FAQs on Process, Presidential Authority and Duration

A practical FAQ for business leaders navigating U.S. trade policy • Updated May 2026

Part I: Fundamentals

1. What is Section 301 and what is it designed to do?

Section 301 of the Trade Act of 1974 is the U.S. government’s primary legal tool to investigate and respond to unfair foreign trade practices. It authorizes the U.S. Trade Representative (USTR) to act when another country violates trade agreements, discriminates against U.S. companies, or engages in unreasonable practices such as forced technology transfer or intellectual property theft.

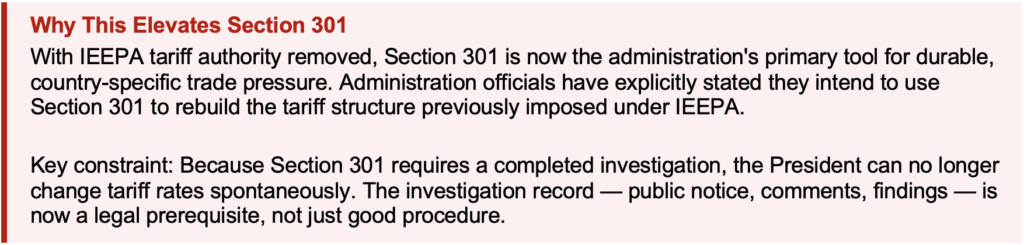

Unlike broad tariff authorities such as IEEPA or Section 232, Section 301 is a retaliatory mechanism tied to a specific, documented grievance. This distinction matters enormously in 2026: following the Supreme Court’s February ruling that IEEPA does not authorize tariff imposition, Section 301 has emerged as the administration’s primary durable tool for country-specific trade action.

2. What is the step-by-step process for imposing Section 301 tariffs?

- Initiation – Triggered by an industry petition or directly by the U.S. government

- Investigation – Conducted by USTR with public comment periods and hearings (typically 6–12 months; can be accelerated)

- Determination – USTR determines whether practices are unfair or violate agreements

- Negotiation – The U.S. attempts to resolve the issue diplomatically before imposing tariffs

- Retaliation – If unresolved, USTR may impose tariffs, restrict imports, or suspend trade agreement concessions

Note: The Trump administration has signaled it may pursue new Section 301 investigations on an “accelerated timeframe,” compressing the typical 6–12-month investigation period.

3. Who actually decides — USTR or the President?

Formally, statutory authority sits with USTR. In practice, the President sets strategic direction while USTR executes. Ambassador Jamieson Greer was confirmed by the U.S. Senate as the 20th United States Trade Representative on February 27, 2025, and has served as the operational lead on trade investigations and bilateral negotiations. The President can direct USTR via executive orders and presidential memoranda to initiate, expand, or modify investigations.

4. Can the President set tariffs at any level he chooses?

Under Section 301 specifically: No — but executive discretion is intentionally broad. The statute requires that tariff actions be “appropriate and feasible” in addressing the identified harm. This is not a strict proportionality test; it is a flexible standard, but tariff levels must be grounded in the documented harm identified in the investigation.

This procedural and statutory foundation is what made Section 301 tariffs legally durable when the Supreme Court found IEEPA tariffs unlawful. Section 301’s investigative process, while slower, provides the clear congressional delegation that IEEPA lacked.

Part II: Current Tariff Landscape (2025–2026)

5. What are the existing Section 301 tariffs on China?

The China Section 301 tariffs originated in 2018–2019 under Trump’s first term, targeting technology transfer, intellectual property theft, and innovation-related practices. They survived intact through the Biden administration, which completed a statutory four-year review and finalized expanded rates effective September 27, 2024 (with additional increases phased in through 2025 and 2026):

- Electric vehicles: 100% (effective Sept. 27, 2024)

- Solar cells (whether or not assembled into modules): 50% (effective Sept. 27, 2024)

- Semiconductors: 50% (phased in, effective Jan. 1, 2025)

- Steel and aluminum products: 25% (effective Sept. 27, 2024)

- Lithium-ion EV batteries: 25% (effective Sept. 27, 2024)

- Syringes and needles: 100% (effective Sept. 27, 2024)

- Critical minerals, ship-to-shore cranes, medical products: 25% (various dates 2024–2026)

- General List 1–4 goods: 7.5–25% (covering hundreds of product categories)

The vast majority of Section 301 tariff exposure is tied to China — by a wide margin — reflecting the scale and scope of the original 2018–2019 investigations. These tariffs remain in place and were explicitly unaffected by the February 2026 Supreme Court ruling.

