Humanoids, agentic AI, and autonomous manufacturing aren’t trends — they’re the new weapons of industrial competition.

Manufacturing is going through a major shift. The manufacturing sector will need 3.8 million new employees between 2024 and 2033, but 1.9 million jobs are at risk of remaining unfilled: a 50% fulfilment gap. In part, this gap is due to an aging workforce, as well as evolving skill requirements and reduced interest in production jobs. The Baby Boomer generation is rapidly reaching retirement age, taking decades of specialized knowledge with them. It’s expected that 25.3 million will retire by 2035.

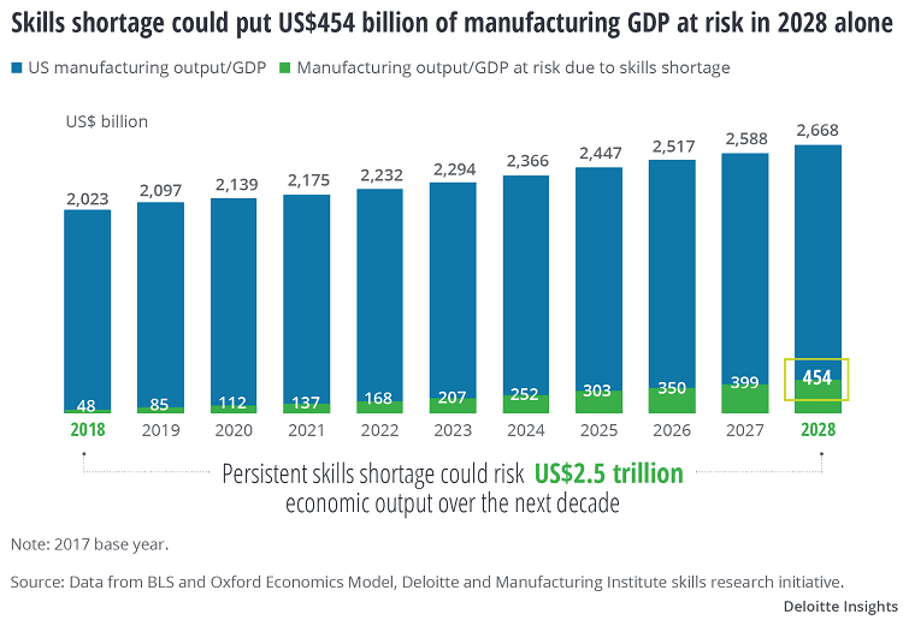

One prediction from Deloitte suggests that “if the manufacturing industry is unable to fill anticipated jobs by 2028, the annual loss of manufacturing GDP can reach $454 billion.” These potential losses are seen as increasingly unacceptable in the current geopolitical climate. You can see these GDP risks from skill shortages highlighted in Figure 1 below:

Figure 1: OroCommerce. Skills shortage could put US$454 billion of manufacturing GDP at risk in 2028 alone.

This workforce crisis coincides with intensifying global economic and strategic competition, as well as supply chain disruptions that require a significant transformation in manufacturing operations. Executive orders and actions from the Trump administration illustrate the importance of manufacturing industry decisions and developments, and this sector is poised to play a key role in US global industrial competitiveness over the next years and decades.

A new wave of advanced manufacturing processes, making use of both robotics and AI technologies, promises to provide part of the solution, and support the US drive for economic dominance. In 2024, 63% of manufacturing companies already report using AI for quality control. Other AI and robotics applications also already include predictive maintenance and real-time process optimization.

Approaches such as Robots as a Service (RaaS) and agentic AI are also significantly transforming the industry by accelerating manufacturing processes, expanding access to cutting-edge robotic and AI tools, and reducing the need for human involvement. Through subscription-based models, RaaS allows smaller manufacturers to leverage sophisticated robotics without the burden of large upfront investments. Meanwhile, agentic AI systems operate autonomously within defined parameters, making real-time adjustments to production conditions with minimal human intervention.

The global industrial AI market reached $43.6 billion in 2024 and is expected to grow at a CAGR of 23% to $153.9 billion by 2030. This level of growth signals a fundamental shift in how products will be designed, manufactured, and delivered, with plenty of hope in these technologies.

As noted, US policy approaches are also reflecting an increasing desire for global economic domination in this area, with laws like the Infrastructure Investment and Jobs Act (IIJA), the Inflation Reduction Act (IRA), and the CHIPS and Science Act (CHIPS) already providing significant federal investment in different sectors. This support established from the previous administration lays a solid foundation for advanced manufacturing to develop.

Alongside these pieces of legislation from the Biden administration, Trump administration actions such as the Executive Orders “Immediate Measures to Increase American Mineral Production” and “Unleashing Prosperity Through Deregulation” aim to reduce regulatory red-tape, expand the industrial base, and channel financing (both private and government) towards local, US-based supply chains. Other executive orders and the One Big Beautiful Bill Act (OBBB) provide major tax cuts, infrastructure investment, regulatory softening, and a drive for industrial competitiveness. These actions illustrate a shift away from climate or global cooperation, and towards industry and global competition.

This report looks at the following aspects of this transformation:

- Evolution of Robotics and AI in Manufacturing: A brief history of industrial robots, collaborative robots, humanoid platforms, and the shift toward mass customization.

- Core Applications of AI in Manufacturing: The way AI and robotics are shifting production optimization, quality inspection, and intelligent supply chain management.

- Robotics in Advanced Manufacturing: Traditional industrial robotics, collaborative robots, humanoid robotics in factories, AMRs and AGVs, plus wearable robotics and augmentation.

- Emerging Technologies Transforming Manufacturing: Digital threads and twins, generative AI for design, edge AI, as well as 3D printing with AI.

- Key Challenges and Barriers: High capital expense, workforce shortages, cybersecurity vulnerabilities, interoperability issues, and labor concerns.

- Economic & Workforce Implications: The industry transformation’s impact on labor markets, the need for reskilling, productivity effects, and role in reshoring strategies.

- Investment Landscape & Startup Ecosystem: VC trends, notable players, and strategic investments by industrial giants.

- Sector Deployment Case Studies: Aerospace, automotive, electronics, medical devices, consumer goods, and heavy industry applications.

- Policy, Trade & Regulatory Landscape: US CHIPS/IRA/IIJA incentives, NIST guidance, OSHA frameworks, Trump administration executive orders and the OBBB, as well as increasing international competition.

- Growth Areas: Autonomous lights-out manufacturing, AI-designed factories, humanoid workforce expansion, and green manufacturing.

- Strategy: What approaches different stakeholder groups can take to make the most of this transformation.

- Conclusion: Why AI and robotics adoption equals competitive survival.

The manufacturers and countries that integrate these technologies will secure decisive cost, quality, and flexibility advantages, as well as more robust supply chains and greater competitiveness. Those who delay will lose out as automated competitors capture market share and global influence through superior operational and economic performance.

