America Arrives with Less Leverage Than It Thinks

What the Trump–Xi Meeting Means for Tariffs, Technology, Rare Earths, EVs, Iran, and Taiwan

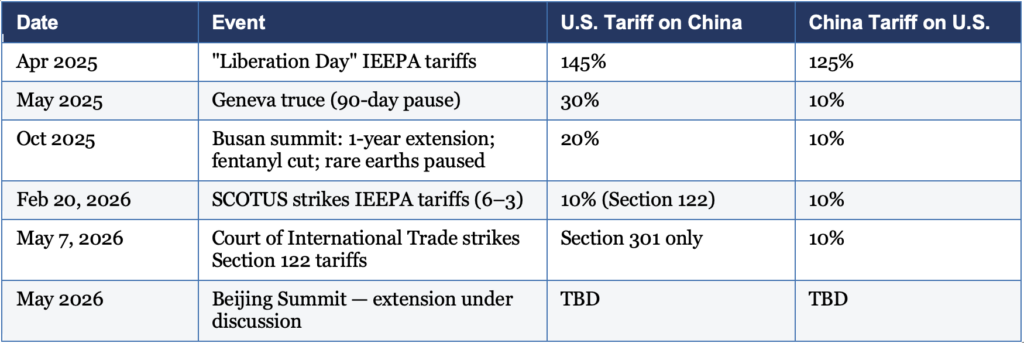

Trump arrives in Beijing as the most tariff-aggressive president in a century — and one of the most legally constrained. The Supreme Court stripped his primary tariff authority in February. His replacement tool expires in July. He may need Xi more than Xi needs him.

This is the paradox at the center of the 2026 Beijing Summit: a U.S. president walking into negotiations with real strategic interests but significantly diminished unilateral leverage. Understanding that gap — between America’s long-term position and its short-term tools — is essential for any executive planning around supply chains, capital allocation, or global market exposure in the second half of 2026.

The operating framework: Call it Managed Rivalry. Neither side wants war. Neither can afford a complete break. The U.S. and China are simultaneously the world’s two largest economies and its two most powerful adversaries. The Beijing summit is not a negotiation about resolving that rivalry. It is a negotiation over the rules for managing it — for the next 12 to 18 months.

Why This Matters: Six Strategic Implications

- Your supply chain has a single point of failure you cannot fix before this summit ends. China controls approximately 90% of global rare earth processing. If the export license arrangement from the London talks is not extended, U.S. manufacturers — including defense contractors — face immediate supply disruption. Ford already paused Explorer production over magnet shortages in 2025. The Pentagon paid a 40% premium to secure supply. This is not a hypothetical risk.

- The tariff floor just moved — and so did the ceiling. With IEEPA struck down and Section 122 legally contested and expiring July 24, the administration’s unilateral tariff power is at its lowest point since 2017. Whatever rates come out of Beijing — or fail to — will be set primarily through Section 301 investigations. Those take months and create a paper record that courts can review. Plan for durability, not volatility.

- China won the EV race. The competitive threat isn’t at the border — it’s in your export markets. U.S. tariffs kept Chinese EVs out of America, but BYD simply went to Brazil, Southeast Asia, Australia, and Europe instead. Markets American automakers once considered secure are now contested. As Ford CEO Jim Farley put it, Chinese EVs are “the most humbling thing I’ve ever seen.” The summit will not change that dynamic.

- The Iran war handed Xi leverage he didn’t have to ask for. China buys approximately 90% of Iranian oil exports. With the Strait of Hormuz under pressure, Trump publicly needs Chinese cooperation to keep energy flows stable. This is the first moment in this rivalry where Washington arrives needing something from Beijing — not the other way around.

- Chips are Washington’s last real trading card. Nvidia’s advanced AI processors and EDA design software remain genuine bottlenecks for Chinese semiconductor ambitions. China’s chip self-sufficiency stands at roughly 33% domestically. Every year of effective export controls is a year the technology gap does not close. Beijing knows it. Any chip concession will come at a price.