6. What happened with the IEEPA tariffs and why does it matter for Section 301?

In April 2025, the Trump administration imposed sweeping “Liberation Day” tariffs on nearly all countries under the International Emergency Economic Powers Act (IEEPA). On February 20, 2026, the Supreme Court ruled 6–3 in Learning Resources, Inc. v. Trump, 607 U.S. ___ (2026), that IEEPA does not authorize the President to impose tariffs.

Chief Justice Roberts wrote the majority opinion, joined by Justices Sotomayor, Kagan, Gorsuch, Barrett, and Jackson. The Court’s holding rests on statutory interpretation: IEEPA’s authorization for the President to “regulate… importation” does not encompass the distinct power to impose tariffs — a core congressional taxing power. The Court did not invalidate IEEPA itself; it held that IEEPA simply never granted tariff authority in the first place. This cannot be fixed legislatively without amending IEEPA.

The ruling did not affect Section 301 or Section 232 tariffs, both of which remain fully valid. The administration immediately invoked Section 122 of the Trade Act of 1974 (a temporary, 150-day authority subject to congressional extension) as a bridge while working to replace IEEPA tariffs through Section 301 and 232 investigations.

7. What is Section 122 and how is it being used?

Section 122 of the Trade Act of 1974 (19 U.S.C. §2132) authorizes the President to impose a temporary import surcharge of up to 15% ad valorem for up to 150 days to address “fundamental international payments problems” — specifically, large and serious balance-of-payments deficits, imminent dollar depreciation, or international payments disequilibrium.

Immediately after the Supreme Court’s February 20, 2026 ruling, President Trump invoked Section 122 to impose a 10% global surcharge, effective February 24, 2026. This marked the first-ever use of Section 122. The surcharge expires July 24, 2026 unless Congress passes legislation explicitly extending it — the statute’s default is expiration, not continuation.

Important caveats: Multiple legal experts and economists have challenged whether current U.S. conditions actually satisfy Section 122’s statutory trigger (“large and serious” balance-of-payments deficit). Under a floating exchange rate regime, the conditions Section 122 was designed for — a fixed-rate currency crisis — do not readily apply. Twenty-four states filed suit in March 2026 challenging the Section 122 tariffs on these grounds. This legal uncertainty distinguishes Section 122 from Section 301.

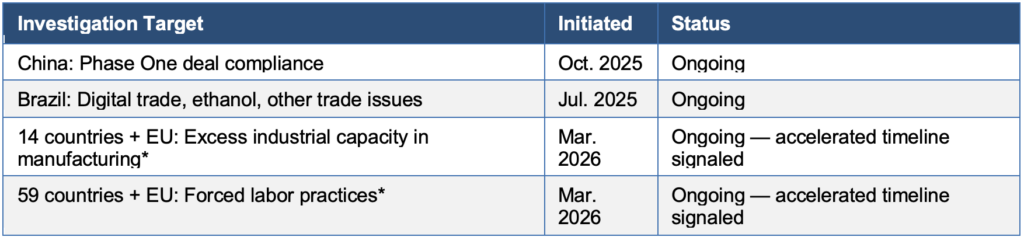

8. What new Section 301 investigations has the Trump administration initiated (2025–2026)?

As of May 2026, the following active Section 301 investigations have been initiated under the second Trump administration:

* These investigations were announced by USTR on March 11–12, 2026, directly following the Supreme Court’s IEEPA ruling, as part of the administration’s plan to rebuild tariff authority through Section 301.

9. What is the China semiconductor Section 301 action?

A Biden-era investigation into China’s semiconductor industry targeting practices concluded in late 2025 and was found to be actionable under Section 301. In December 2025, Section 301 duties on advanced semiconductors and derivatives were referenced in Federal Register notices. The Trump administration separately used Section 232 to impose a 25% duty on advanced computing chips, while indicating broader semiconductor-related tariffs may follow contingent on negotiations.

10. What is the China maritime/shipbuilding Section 301 action?

An investigation into China’s dominance in maritime, logistics, and shipbuilding was initiated in April 2024 under the Biden administration and concluded with a finding of actionable practices. Proposed port fees and tariffs were suspended in 2025 as part of the U.S.-China trade truce that began in May 2025 and was extended through November 2026.