Evolution of Robotics and AI in Manufacturing

The journey from Henry Ford’s assembly line to today’s intelligent factories is one of many years of incremental innovation, followed by a sudden decade of radical transformation. Traditional industrial robots, confined to limited areas of movement and programmed for single tasks, are now giving way to flexible systems that can adapt, learn, and collaborate with human workers in real time.

The shift toward humanoid robotics and the use of AI is manufacturing’s next evolutionary leap. For example, one of the industry leaders, Tesla, aims to produce several thousand Optimus humanoid robots in 2025 alone, with aspirations for exponential growth to follow. These humanoids will initially handle repetitive tasks at Tesla factories, such as loading sheet metal on welding lines.

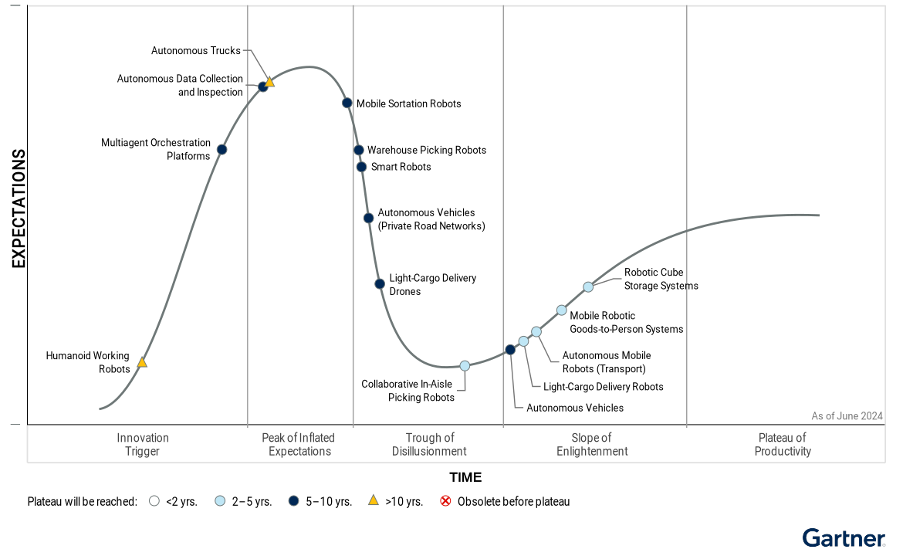

However, not all technologies mature and achieve the promise that industry members and investors hope for. The gap between technological demonstration and scaled industrial deployment often spans years, with many promising prototypes failing to survive the transition from controlled environments to demanding production floors. In Figure 2 below, you can see Gartner’s hype cycle for mobile robots and drones, showing the progress from innovation to mainstream adoption, as well as some of the technologies that have had inflated expectations, and the timelines for realisation.

Figure 2: Gartner. Hype Cycle for Mobile Robots and Drones, 2024

For instance, robots continue to face what is known as the “hands problem”, an issue with robotic hands being unable to completely match the dexterity and ability of human hands. Another example of this mismatch between hopes and reality is the example of Figure’s collaboration at BMW plants. Figure is a California-based company developing autonomous humanoid robots, and it announced last year that it had signed a commercial agreement with BMW to deploy general purpose robots in automotive manufacturing environments. Figure’s humanoid robots assist with the automation of difficult, unsafe, and tedious tasks throughout the manufacturing process.

As in Gartner’s image, some of the excitement around these robots turned out to be over-inflated, indicating the development that is still to come: by March 2025, only a single Figure 02 robot was operating at the plant, performing a repetitive task in the body shop during production hours. The robot retrieves metal sheet parts from a logistics container and places them onto a fixture for welding by other automated systems. You can see an image of the Figure 02 robot in Figure 3 below:

Figure 3. BMW Group. Humanoid Figure 02 robots tested at BMW Group Plant Spartanburg

The integration of AI with Industrial Internet of Things (IIoT) sensors is another step in the evolution of manufacturing robots, as it creates cyber-physical systems that monitor, analyze, and optimize production in real time. These systems can process data from thousands of sensors simultaneously, identifying patterns and anomalies that would be impossible for human operators to detect. Digital twins (virtual replicas of physical production systems) allow manufacturers to simulate changes before implementation.

A continuing shift from mass production to mass customization is also fundamentally changing manufacturing economics, as this customization requires high-mix, low-volume capabilities that serve niche markets profitably while maintaining efficiency. Where traditional assembly lines might produce millions of identical units, modern flexible manufacturing systems can economically produce batches as small as one unit, enabling personalized products at near-mass-production prices. AI systems that can change models and production lines quickly can allow this mass customization to occur more quickly.

Core Applications of AI in Manufacturing

Humanoids, AI systems, and machine learning algorithms are being applied in several core manufacturing applications. In many ways, they are transforming production floors into self-optimizing systems. This has a major effect on business outcomes: according to IBM’s 2024 Industrial report, enterprises that use predictive AI in manufacturing quality management see a significant improvement (up to 4x) in process capability compared to those using traditional statistical process control models.

When equipment breaks and work stops, costs to a business (per hour) can range from $36,000 (e.g. in consumer goods) to $2.3 million (e.g. in the automotive sector) according to a 2024 report from Siemens. These figures account for not only lost production but also cascading effects on supply chains, labor idling, and contractual penalties for delayed deliveries. Predictive maintenance is one way that shut-downs can be prevented, as maintenance can take place on schedules that are less disruptive, and keep equipment working for longer periods of time. The economic reality of potentially large losses is part of why urgent adoption of AI-powered predictive monitoring systems is taking place, as they can help to mitigate these costs.

The global predictive maintenance market size has already reached USD 12.7 billion in 2024, and is projected to grow at a CAGR of 22.8% reaching USD 80.6 billion in 2033. One example of a large business already seeing results is Bosch. They implemented a comprehensive predictive maintenance strategy that utilized IoT devices to monitor manufacturing equipment. The system analyzes vibration patterns, temperature fluctuations, and acoustic signatures to identify potential failures weeks before they occur. This AI-driven predictive maintenance system led to a 25% reduction in equipment downtime and a 15% decrease in maintenance costs for the business.