- A partial deal is the most likely outcome — and the riskiest scenario is the one markets aren’t pricing. The tariff pause, rare earth stability, and supply chain confidence all rest on the assumption that Beijing produces at least a minimal agreement. Scenario 4 — summit collapse — is only 10% likely. But none of those conditions is guaranteed if talks fail.

I. Lower Tariffs, Higher Uncertainty

The trade war peaked in April 2025, when U.S. tariffs on Chinese goods hit 145% and Chinese counter-tariffs reached 125%. The Geneva truce dropped both sides significantly. Subsequent talks in London, Paris, and Busan maintained the pause while extending it through late 2025. Trump arrives in Beijing with tariffs at roughly 33–35% on most goods — but without the legal architecture that held them at 145%.

On May 7, 2026, the U.S. Court of International Trade struck down the Section 122 tariffs in a 2–1 ruling, finding the administration had not met the statutory threshold required to justify them. Trump has signaled he will pursue tariffs through other legal routes — primarily Section 301. This further narrows unilateral tariff options heading into Beijing.

The arithmetic of trade deficits is also working against the U.S. negotiating position. The goods deficit with China fell from $295 billion in 2024 to $202.1 billion in 2025 — but the overall U.S. trade imbalance with the world did not shrink. It shifted to Vietnam, Taiwan, and Thailand. Tariffs redirected supply chains; they did not change the underlying U.S. consumption pattern. No summit deal changes that structural reality.

II. The Chip You Can’t Buy and the Metal You Can’t Mine

AI Chips: Washington’s Last Clear Leverage

In January 2026, the U.S. Bureau of Industry and Security shifted its approach on advanced AI chip export licenses for China from automatic denial to case-by-case evaluation — a partial easing. China wants more: the full removal of restrictions on Nvidia H200 processors, advanced AI accelerators, and EDA software, which remain the most painful bottlenecks for Chinese domestic semiconductor development.

Nvidia and advanced semiconductor exports represent something China genuinely cannot yet replicate domestically, which makes chips one of the few areas where the U.S. holds concrete leverage. Any concession is likely to be packaged — chips for rare earths, chips for Iranian restraint, chips for purchase commitments. Watch for what moves with them.

Semiconductors: The Long Game

China’s chip self-sufficiency stands at roughly 33% of domestic consumption, with a stated five-year plan targeting 80% by 2030. That goal mirrors the earlier Made in China 2025 target of 70% by 2025, which fell substantially short. The ambition is real; the timeline is not.

For the U.S., every year of effective export controls is a year the technology gap does not close. The technology competition is not about near-term trade balance — it is about who controls the foundational infrastructure of the global economy over the next 30 years. That is the frame through which every chip concession at this summit should be evaluated.

Rare Earths: The Supply Chain Landmine

China is the leading refiner for 19 of 20 important strategic minerals, processing approximately 90% of global rare earth supply. These are the elements essential to permanent magnets, EV motors, wind turbines, and advanced weapons systems.

In early 2025, China imposed export restrictions and the effect was immediate: Ford temporarily paused Explorer production over rare earth magnet shortages, and the Pentagon moved to stockpile materials — paying a 40% premium above market prices to secure supply through a 10-year offtake agreement with MP Materials.

Following the London talks in June 2025, Beijing agreed to gradually restart export license approvals over six months. That arrangement is now up for extension at this summit. The most likely result is a one-year pause on new restrictions in exchange for U.S. concessions on semiconductor export controls.

III. China Won the EV Race. America Didn’t Notice.

In 2025, BYD sold 2.26 million battery-electric vehicles, surpassing Tesla’s 1.64 million for the first time in annual pure EV sales. Six of the world’s ten largest EV manufacturers are now Chinese. BYD’s overseas sales exceeded one million vehicles in 2025 — more than double the prior year — with factories opening in Hungary, Turkey, and Brazil.