11. What is the status of U.S.-China trade relations and how does it affect Section 301?

The U.S. and China reached a temporary tariff truce in May 2025, extended following a meeting between President Trump and President Xi Jinping in November 2025. Key current outcomes:

- The U.S.-China tariff reduction extended through November 10, 2026

- USTR extended 178 Section 301 exclusions for China goods through November 10, 2026

- The Phase One deal compliance investigation remains active — future Section 301 action is possible if China is found non-compliant

- Proposed port fees and shipping tariffs tied to the maritime investigation remain suspended

Business implication: The truce is bilateral and temporary. Section 301 tariffs on China represent the floor — not the ceiling — of potential trade pressure. A new excess capacity investigation targeting China specifically was initiated in March 2026.

Part III: Duration, Review, and Modification

12. Do Section 301 tariffs automatically expire?

No. There is no fixed legal expiration date. Tariffs remain in effect indefinitely unless affirmatively removed by the President or USTR. The China tariffs from 2018–2019 have now persisted through the Biden administration and into Trump’s second term — over seven years and counting.

13. Is there any required review mechanism?

Yes. The Trade Act requires a mandatory four-year review evaluating whether tariffs remain necessary. In practice, continuation is the near-universal outcome because:

- Domestic industries almost universally petition for continuation

- Removing tariffs requires a policy reversal — politically costly for any administration

- USTR has authority to modify rates up or down based on the review

The Biden administration completed the first statutory review in 2024, maintaining all tariffs and expanding rates on approximately $18 billion in Chinese goods across strategic sectors.

14. Can tariffs be removed before a scheduled review?

Yes. The President can modify or remove Section 301 tariffs at any time by executive action. Tariffs can also be modified through:

- Bilateral trade agreements or framework agreements

- Negotiated commitments by the targeted country (e.g., Phase One deal)

- Product-specific exclusions granted by USTR

- Strategic repositioning or deal-making (as seen with China truce, May 2025)

15. How do tariff exclusions work under Section 301?

Section 301 does not specify a formal exclusion process. Exclusions are purely an administrative discretion exercised by USTR — they are not a legally guaranteed right. USTR created an exclusion process in 2018 in response to industry concerns about unintended supply chain impacts. Key current status:

- 178 exclusions related to China technology transfer tariffs extended through November 10, 2026

- It is unclear whether USTR will establish a new exclusion process for current or future tariff actions

- Companies should not assume exclusions will be available or renewed — there is no legal requirement for USTR to offer them

Part IV: Potential Future Actions

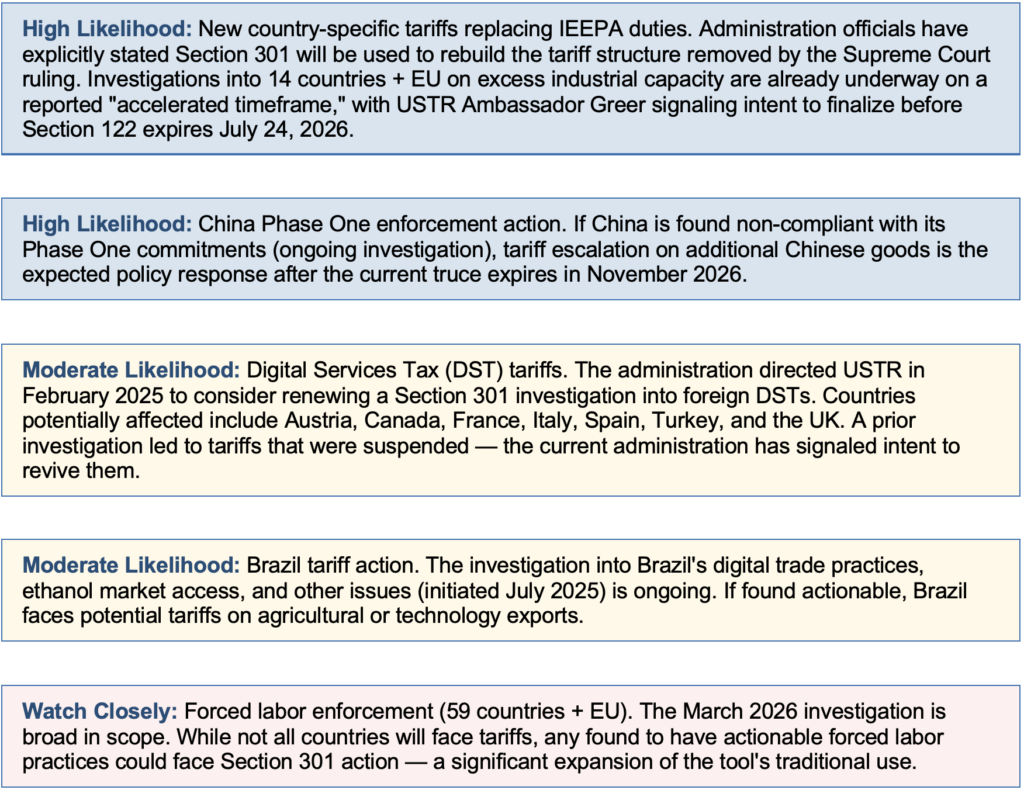

16. What Section 301 actions are most likely in 2026 and beyond?

Based on active investigations, public statements by USTR, and policy signals, the following scenarios carry meaningful likelihood. These are analytical assessments — not certainties.