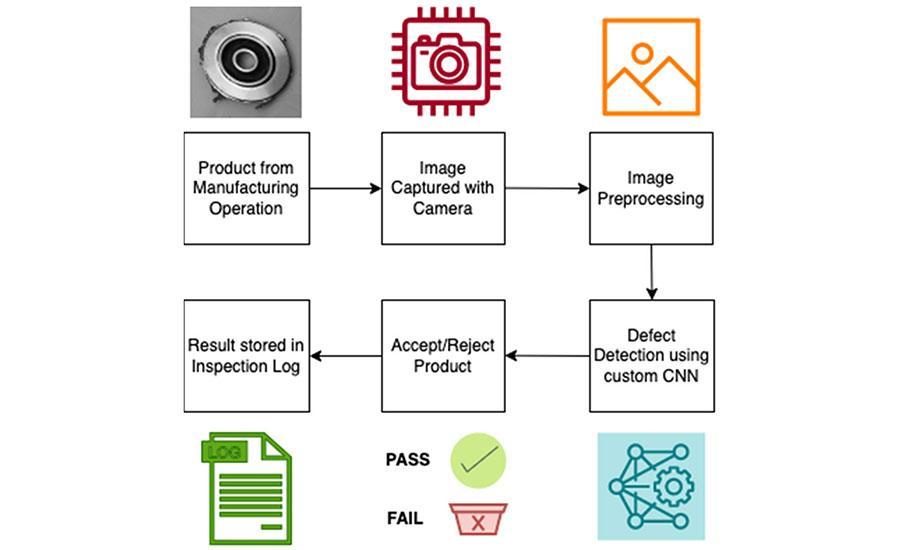

In addition, computer vision powered by deep learning has also revolutionized quality control. As a result of issues like worker fatigue, shift changeovers, and simple errors, human inspectors are prone to variability in their defect detection rates, which can range between 60 and 90 percent. In contrast, AI-based quality control systems make fewer mistakes, and can work around the clock without slowdowns in speed or changes to accuracy. In Figure 4 below, you can see a diagram of how the AI quality-control inspection process works.

Figure 4. Assembly Mag. AI-based inspection is a six-step process.

In one early case study, BMW implemented comprehensive AI vision systems across their production facilities, with an immediate impact. At one of their European plants, BMW was able to reduce defect rates by 30% within a year of implementation. In addition, at one of their South Carolina plants, BMW also saw significant efficiency improvements. “We’re achieving five times of what we thought was even possible before, with what the AI is achieving now,” said BMW Group Manager Curtis Tingle. This transformation was carried out by using a combination of welding robots, as well as AI quality checks, and real-time correction. The system detects welding imperfections immediately and adjusts parameters on subsequent welds, creating a continuous improvement loop.

Samsung also reduced customer return rates by 31% within 18 months of implementing an AI-based quality control approach to semiconductor manufacturing, using a “multi-stage machine learning system that analyzes both visual data and electronic test parameters to identify potential defects in microchip production.” Given that semiconductor defects can be microscopic and occur at various production stages, this multi-layered approach catches issues that single-method inspection would miss. In general, studies show that AI-driven quality control can reduce false rejections by up to 30%, which helps manufacturers to increase output without sacrificing quality. False rejections occur when perfectly functional products are discarded, resulting in wasted materials and production capacity.

AI can also play a big role in improving supply chain orchestration through predictive analytics and real-time optimization. According to AllaboutAI, “Currently, 41% of manufacturers use AI-based applications to gather and manage supply chain data.” Forbes also notes that companies can “use AI to analyze vast amounts of data from suppliers, weather patterns, and market trends to enhance supply chain efficiency … [they are] able to more effectively predict demand and optimize inventory levels, improve overall logistics as well”. The improvement of these supply chains and the desire for localization from the current Trump administration is likely to fuel investment in these areas. Resilient supply chains that function more efficiently can help to support US political goals both locally and on the global stage.

These AI systems analyze thousands of variables, including supplier performance, transportation networks, inventory levels, and demand patterns, to optimize procurement and distribution. This holistic analysis enables manufacturers to anticipate disruptions and reroute shipments or adjust production schedules proactively rather than reactively. One example of improved supply chain management is that in July 2025, Amazon passed the milestone of deploying 1 million robots and is now making use of a generative AI foundation model that can improve robot fleet travel efficiency by 10%. This model is called “DeepFleet”, and is intended to “coordinate the movement of robots across [Amazon’s] fulfillment network.”

Robotics in Advanced Manufacturing

In advanced manufacturing systems, there are also a few different types of robots that can be useful, including traditional industrial robots, collaborative robots, humanoids, mobile robotics, and wearables. Fixed automation systems continue to dominate specific manufacturing tasks. The top four industrial robot vendors (Fanuc, ABB, KUKA, Yaskawa) collectively held 57% market share in 2024. These systems excel at repetitive tasks requiring precision and speed but lack the flexibility needed for modern high-mix production environments.

Collaborative robots work alongside human operators without safety barriers, using force-limiting technology and advanced sensors. When unexpected contact occurs, these robots immediately reduce force or stop movement, preventing injuries that traditional industrial robots could cause. The collaborative robot market is projected to grow significantly from $1.42 billion in 2025 to $3.38 billion by 2030. These systems create hybrid workflows where robots handle repetitive tasks while humans focus on complex decision-making and quality control.

Humanoid robots are another major aspect of manufacturing automation. As noted above, Tesla aims to produce several thousand Optimus humanoid robots in 2025, with hopes for exponential growth to follow. At volumes exceeding 1 million units annually, Optimus’ production cost is expected to drop below $20,000 per robot, making units significantly more affordable. This price point would make humanoid robots competitive with the annual cost of human labor in many manufacturing roles. The advantage of humanoid form factors is their ability to work in facilities designed for humans without requiring infrastructure modifications or specialized workstations.

Sanctuary AI has also announced a strategic partnership with global mobility technology company Magna. The partnership aims to increase the scaling of Sanctuary AI’s robots while refining the technology for use in challenging manufacturing environments for Magna and other industrial and automotive customers. The time it takes for new tasks to be automated has gone from weeks to less than 24 hours, which is a significant improvement in task automation speed and autonomous system capability.

Another application of robotics in advanced manufacturing is the use of exoskeletons and wearable robotics. These augment human capabilities while reducing injury rates. These systems address the physical demands of manufacturing work, where workers routinely carry heavy loads over difficult terrain, leading to musculoskeletal injuries that account for significant medical costs and reduced readiness.

Like other aspects of this industry, market valuations are increasing. The Autonomous Mobile Robots For Intralogistics Application Market was valued at USD 4.8 billion in 2024 and is projected to grow to USD 18.2 billion by 2034. This is a CAGR of 14.3%. Advanced manufacturing is seeing significant growth across several fronts, with several technologies converging in ways that multiply the benefits.

Emerging Technologies Transforming Manufacturing

In addition to more established or tested tools, a few emerging technologies are transforming the manufacturing sector in several ways. First, one major interesting development is in the field of agentic AI.

Agentic AI is a type of AI that can carry out autonomous decision-making with no or minimal human intervention. The development and increasingly widespread use of agentic AI is because of a number of reasons, including the increasingly rapid development of LLMs, the improvement of advanced reasoning capacities, AI API integration, and GPU availability, which improves computational power.