U.S. tariffs kept Chinese EVs out of the American market. BYD simply went elsewhere. American automakers are now facing Chinese competition not in Detroit but in Brazil, Southeast Asia, Australia, and Europe — markets they once considered secure. When Ford CEO Jim Farley described Chinese EVs as “the most humbling thing I’ve ever seen,” he was not exaggerating. He was acknowledging a competitive reality that much of corporate America has not yet fully absorbed.

EVs themselves are unlikely to be a central point of contention at this summit. China has little incentive to make them one — it already leads and the lead is widening. The more consequential issue involves batteries, critical minerals, and the battery technology supply chain that supports both the energy transition and the defense industrial base. China’s export controls on battery manufacturing technologies — partially suspended under the Busan agreement — are part of what gets extended or formalized in Beijing.

IV. The War That Gave Xi Leverage He Didn’t Have to Ask For

The Beijing summit was originally scheduled for late March. The Iran war pushed it to mid-May, giving Beijing additional preparation time — and more importantly, altering the strategic environment before either side entered negotiations.

China is the world’s largest buyer of Iranian oil, accounting for approximately 90% of Iran’s exports. The stability of the Strait of Hormuz is a matter of Chinese national economic security. When Trump publicly stated he needed China’s help keeping the Strait open — and predicted Xi would give him “a big, fat hug” in Beijing — he was acknowledging a shift in the negotiating dynamic that is easy to understate.

This is the first moment in this phase of the rivalry where Washington arrives in Beijing needing something from Xi — not only offering concessions but requiring cooperation. Trump has threatened a 50% tariff on Chinese goods if Beijing is found supplying weapons to Iran. On April 24, the U.S. Treasury sanctioned five Chinese refiners for buying Iranian crude. Eight days later, Beijing invoked its blocking statute for the first time, ordering all Chinese entities to refuse compliance. That was a deliberate pre-summit signal: China intends to set the terms of engagement.

The most likely outcome is that Iran-related understandings become part of the broader bargain — exchanged for concessions on Venezuelan oil purchases, export controls, or tariff implementation timelines. Of all the issues on the Beijing agenda, Iran is the one where Washington has the least leverage and the most urgency.

V. Taiwan: Managed Uncertainty as the Best Achievable Outcome

Taiwan is, in Xi’s words, the most important and sensitive issue in bilateral relations. On the underlying question of status, U.S. and Chinese positions are fundamentally irreconcilable. No summit changes that.

In December 2025, Washington approved an $11.1 billion arms package for Taiwan, including HIMARS, ATACMS missiles, howitzers, and drones — the largest U.S. arms sale to Taiwan to date. Beijing condemned it as a serious violation of the One China principle. Yet Xi did not make cancellation a precondition for the summit. That restraint is itself a signal: Beijing is calibrating rather than escalating.

The realistic objective at this summit is preserving the conditions for stability — reinforcing military-to-military communications, strengthening crisis-management channels, and reducing the risk of miscalculation. In a relationship this tense, a functioning phone line is genuinely valuable. The most plausible outcome is managed uncertainty: neither side changes its formal position, but both signal enough restraint to keep the Taiwan Strait out of active crisis mode.

One concern worth monitoring: Taiwan has historically served both strategic and diplomatic purposes in U.S. policy. The line between security commitments and bargaining material is rarely as clean as official statements suggest. Marco Rubio has dismissed the idea. History suggests the question will remain open.

VI. Four Scenarios: What Happens and What It Means for Your Business

The Bottom Line

The Beijing summit is not a reset in U.S.–China relations. It is not a reconciliation. It is an attempt — under the framework of Managed Rivalry — to define the operating boundaries of an increasingly intense competition between the world’s two largest economies.

Beijing enters with perceived advantages: growing domestic technological capacity, dominance over critical mineral processing, a stronger position in electric vehicles, and U.S. political constraints that have narrowed Washington’s room for maneuver. Chinese leadership increasingly believes that long-term structural trends favor Beijing over Washington. Whether that assessment is accurate will depend on several factors still under U.S. control.

For executives and investors, the central question is not whether the United States and China will become partners again. They will not. The question is whether both sides can manage an increasingly intense rivalry without forcing the global economy to absorb the consequences when that management fails.