17. Could Congress constrain or expand Section 301 authority?

Legislation has been introduced in the 119th Congress to increase congressional oversight of presidential tariff authority, including the Trade Review Act of 2025 (H.R. 2665/S. 1272), which would require congressional notification and review before tariffs take effect. Major legislative reform faces significant political and procedural hurdles. More likely near-term developments:

- Debate over whether to codify or limit tariff authority following the Supreme Court’s statutory interpretation ruling on IEEPA

- Potential for Congress to extend Section 122 authority beyond July 24, 2026 — the statute requires an affirmative Act of Congress to extend; inaction means the surcharge expires automatically

- Oversight hearings on USTR’s accelerated investigation timeline and the scope of the 59-country forced labor investigation

Part V: Strategic Context for Business Leaders

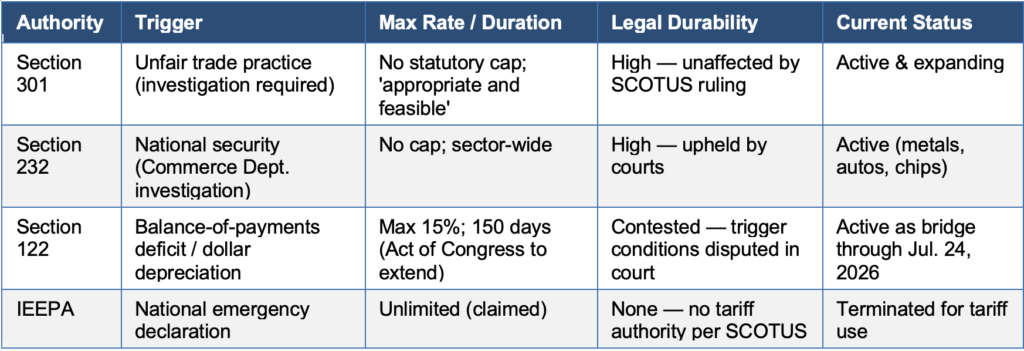

18. How does Section 301 compare to other tariff authorities?

19. What changed in 2025–2026 that business leaders must understand?

Three structural shifts define the current trade environment:

- Executive tariff power was narrowed by the Supreme Court. IEEPA’s tariff authority is gone — a ruling of statutory interpretation that cannot be reversed without amending IEEPA. Future tariff escalation must run through the statutory processes of Section 301, 232, or 122.

- Section 301 is now the primary workhorse. With IEEPA off the table, Section 301 is the administration’s most precise, legally defensible, and strategically flexible instrument for country-specific tariffs. The pipeline of new investigations — four initiated since the ruling — confirms this shift.

- Speed is accelerating. USTR has signaled an “accelerated timeframe” for completing new investigations, aiming to finalize Section 301 tariffs before Section 122 expires on July 24, 2026. New tariff exposure can materialize faster than in prior cycles.

20. What should business leaders do now?

Section 301 tariffs are durable, structural policy tools — not temporary measures. Recommended actions:

- Map supply chain exposure to active investigations — particularly China Phase One compliance, Brazil, and the 14-country excess capacity probe (public comment closed April 15, 2026)

- Monitor July 24, 2026 closely — Section 122 expires unless Congress acts; the administration’s stated intent is to replace it with Section 301 tariffs, which would be permanent rather than temporary

- Assess DST investigation exposure if your business operates in Austria, Canada, France, Italy, Spain, Turkey, or the UK

- Evaluate tariff engineering options (country of origin shifts, product classification reviews, bonded warehouse strategies) before new tariffs take effect

- Do not assume exclusions will be available — USTR has made no commitment to a new exclusion process, and exclusions are discretionary, not legally guaranteed

- Build tariff scenario planning into capital allocation, pricing, and contract structures — effective rates on Chinese strategic goods could return to 45–55% under Section 301 authority once investigations conclude

This document is for informational purposes only and does not constitute legal advice. Consult qualified trade counsel for guidance specific to your business. Current as of May 2026.