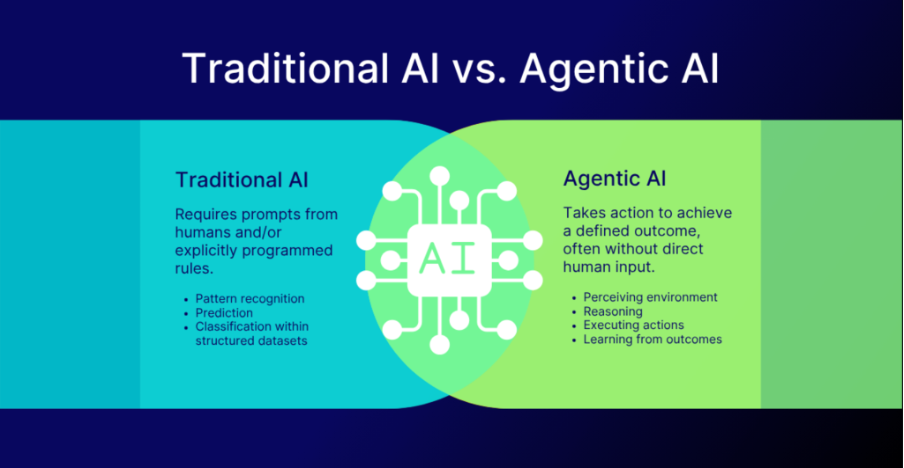

In the context of manufacturing, these platforms analyze production data, identify optimization opportunities, and implement changes in real-time. AI design systems can help engineers to generate hundreds of valid designs in seconds, and can account for factors such as manufacturability, compliance requirements, sustainability targets, and material utilization. In Figure 5 below, you can see some of the key differences between traditional and agentic AI.

Figure 5. Logicgate. Traditional AI vs Agentic AI.

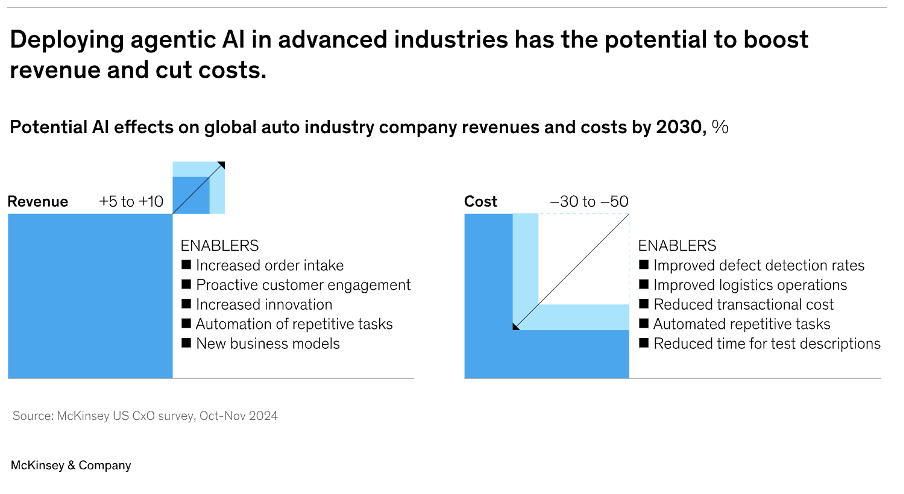

McKinsey notes that through the use of agentic AI, “logistics operations have increased in efficiency through autonomous routing and scheduling, in some cases leading to a more than 20 percent drop in inventory and logistics costs. … And transactional cycle times have been reduced from days to hours or even minutes with intelligent workflow agents, such as those used in documentation efforts.” In Figure 6 below, you can see a chart highlighting the ways in which revenue can be boosted, and costs can be cut using agentic AI:

Figure 6. McKinsey. Deploying agentic AI in advanced industries has the potential to boost revenue and cut costs.

For instance, agentic AI troubleshooting systems can repair equipment failures, recommend solutions, and even order replacement parts automatically. By accessing supplier databases to compare lead times and pricing, these systems place orders within predefined budget parameters, completing processes that previously required multiple human approvals. When integrated with Manufacturing Execution Systems (MES) and Enterprise Resource Planning (ERP) platforms, they enable end-to-end automation of production planning and execution.

Generative AI is also fundamentally reshaping the design phase. Generative design systems take specific functional and physical constraints, such as load-bearing requirements, material type, and weight limits, and use algorithms to generate thousands of optimized designs that a human engineer might never think of. These designs often use complex, organic geometries that are lighter, stronger, and use less material, leading to significant weight reductions in applications like automotive components.

This approach works well in combination with Advanced Additive Manufacturing (3D Printing). Unlike traditional subtractive methods, 3D printing can create the complex shapes generated by AI, making the combination of generative design and 3D printing a fast-moving frontier in manufacturing. AI-powered vision systems are also being integrated directly into the 3D printing process to analyze print quality layer-by-layer and adjust in real-time to prevent micro-defects.

The efficacy of generative design and AI-driven manufacturing relies heavily on data infrastructure. This infrastructure is increasingly using approaches such as digital threads and digital twins. A digital thread is a single, continuous flow of data that links every stage of a product’s lifecycle, from the initial requirements and design, through manufacturing, quality inspection, service, and disposal. It connects data silos across ERP and MES systems to make sure all stakeholders use one set of information. Digital threads can also be built using generative AI to increase data connectivity, so product manufacturers can make use of data that could help to improve their products.

Digital twins are virtual replicas of a physical object, system, or process that uses real-time data to accurately simulate their real-world counterpart’s behavior. For example, wind energy companies utilize multiple predictive maintenance techniques to maximize turbine performance by running simulations on these virtual models. When combined with generative AI, AI can generate synthetic data for testing, create new operational scenarios, and autonomously suggest optimizations.

Finally, edge AI allows manufacturers to connect intelligence directly to production equipment, so that machinery and tools can make millisecond response times without cloud connectivity. Edge-AI processors can reduce decision-making latency from seconds to milliseconds, so that autonomous mobile robots can navigate dynamic production floors without cloud dependence.

Key Challenges and Barriers

Despite several benefits, manufacturers must deal with significant implementation challenges. For example, the financial barrier remains the most immediate obstacle for most manufacturers. According to Deloitte, predictive maintenance can reduce maintenance costs by 5-10% and increase equipment uptime by 10-20%. However, hardware installations can significantly add to project costs: complex legacy system integrations add even more. This can create financial situations where upfront costs are significant, and businesses must take time before the integration of new technologies pays off.

The human factor presents an equally big challenge. In many cases, human workers need to reskill and adapt. McKinsey explains that “in terms of magnitude, it’s akin to coping with the large-scale shift from agricultural work to manufacturing that occurred in the early 20th century in North America and Europe, and more recently in China.” Significant skills gaps require retraining and reskilling, which takes time and can be costly.

