in cloud computing, data analysis, and artificial intelligence becoming critical tools in both corporate and government strategies.

Finally, international institutes are facing new challenges. The WTO and IMF have had to adapt to the increasing pressures of political uncertainty by issuing revised frameworks and policy recommendations to uphold stability. Alternatively, security alliances like NATO have been revitalised due to conflicts in Ukraine and Russia, pressuring more security measures from each of its participants. Emerging blocs like BRICS+ are also something to look out for, as they promote alternative economic paths that challenge Western dominance, reliability and are growing in geopolitical influence.

Foresight Over Efficiency

The strategic implications of globalisation 2.0 have changed the rule book for globalisation. The competitive advantage is no longer about how efficient a supply chain may be, but about foresight and resilience. In turn, the winners of globalisation 2.0 will be the first movers who build AI-enabled trusted networks, positioning themselves to dominate trade and capital flows of the coming decade. For corporations, the ability to integrate geopolitics into their forecasting will be a core value in determining risk and give them a competitive edge. Those who fail to adopt will risk not falling behind but breaking entirely.

However, this does create a bit of a difficult scenario: how much efficiency must corporations sacrifice in pursuit of stability? The balance between political risk and market opportunity will be a consistent factor that needs to be re-evaluated as forecasting and geopolitical events unfold, ultimately turning every investment decision into a geopolitical one too. In short, there will be opportunities for wealth as nations dial back on dependencies, but how much are you willing to risk for them?

As these corporate and national choices accumulate around trade, security, and alliances, a critical question emerges: will nations continue to double down on fragmentation into fortified economic blocs, or will shared global challenges cause the emergence of new, more pragmatic alliances built for mutual stability? In the end, it is these decisions that will define both the economic and political framework for the next decade.

Wrapping it up

In the new globalization 2.0, geopolitics drives economics. Global power competitions, regional conflicts, and strategic decoupling have fractured what was once a unified global trading system, forcing a complete overhaul of how international commerce and finance are conducted.

The evidence is clear: wars are disrupting energy and food supplies, alliances are reshaping financial systems, tariffs are being used as political/economic weapons, and immigration policies are limiting labour markets. Each of these forces, examined throughout this analysis, demonstrates how deeply geopolitical considerations have penetrated the foundation of economic decision-making.

However, amid this fragmentation, corporations are adapting, seeing that success is no longer in efficiency, but from resilience to geopolitical changes.

Yet a paradox persists. How much efficiency must be sacrificed for stability? How much growth for security? These are not questions with universal answers but calculations that must be continually reassessed as the geopolitical order shifts. What is certain is that ignoring these questions is no longer viable. The just-in-time model that defined globalisation 1.0 lies shattered, exposed as fundamentally incompatible with a world where supply chains are strategic assets and economic dependencies potential weapons.

Fo success, companies must use all the tools at their disposal: leveraging AI for supply chain visibility, investing in trusted networks, and capitalizing on major opportunities in the energy, defence, and technology sectors. In turn, the winners of the next decade will thrive not despite geopolitics, but because of their ability to navigate and harness its opportunities.