One of the major factors considered by businesses in the 2025 Smart Manufacturing and Operations Survey is operational risk from failed initiatives. You can see these risks in Figure 7 below:

Figure 7. Deloitte. The potential risk of business disruption in complex transformations

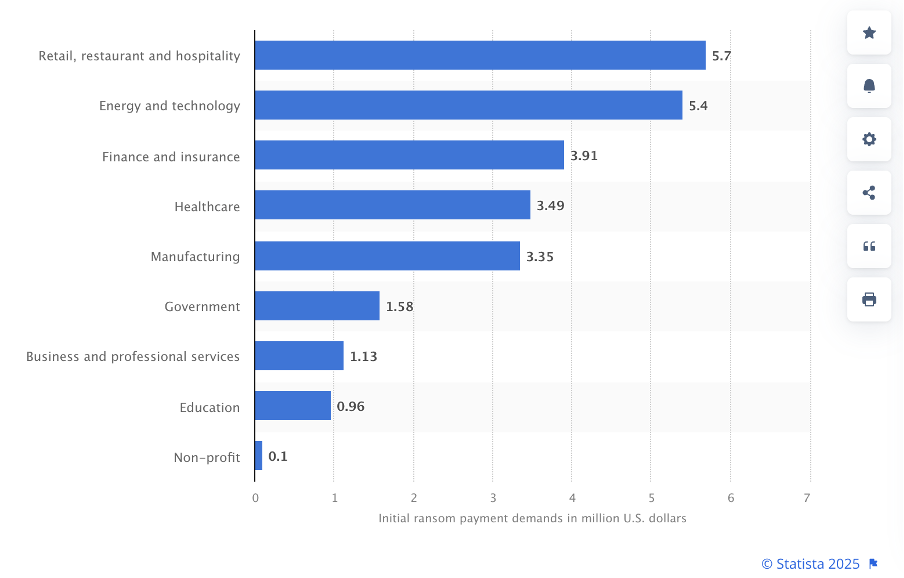

The use of IT and AI systems in various industries also creates new security risks. For the fourth consecutive year, manufacturing was the most attacked industry, with 24% of all cyberattacks in 2024. Manufacturers present attractive targets because production disruptions create immediate financial pressure, making companies more likely to pay ransoms quickly. In many of these cases, data theft occurs, but ransomware attacks can also stop production and become very costly. As you can see in Figure 8 below, Statista estimates that ransomware payments for the US in 2023 were upwards of 3.3 million dollars. This amount is only likely to increase as attackers become more sophisticated and gain access to further attack surface as businesses integrate more AI and IT systems.

Figure 8. Statista. Average initial ransom payment demands from organizations in the United States in 2023, by industry (in million U.S. dollars)

In addition, most manufacturing facilities operate a patchwork of equipment spanning decades, creating major integration challenges. Modern AI and robotics systems must communicate with programmable logic controllers (PLCs), MES and ERP platforms that were never designed for such integration. Custom interfaces and middleware solutions increase both complexity and cost.

Manufacturers in regulated industries face additional hurdles. Medical device manufacturers must check that AI systems meet FDA requirements for quality and traceability. Automotive suppliers must demonstrate compliance with ISO/TS 16949 standards. Food processing facilities must satisfy FDA and USDA requirements. These validations add time and cost to the process of integrating AI systems, and the evolving nature of AI regulations creates additional uncertainty. This leaves manufacturers with issues when they want to make long-term automation investments, as there’s a risk that future regulations may require costly retrofits or modifications.

The European Union’s AI Act, which began phased implementation in 2024, exemplifies this regulatory uncertainty by classifying certain manufacturing AI systems as “high-risk” and requiring extensive compliance documentation.

Nonetheless, in the current regulatory climate established by the Trump administration, manufacturers and companies in the US may face lower regulatory hurdles than before. While this creates additional uncertainty, it’s likely that investment and development in the manufacturing sector will benefit from this regulatory softening.

Economic & Workforce Implications

Amidst these technological changes, the manufacturing workforce is also going through a transformation . One issue is that AI and robotics are simultaneously driving productivity gains and transforming labor demand. The most immediate workforce effects are two-fold: demand is rising for technicians, robotics engineers, and data-literate operators, while routine machine-operation and repetitive assembly roles are in decline.

An OECD analysis from 2024 shows how AI exposure is changing skill mixes and estimates that a substantial share of tasks in manufacturing is susceptible to automation, and notes that AI adoption simultaneously creates new hybrid roles (robot maintenance, systems integration, AI-assisted quality control) that require different skills and training.

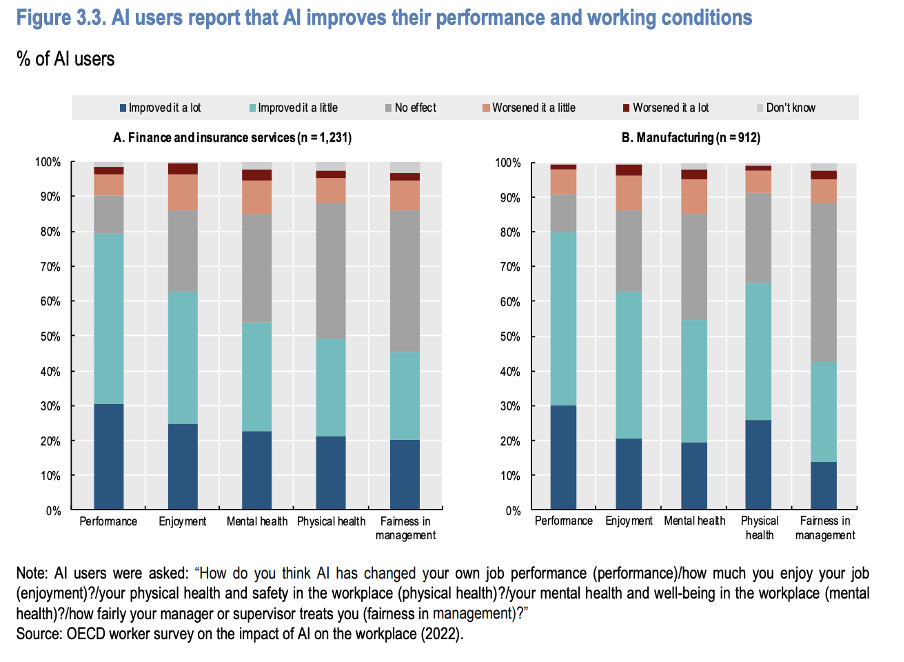

Despite the possible job changes or shifts in roles, another OECD report from 2022 found that most AI users in both finance and manufacturing industries had improved their performance, enjoyment, and mental health at work as a result of AI, as you can see in Figure 9 below:

Figure 9. OECD. AI users report that AI improves their performance and working conditions

Overall, automation’s net effect is likely to be a small amount of employment growth paired with significant occupational turnover in terms of employees. Deloitte’s manufacturing surveys and industry outlook report both highlight that firms often reinvest productivity gains into R&D and new product lines, which can create additional jobs in other areas, such as design, software, and advanced materials.

Other than reskilling and workforce development, AI and robotics adoption in the manufacturing sector is also shifting reshoring strategies, as manufacturers bring production back to domestic facilities. President Trump’s tariff policies, such as reciprocal tariffs and a baseline 10% levy on imports, have been explicitly designed to incentivize reshoring by making domestic manufacturing more cost-competitive. While this aims to revive American manufacturing, experts note that successful reshoring will take years and likely favor high-value, automated production over labor-intensive manufacturing. For manufacturers pursuing reshoring, advanced automation technologies help offset traditional cost disadvantages, which offer a pathway to supply chain resilience and reduced lead times.

Additional Trump administration executive orders, and the OBBB, as discussed in the policy section below, also highlight movements towards local manufacturing and the hope of additional reshoring.

Investment Landscape & Startup Ecosystem

The global market for artificial-intelligence-enabled robotics is projected to grow significantly, as noted above. This dramatic growth reflects rising demand in manufacturing and logistics as companies seek automation solutions to address labor shortfalls, customization pressures, and efficiency goals.

As a result, venture capital and strategic investment are flowing heavily into robotics startups. For example, Figure AI, a California-based humanoid-robotics firm, has reportedly raised in excess of USD 700 million since 2022, backed by high-profile investors including Microsoft, Nvidia, Intel Capital and Jeff Bezos’ investment arm. Figure AI is reportedly seeking an additional USD 1.5 billion at a valuation of around USD 39-40 billion.

In 2024, robotics startups raised approximately $7.5 billion, higher than 2023’s $6.9 billion, though funding became increasingly concentrated, with only 473 funding rounds compared to 671 the previous year. More broadly, AI and machine learning startups attracted $192.7 billion in the first three quarters of 2025, with manufacturing companies raising $42.6 billion across various deals. The concentration of capital into fewer, larger deals means that growth-stage companies face longer fundraising timelines and increased scrutiny from VCs wary of robotics’ inherently capital-intensive nature and extended development cycles.

Investments into the manufacturing industry from big companies like TSMC, Samsung, and ASML are also producing significant reshoring and investment into the US, particularly in relation to semiconductors. For example, “from October 2024 to April 2025, semiconductor projects represented only about 5% of all announcements. However, they accounted for a staggering $102.6 billion in capital investment.” The global chip shortage, the CHIPS Act, and the Trump administration’s invocation of Defense Production Act authority (which allows the government to prioritize and allocate resources for national defense) for strategic minerals are big drivers behind this trend, channeling both private and federal capital toward domestic semiconductor capacity. The US government’s emphasis on localization and American manufacturing will likely increasingly fuel reshoring and US investment in AI and robotics manufacturing companies.

In parallel, business models are evolving. As an example, Robotics-as-a-Service (RaaS) is increasing used to shift robotics adoption from large-capital expenditure to subscription/operational cost models. According to Global Market Insights, the RaaS market is projected to expand at a CAGR of around 18%, as you can see in Figure 10 below:

Figure 10. Global Market Insights. Robotics as a Service (RaaS) Market

The RaaS model lowers entry barriers for mid-sized manufacturing firms and accelerates automation rollout.

Leading firms currently include Geek+, Amazon Robotics, Fetch Robotics (acquired by Zebra Technologies), GreyOrange and Locus Robotics. These companies are focused not only on robotics hardware, but also on integrated software, fleet orchestration and scalable deployment models. Taken together, the investment landscape suggests not just hardware build-out, but an emerging services infrastructure, ecosystem platforms and software stacks tailored for modern manufacturing.

For manufacturers and investors alike, the implication is clear: the automation frontier is no longer distant or niche; it’s becoming mainstream.

Sector Deployment Case Studies

Some sectors, such as aerospace, automobiles (as already mentioned in examples from BMW), electronics, medical devices, and consumer goods and packaging, already show key case studies. In the aerospace industry, automation and AI-driven robotic systems are being used to achieve ultra‐high precision in the assembly of critical components. Aerospace manufacturing demands tolerances measured in microns, as even minor deviations can compromise structural integrity or aerodynamic performance at high altitudes. For example, Canadian startup company Xaba Inc. has been working with Lockheed Martin Corp, using advanced robotics to assemble military planes. These systems handle tasks like drilling thousands of precisely positioned holes in aircraft fuselages and wings, work that previously required highly skilled technicians and consumed weeks of labor.

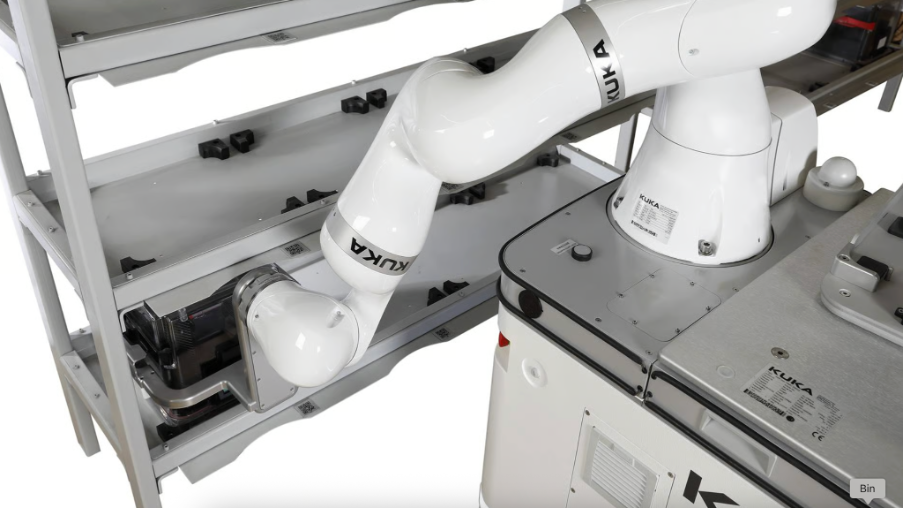

In the electronics and semiconductor fabrication sectors, manufacturing systems require clean-room compatible robotics with sub-millimeter precision and extreme process control. For instance, a case study by KUKA highlights how they are using a “cleanroom” automated guided vehicle (AGV) robot for wafer transport and handling in semiconductor plants, including mobile platforms designed for ultra-clean environments. You can see an image of the KUKA robot below in Figure 11:

Figure 11. KUKA. Robot for handling “wafers” in semiconductor production

Medical device production is another particularly difficult area, as it has strict regulatory requirements (e.g., from the Food and Drug Administration in the US). An article from Universal Robots describes how collaborative robots are being used across medical-device manufacturing for high precision, consistent quality, and meeting regulatory demands. Automation providers also emphasise that factory automation supports medical-device producers in achieving traceability and regulatory compliance.

Fast-moving consumer goods and packaging lines also increasingly deploy high-speed pick-and‐place robots and flexible automation to handle high mix, low volume, and rapid changeovers. For example, a case study of a confectionery packer shows how pick-and-place robots improved output by nearly 30 % in a flexible packaging line. In Figure 12 below, you can see an image of the fully automated “Mozart” chocolate packaging robot line:

Figure 12: Schubert. Packaging of the Mozart-Kugeln

More broadly, robotics in packaging is recognised as a growing trend: robotics systems (including delta robots, SCARA (Selective Compliance Assembly Robot Arm), and collaborative arms) are being adopted to boost throughput, quality and flexibility in packaging operations.

Policy, Trade & Regulatory Landscape

The transformation of manufacturing through AI and robotics is not purely a technological shift. Rather, it is increasingly shaped by policy, trade and regulation. In the US, some federal initiatives passed by the previous administration was explicitly designed to accelerate automation and advanced manufacturing. In addition, a few executive orders and other acts from the Trump administration have further deepened support for manufacturing, while removing regulatory hurdles and reducing the focus on climate and other secondary issues.

For example, the CHIPS and Science Act (2022) provides funding for domestic chip fabrication and advanced manufacturing capability, including grants, tax-credits and programmes targeting automation and advanced production.

Meanwhile, the Infrastructure Investment and Jobs Act and the Inflation Reduction Act funnel funding toward smart-manufacturing, clean-energy production and advanced materials. These are areas where robotics, IIoT sensors and AI are key enablers.

Executive orders, alongside the One Big Beautiful Bill Act (OBBB), have further emphasized the importance of manufacturing and the industrial base to exert global strategic dominance and achieve political goals. The Critical Minerals Executive Order notes explicitly that the US “possesses vast mineral resources that can create jobs, fuel prosperity, and significantly reduce our reliance on foreign nations.” The Order elaborates that “reliance upon hostile foreign powers’ mineral production” is a threat to US national and economic security. As a result, the intention of the order is to facilitate domestic mineral production and reduce regulatory barriers in industry and manufacturing that relate to these processes.

Another Executive Order from January 31, 2025 titled Unleashing Prosperity Through Deregulation, highlights further the shift taking place. This Executive Order would require, for example, for every new regulation proposed by a government department, 10 should be identified to be repealed. This Executive Order and other such deregulation steps will have a large impact on the US manufacturing and industrial sectors and shifts the focus from global issues such as climate change to domestic competitive cost structures and US economic benefit.

In relation to AI in the sector in particular, a further Executive Order titled Removing Barriers to American Leadership in Artificial Intelligence, explicitly revokes “existing AI policies and directives that act as barriers to American AI innovation”, and emphasizes that the intention is to “clear a path” for the US to “act decisively to retain global leadership in artificial intelligence.”

The OBBB also combines large tax cuts with investments in infrastructure, oil and gas, energy independence, and further reduces regulatory burdens. This is another fiscal vehicle for the current administration to increase investment in the manufacturing and other industrial sectors, with the aim of re-establishing and maintaining global dominance. The development of AI and robotics-based processes and technologies in the sector will also benefit from this legislation, particularly for companies based in the US and using US-sourced materials.

As the complexity of integrated cyber-physical systems grows, government agencies like the National Institute of Standards and Technology (NIST) and the Occupational Safety and Health Administration (OSHA) are also developing frameworks to guide safe and reliable deployment. For example, OSHA is adapting its workplace safety regulations to address the unique risks posed by robotics, especially the rise of collaborative robots and human-robot teams. In addition, NIST is providing protocols to secure the highly connected environments that integrate AI and robotics (one of the main challenges noted above). The administration’s deregulation agenda creates a tension between accelerating deployment and maintaining safety oversight. This is a balance that will define the practical implementation of these frameworks and may need additional adjustments in the future as the technology develops.

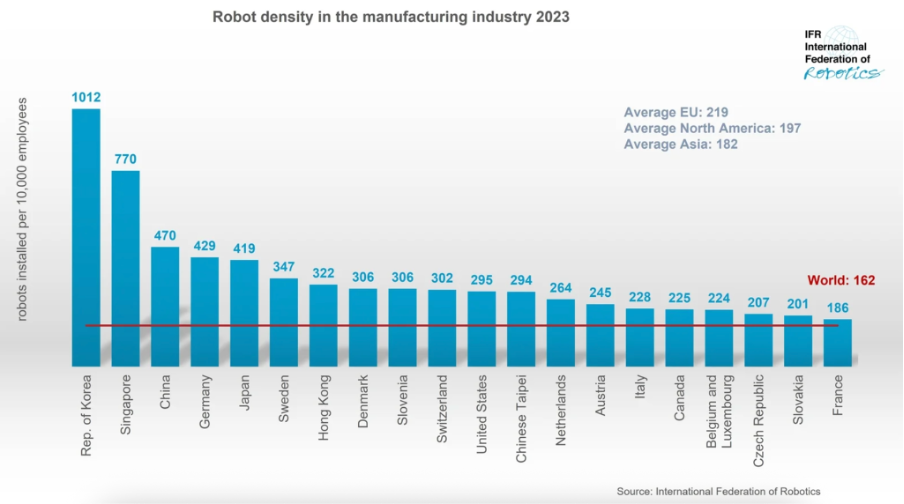

On the international front, global competition in manufacturing automation is accelerating, and the US policy landscape reflects this increasing race for domination Other countries, particularly in Asia, have a significant lead when it comes to robot density; this is a trend that the current US administration would like to shift. The International Federation of Robotics (IFR) reports that global robot density in factories has more than doubled in recent years, reaching an average of 162 robots per 10,000 employees in 2023. In Figure 13 below, you can see an image from the IFR showing robot density in the manufacturing industry across several countries:

Figure 13. International Federation of Robotics. Manufacturing robots per 10,000 employees, listed in order by country.

In countries like China (470 robots per 10,000 in 2023), automation is rapidly scaling, and making use of state-backed strategies to capture manufacturing competitiveness. China’s “Made in China 2025” initiative provides subsidies, tax incentives, and preferential financing to companies investing in automation, creating competitive advantages that extend beyond labor costs. This highlights how countries that combine manufacturing investment, workforce development and automation incentives may capture disproportionate gains in global competitiveness.

Policymakers are facing a dual challenge: continuing to incentivise automation, digital transformation and advanced manufacturing to secure competitiveness and supply-chain dominance, as well as resilient networks , while managing workforce disruption, trade-policy risks and regulatory oversight of AI and robotics systems. A balanced regulatory approach going forward should couple the already-existing automation and industrial incentives with workforce-reskilling programmes, regional manufacturing hub support, and flexible regulatory frameworks that continue to provide oversight of advanced robotics and cyber-physical systems for safety purposes.

Growth Areas

Looking ahead, several strategic growth areas within robotics and AI-enabled manufacturing warrant particular attention. One core growth area is the rise of lights-out factories. These are production facilities operating with minimal to no human presence, often during non-core shifts. As AI systems, autonomous robotics, and edge-enabled sensors mature, this operational paradigm grows more feasible.

Manufacturers are adopting this approach for its significant cost and efficiency benefits. Factories achieving true lights-out operation have reported 75-90% labor cost reductions and 150-300% output improvement. These gains stem not only from eliminated labor costs but also from the ability to run production 24/7 without shift changes, breaks, or the productivity variations inherent in human work cycles.

Another strategic frontier is self-optimising production systems. This was mentioned above but should be particularly noted as a key growth area. These platforms integrate real-time sensor data, AI analytics, robotics, and MES to automatically adjust production parameters. This includes parameters such as speed, tool choice, quality thresholds, and energy use, based on material variations, demand shifts, or defect trends.

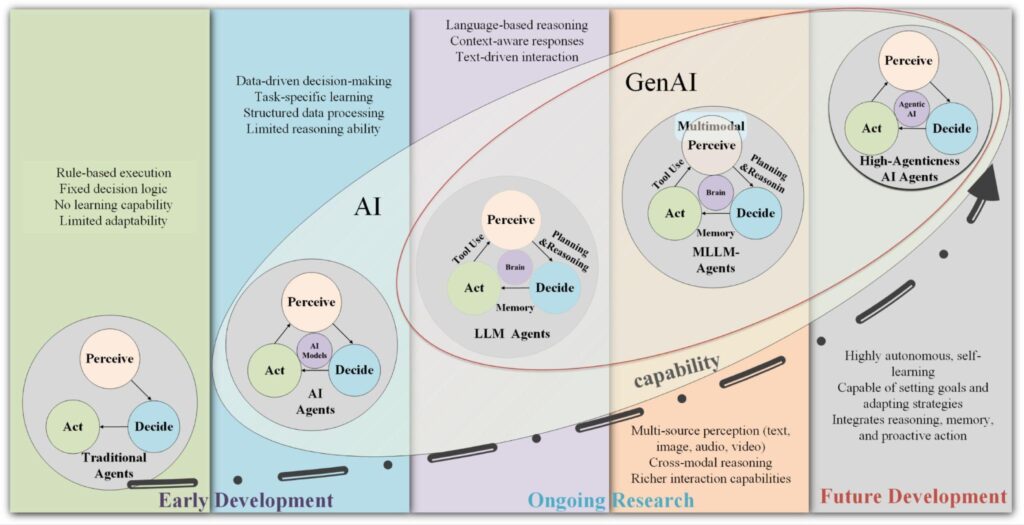

This integration is often done by agentic AI systems, mentioned above. In Figure 14 below, you can see some of the differences between different AI models, highlighting what makes agentic AI different:

Figure 14: Science Direct. Evolutionary path of AI agent technologies

One reason agentic AI is such a strategic growth area is that it moves systems beyond simple, rule-based automation. Instead of just reacting to programmed conditions, an agentic system can set goals, creating and executing complex plans, utilizing external tools, and learning from its own performance. Traditional automation follows “if-then” logic programmed by humans; agentic AI evaluates multiple potential actions, predicts their outcomes, and selects optimal strategies autonomously.

For instance, agentic AI continuously analyzes real-time sensor data regarding material quality, machine wear, and demand shifts. It can then autonomously adjust production parameters instantly and dynamically. If incoming raw materials show slight variations in composition, the system can automatically modify temperature, pressure, or processing time to maintain consistent output quality without human intervention. More generally, agentic AI can handle complex, multi-step tasks without continuous human input. This shift from static automation to dynamic, self-directed agency is what makes this market segment so valuable.

Stakeholder Strategies for Adoption

To successfully navigate this industrial transformation, coordinated strategies are necessary across all key stakeholders:

- For Manufacturers: One key initial step is to engage with pilot programmes in non-critical processes (e.g., machine tending or quality inspection). Manufacturers can prioritize the testing of hybrid human-robot systems rather than rushing to full automation and invest early in change management and upskilling the current workforce for new roles like robot supervision and maintenance. Also, focus on gaining knowledge of new markets, and avoid “all or nothing” approaches.

- For Investors: Prioritise companies with tangible, real-world deployments and recurring-revenue business models (e.g. RaaS). Focus on solutions that reduce operational costs, or tackle specific, quantifiable manufacturing pain-points, such as predictive maintenance, quality control, and reducing changeover time, rather than overly broad “general-purpose” robotics platforms.

- For Workforce Leaders: Shift training programmes from purely manual skills to hybrid roles. This includes robot supervision, data analytics, human-robot teaming, and system maintenance. Create clear career pathways from operator roles to certified robotics technician roles, ensuring employees view automation as an opportunity for advancement, not a threat.

- For Policymakers: In the current US political climate, policymakers should take care to create policies that continue to invest in and support automation development, while providing employment initiatives and other secondary measures that can maintain a strong economic position from a holistic perspective. Invest in technical education, low burden industry standards, and create policy incentives that drive both automation adoption, supply chain reshoring, and verifiable workforce reskilling and job creation.

Conclusion

The integration of AI and robotics in manufacturing represents more than technological advancement; it fundamentally redefines industrial competition. What began as isolated experiments in automation has evolved into a comprehensive transformation touching every aspect of manufacturing, from initial design through final delivery.

The data presented throughout this report demonstrates that leaders adopting these technologies are not achieving marginal improvements but order-of-magnitude advantages in productivity, quality, and adaptability. Those successfully integrating AI and robotics are achieving cost structures, quality levels, and operational flexibility that manual processes cannot match. The question facing manufacturers is not whether to adopt these technologies, but how rapidly manufacturers can transform.

Yet this transformation demands more than capital investment in hardware and software. Success requires simultaneous attention to workforce development, cybersecurity infrastructure, regulatory compliance, and organizational change management. The manufacturers thriving in this transition are those treating automation as a holistic business transformation rather than a purely technical upgrade.

The factory of tomorrow already runs today in pioneering facilities worldwide. BMW’s AI-driven quality systems, Bosch’s predictive maintenance platforms, and Amazon’s million-robot fulfillment network are not futuristic visions but operational realities delivering measurable results. Lights-out factories operating autonomously, generative design systems creating optimized components in seconds, and self-healing production lines that predict and prevent failures are transitioning from competitive differentiators to standard expectations.

As costs decline and capabilities expand, the convergence of agentic AI, humanoid robotics, digital twins, and edge computing will accelerate these changes, reshaping not just how products are made but also fundamentally altering the economics of global manufacturing. With the US striving for global economic and strategic dominance, the overlapping benefits are clear: reshoring, deregulation, and other policy initiatives that support US manufacturing and industry will have a large impact as AI and robotics in the sector take off.

For manufacturers, investors, workers, and policymakers, the imperative is clear: engage actively with this transformation and develop strategies that fuel technological and political ambition, while maintaining a clear view of the challenges that need to be carefully managed. The companies and nations that master advanced manufacturing today will define the global economy for decades to come.